Cate Gillon

Investment Thesis

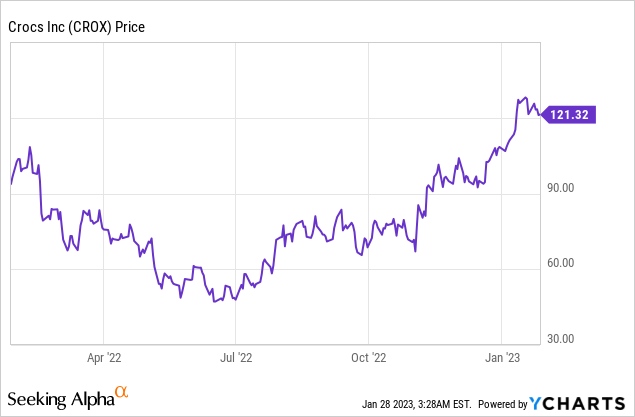

Crocs (NASDAQ:CROX) has been one of the best-performing companies in the past few months, with its share price up over 150% since June. The company has turned itself around in the past few years and has gained significant traction. I believe the company still has multiple growth opportunities in collaborations, digital sales, and the Asia market.

Despite the huge run-up in share price, the company’s current valuation is still very compelling. Its multiples are still below both footwear peers and its own historical average. Therefore I rate Crocs as a buy at the current price.

Growth Opportunities

Brand collaboration presents a massive opportunity as it significantly increases growth and brand relevance. Its collaborations with the likes of Salehe Bembury, Lightning McQueen, Balenciaga (OTCPK:PPRUY), etc., have been successful. With collaborations, Crocs can often sell its products for a much higher price than its normal ones. For example, some clogs from the collaboration with fashion house Balenciaga sell for over $900 yet the cost of production is essentially the same. Even after sharing the revenue with the collaborating brand, the revenue and margin for these products are still significantly higher. It can also introduce Crocs’ products to a different demographic (wealthy fashion individuals in this case) and increase brand awareness. I expect to see much more collaborations moving forward.

E-commerce is another growth driver that has been seeing strong traction. Due to the pandemic, the adoption rate for e-commerce has substantially increased. According to Statista, the e-commerce market is expected to grow at a CAGR (compounded annual growth rate) of 9.3% from 2023 to 2027. Digital channels are also more convenient, enabling more personalized experiences and stronger engagements. Customers are now much more comfortable purchasing online, especially with recognizable brands. For Crocs, digital sales currently account for only around 37% of total sales and the company expects the number to grow to 50%+ by 2026. This represents a potential revenue opportunity of $2+ billion and should continue to fuel growth.

Crocs

The Asia market opportunity is also huge. Unlike in the US, Crocs are still relatively new in Asia, which presents ample room for expansion. Sales from Asia currently only account for roughly 20% of total sales. The hype is now spreading over and Asia growth is seeing strong momentum. In the latest quarter, Asia’s revenue was up a whopping 82.3%. China finally reopening should also provide a big boost in demand, as the country is the second-largest footwear market in the world. I believe the Asia market will continue to provide strong tailwinds as brand relevance increases in the continent.

Anne Mehlman, CFO, on international growth

International was the largest growth driver for the Crocs brand in Q3, as we execute on our long-term growth plan to ignite the brand in Asia and EMEALA. Crocs brand revenues in Asia grew 82.3% to $138 million during the quarter. The strong growth was broad based across India, Southeast Asia, Japan and South Korea.

Valuation

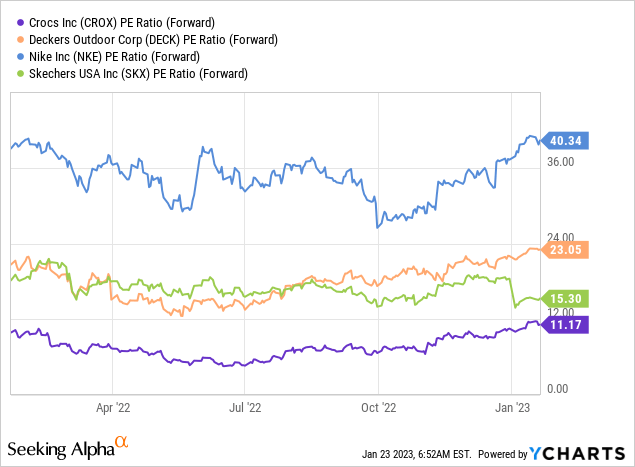

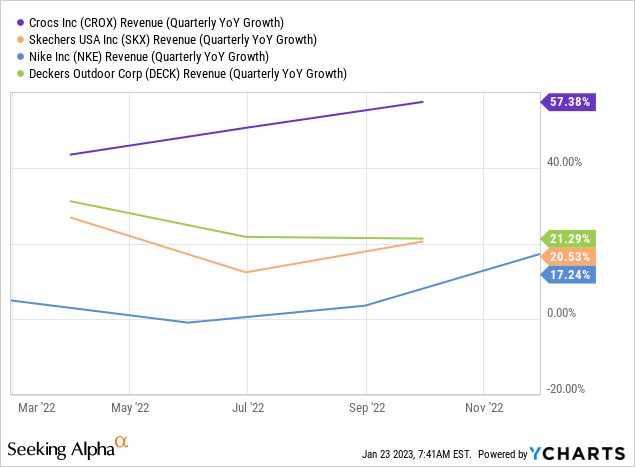

Even though Crocs has been executing on all levels and fundamentals continue to improve, the company’s valuation remains discounted compared to peers and its own 5-year average. Even after the 100%+ gain in share price from last June, the current fwd PE ratio is still very low at 11.2x. This is meaningfully below other footwear peers like Nike (NKE), Skechers (SKX), and Deckers Outdoor (DECK) which has an average PE ratio of 26.2x, as shown in the first chart below. This is a whopping 134% premium over Crocs’ valuation. Yet, Crocs’ latest quarterly revenue growth rate is actually the highest at 57.4%, significantly above the peer’s average of 19.7%, as shown in the second chart below. The current valuation is trading at a 38.1% discount compared to its 5-year average PE ratio of 18.1x. With Crocs expecting double digits revenue growth for the next few years thanks to its growth opportunities, I believe the company deserves a multiple similar to the industry’s average which should offer decent potential upsides from here.

Risks

I think one of the biggest risks in regard to Crocs is the hype and popularity cooling down. I believe a lot of Crocs’ momentum is generated from the latest fashion trends and the shift to the “work from home” life. However, fashion trends are always changing and it is hard to predict whether Crocs will continue to be the hot item. Also, people who buy them for home slippers already got them and should not need new pairs anytime soon. I am not saying Crocs will go away as it has been around for a long time but there are certainly risks in maintaining this elevated popularity. The company diversified its catalog and revenue stream with the acquisition of HEYDUDE which is smart. However, it is still relatively small and its brand recognition is much weaker than Crocs. It is showing exponential growth but whether the momentum is sustainable remains to be seen.

Conclusion

In conclusion, I think it is still not too late to get into Crocs. The company has multiple growth opportunities in collaborations, e-commerce, and the Asia market which should provide strong tailwinds moving forward. Despite having strong growth prospects, the market is still discounting the company and its valuation is still compressed compared to other footwear peers highlighted above. There are risks in regard to maintaining its popularity but I am not too concerned at the moment as momentum is still looking strong. I believe there is solid potential upside due to its discounted valuation therefore I rate the company as a buy.

Be the first to comment