buzbuzzer/E+ via Getty Images

Kite Realty (NYSE:KRG) shares have performed well over the past year with a total return just over 9%, significantly better than the broader REIT index/ETF (VNQ) which has had a -8% return. The company has benefited from the pruning of its portfolio (discussed below) as well as a strong appetite amongst retailers to lease space in well located shopping centers.

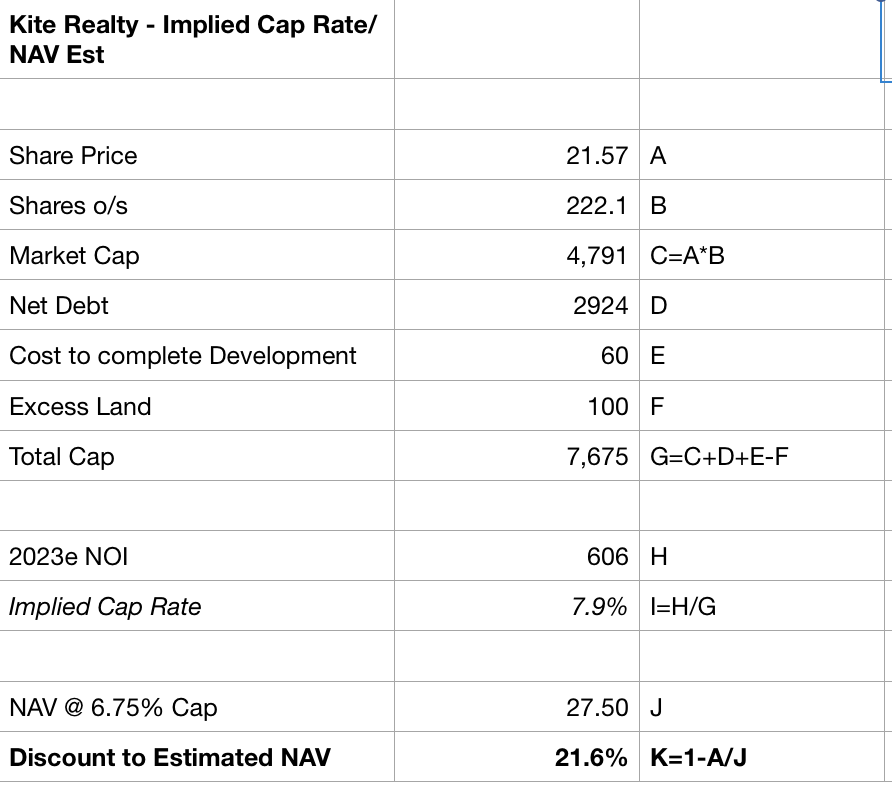

Despite the relatively strong share price performance, Kite shares remain inexpensive trading at an P/2023e FFO of 11x and an implied cap rate of 7.9%.

Overview

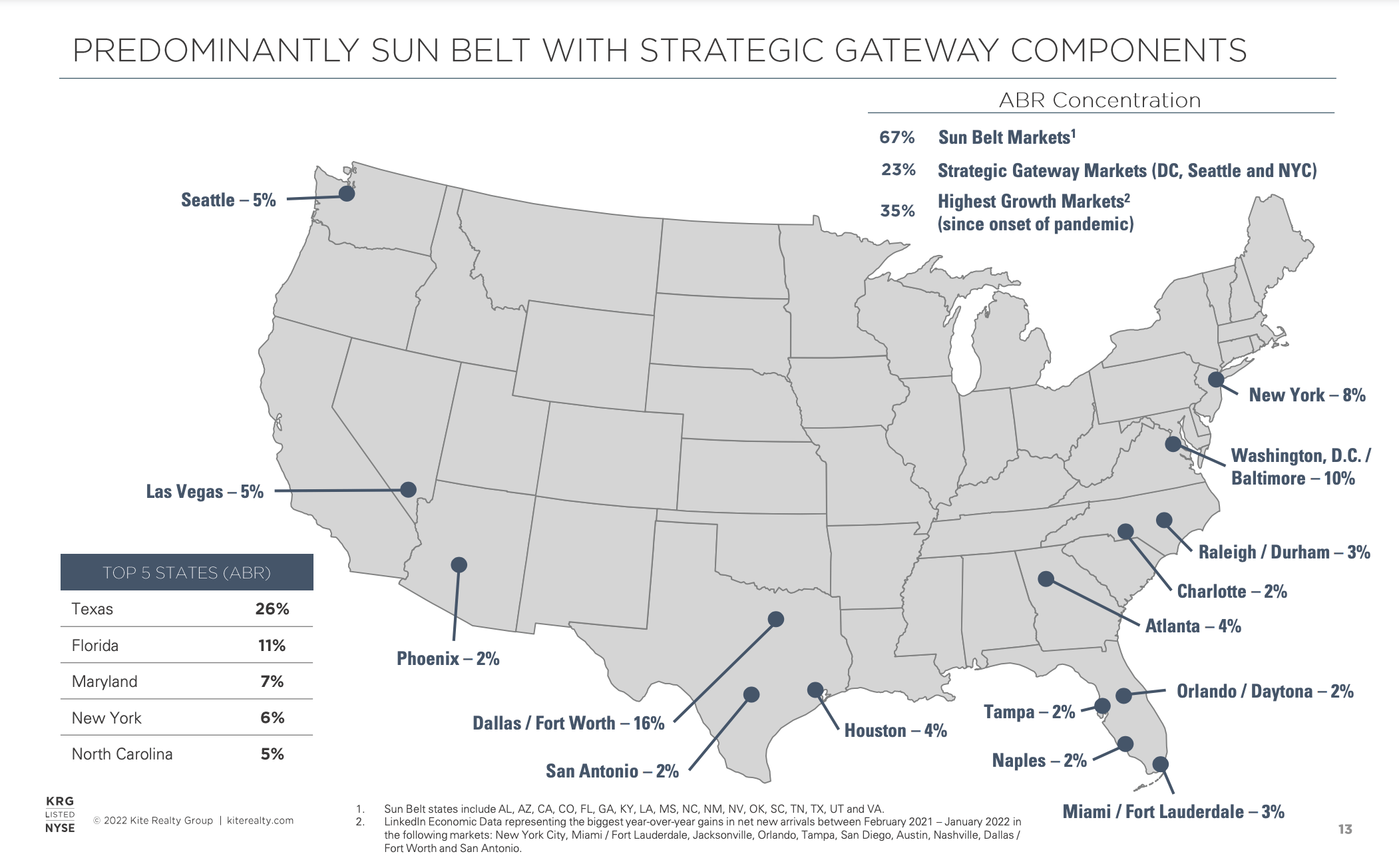

Following its 2021 merger with Retail Properties of America, Kite owns 183 shopping centers which average 158k square feet, more than 70% of which are grocery anchored. As shown below, 67% of Kite’s annual rent comes from sunbelt markets which have faster population growth than the national average. The company boasts a tenant roster which includes many proven winners in retail including TJX Companies, Kroger, Burlington, Publix and Ross among others.

NOI by Market (Investor Presentation)

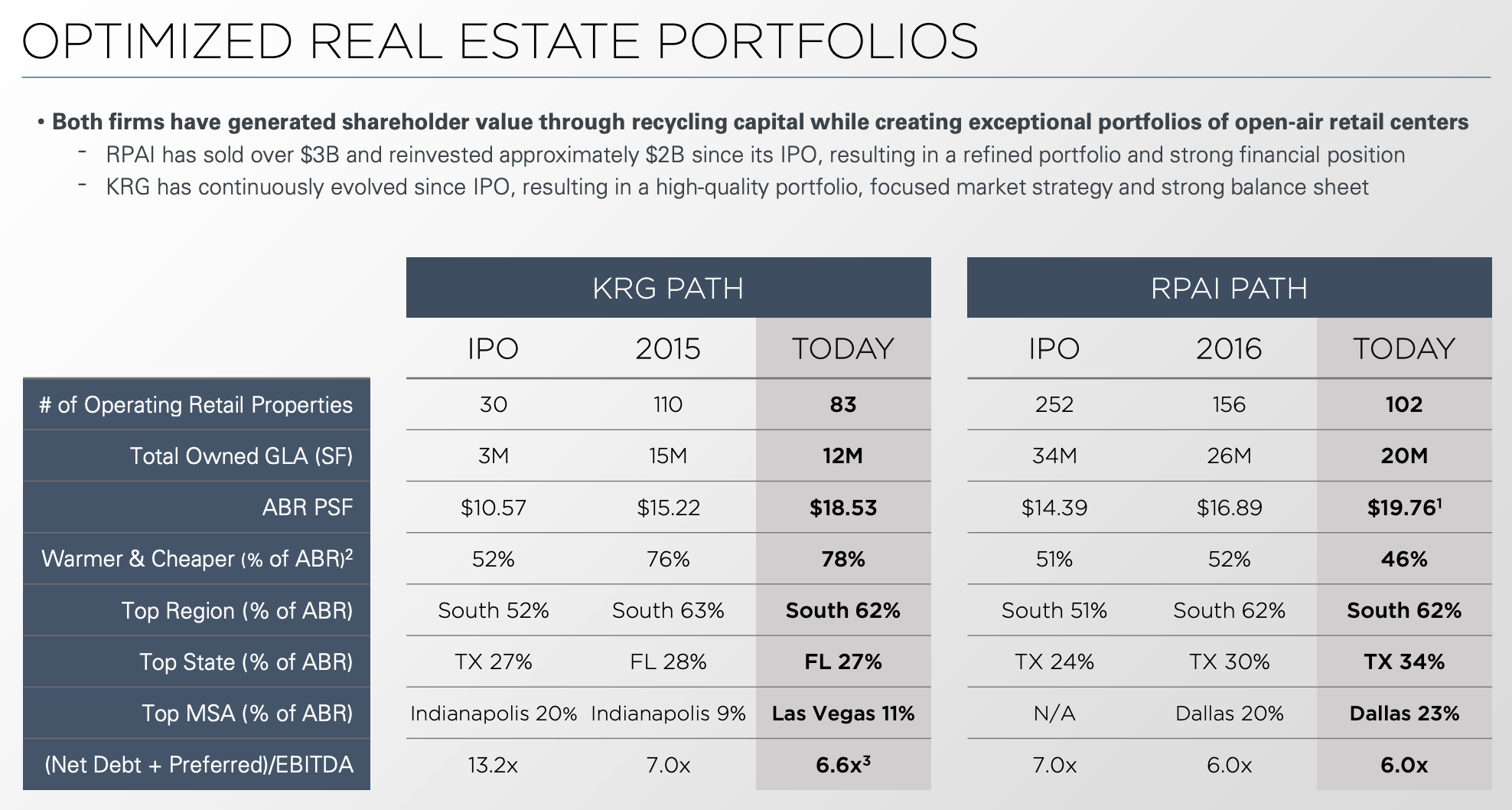

Like shopping center peers Brixmor (BRX) and SITE Centers (SITC), both Retail Properties of America and Kite underwent significant portfolio pruning since 2015 whereby lower quality centers were divested with the proceeds being used to reduce debt. As shown below, in total, over 80 lower quality centers (30%) were divested and leverage was reduced significantly with Net Debt to EBITDA declining from 6.5x to just 5.4x today.

Portfolio Pruning (Investor Presentation)

The culling of the bottom 30% of its portfolio, has left Kite with a portfolio of centers in high density areas serving more affluent customers with greater purchasing power – average household income within a 3 mile radius today stands at $117,000 which is up over 30% from 2015 as centers serving lower income communities have been divested. Further, Kite has re-invested some of the proceeds from asset sales to re-develop many of its remaining properties. In doing so, the company has not only earned attractive (8-12% incremental yields) returns on investment, but also increased the relevance of its shopping centers by bringing in more successful new tenants.

Shopping centers are a collaborative ecosystem whereby tenants benefit from the success of other tenants who drive additional traffic to the center and create an uplift in sales for all tenants within the shopping center. Importantly, this gives Kite an ability to increase overall occupancy (portfolio is 94% leased today, a multiyear high) and drive rents higher.

Current Conditions

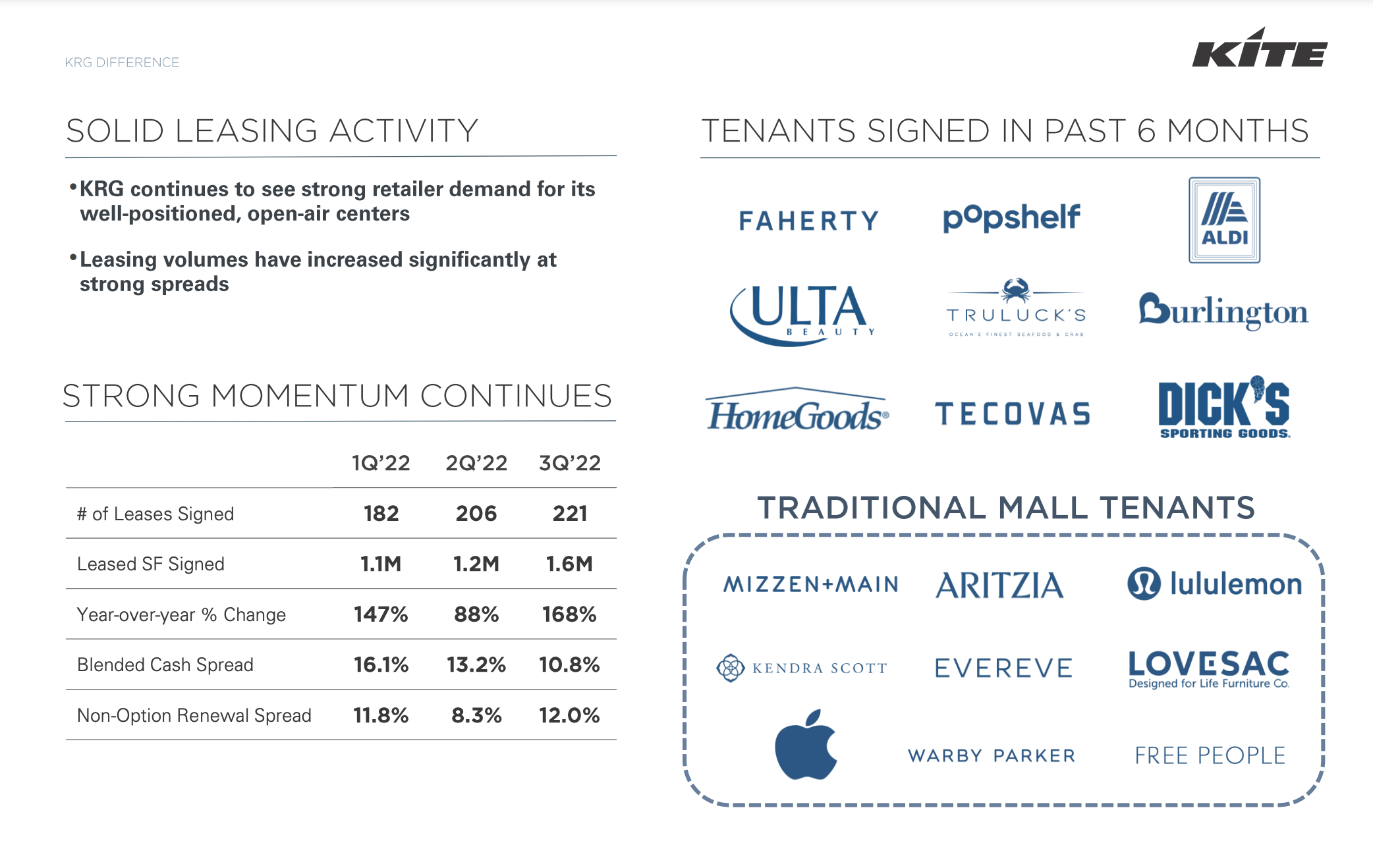

The environment for retail leasing remains very strong – after several years where retailers closed more stores than they opened, 2021-22 has seen a reversal of this trend with a dramatic increase in openings. Higher tenant demand has driven increases in occupancy (all major shopping center operators are now mid 90s leased vs. low 90s pre-COVID) and driving strong cash leasing spreads (shown below) which will positively impact NOI going forward.

Kite Leasing Trends (Investor Presentation)

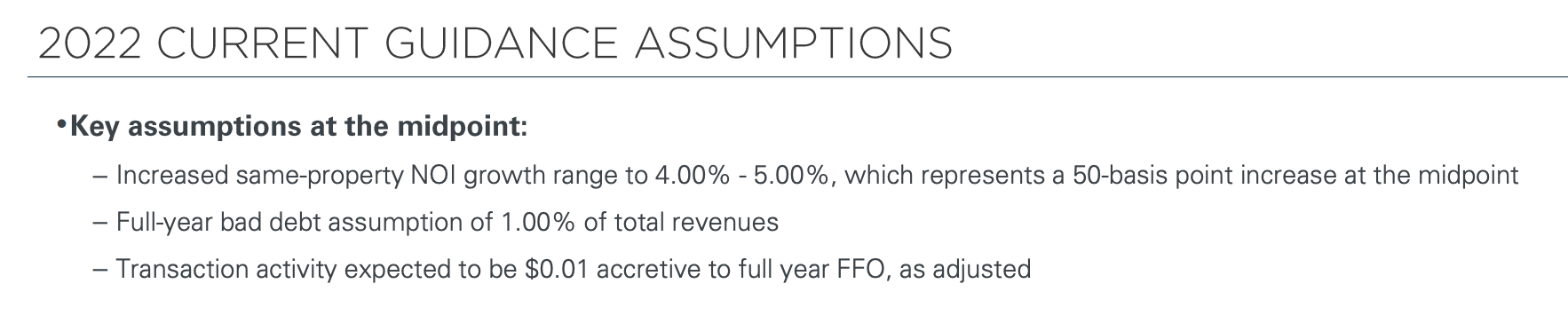

The strong leasing environment has shown up in increased occupancy numbers. As we sit today, the overall portfolio is nearly 94% leased (up from 91-92% pre-pandemic) with small shop occupancy (small shops have the highest rent per square foot in shopping centers) occupancy now exceeding 89% (was mid 80s in 2017-2019). The healthy rent spreads, increasing occupancy and lease escalators have led to 4-5% same store NOI growth guidance for 2022. I expect some moderation in 2023 as the economy slows and occupancy gains are harder to come by, I believe 3% is achievable as rent spreads should remain solidly positive.

2022 Guidance (Investor Presentation)

Valuation & Conclusion

As we sit today, assuming 3% same-store NOI growth in 2023 and taking into account development coming online, Kite trades at roughly a 7.9% cap rate as shown below:

Kite Implied Cap Rate & NAV Estimate (Company Filings; Author Estimates)

Ultimately I think the fair cap rate for Kite is around 6.75% which I used to calculate my $27.50 NAV estimate. Sunbelt grocery anchored neighborhood centers are probably worth a bit more (5.5-6% cap rate) whereas power centers in the northeast are worth less (high 7s-8).

Kite is a high quality collection of assets which I would like to own at the right price. While shares are modestly undervalued by my calculations, I believe there to be greater opportunities in the REIT universe, some of which I have recently written up here on Seeking Alpha. At this time I hold no position in Kite shares, but would be a buyer below $19 per share which would be a 30% discount to my estimate of intrinsic value (as a value, I always look to buy in at a hefty discount, typically 30% or more). Below I discuss some of the risk factors – some of which might cause the stock to decline and create an opportunity for me to buy in at or below $19.

Risks

1. A sharper economic downturn could lead retailers to curb expansion plans. A severe downturn could lead to retailer bankruptcies and store closures. To some extent we are starting to see this with the expected bankruptcy of Bed Bath & Beyond (BBBY) which represents 1.4% of Kite’s total rent. I also have concerns about tenant Michael’s (1.5% of rent) which was taken private in a leveraged buyout and is likely facing some of the same difficulties as competitor Jo-Ann (JOAN).

2. Continued interest rate increases may lead to further near-term declines in REIT prices.

Be the first to comment