Wirestock/iStock via Getty Images

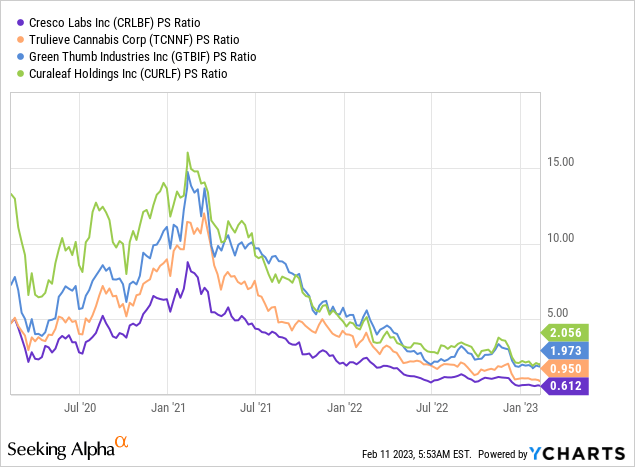

Cresco Labs (OTCQX:CRLBF) is one of the largest US multi-state operators by revenue but has had a relatively under-the-radar presence. The Chicago, Illinois-based company has one of the lowest price-to-sales multiples against its peers. Cresco currently trades on a retrospective PS multiple of 0.64x, lower than the multiple for Curaleaf (OTCPK:CURLF), Green Thumb Industries (OTCQX:GTBIF) and Trulieve (OTCQX:TCNNF).

This has placed Cresco’s market cap at $750 million and set the backdrop for the company’s acquisition of Columbia Care (OTCQX:CCHWF), the sixth-largest MSO by revenue. Whilst the $2 billion all-stock buyout would propel Cresco to the top of the MSO rankings based on combined revenues for the last reported fiscal 2022 third quarter, it currently faces material uncertainty with closing.

With Cresco’s near-term history being seldom defined by protracted periods of trading below a 1x price-to-sales multiple, the recovery of broad market sentiment likely forms the key driver of returns this year. The cannabis industry has always meandered between periods of high euphoria and heavy fears. The current market zeitgeist, unfortunately, falls into the latter with the opportunity for positive cannabis reform being missed as the plant remains illegal under US federal law. This dynamic is unlikely to change until after the next US elections in 2024, creating the backdrop for a continuation of the current dire performance.

The Columbia Care Buyout And Financial Momentum

Cresco announced its intention to buy New York-based Columbia Care early last year on March 23, 2022. The deal was meant to see Cresco acquire all of the issued and outstanding shares of Columbia Care with a close initially expected in the fourth quarter of the same calendar year. Columbia Care’s shareholders would receive 0.5579 shares of Cresco Labs for each share of Columbia that they owned. The transaction was valued at $2 billion against the closing price of both companies when the deal was initially announced.

Critically, the deal was meant to realize a number of benefits and catapult Cresco to become the largest MSO by pro-forma revenue at over $1.4 billion. The combined entity would have a 130-store retail footprint across 18 markets with a dominant market position expected in a number of states including Illinois and Virginia. However, the deal is yet to close and the board of Cresco and Columbia Care have been forced to divest certain parts of their retail footprint with a sale of stores and production facilities in New York, Massachusetts, and Illinois made to Sean “Diddy” Combs.

The closing of the deal is contingent on the approval of certain states and the company is now targeting a first quarter 2023 close. But uncertainty around proceeds from asset sales and the overall extent of dilution that will be required have driven Cresco’s commons to trade at a divergence from its peers even as its continues to notch some positive operational momentum.

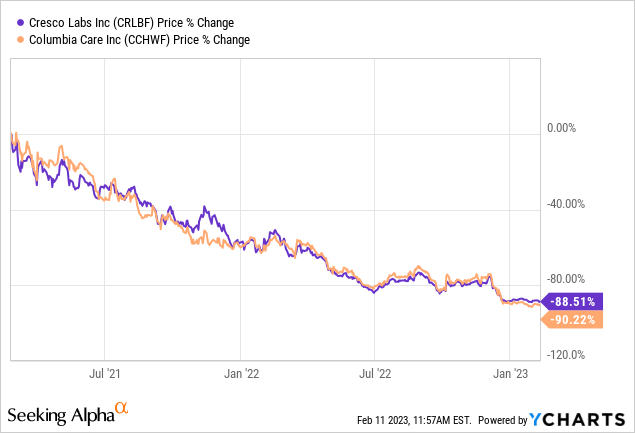

Since the deal was announced, the commons for Cresco and Columbia Care have fallen by 88.5% and 90.2% respectively. Whilst the share exchange terms of the buyout might have to be updated on the back of the divestments, management stated during their last reported fiscal 2022 third quarter earnings call that they don’t expect to divest any more assets.

The Recovery Of Sentiment And Returns In 2023

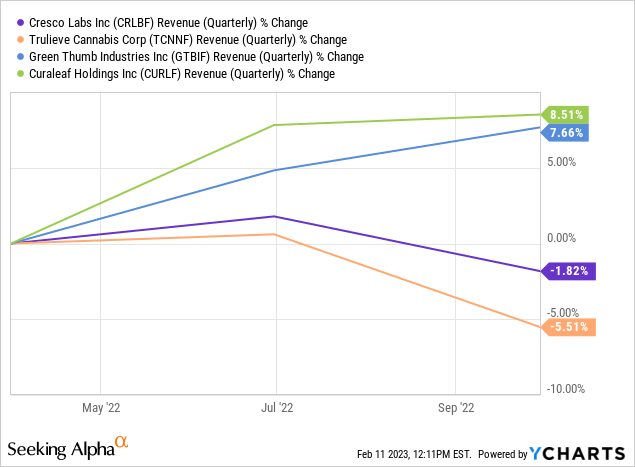

Earnings during the quarter for Cresco were mixed. The company reported revenue of $210 million, down by around 2% over the year-ago quarter. This was due to price compression in certain markets, albeit offset by sales growth in emerging states. Trailing 12-month revenue now stands at $842 million, broadly flat on the sequential comp with quarterly revenue having peaked at $212.9 million in the fourth quarter of fiscal 2021. Whilst the lack of growth is not rare against the broader North American cannabis industry as black market sales remain strong even against the regulated competition, other US MSOs have had more luck in growing their topline.

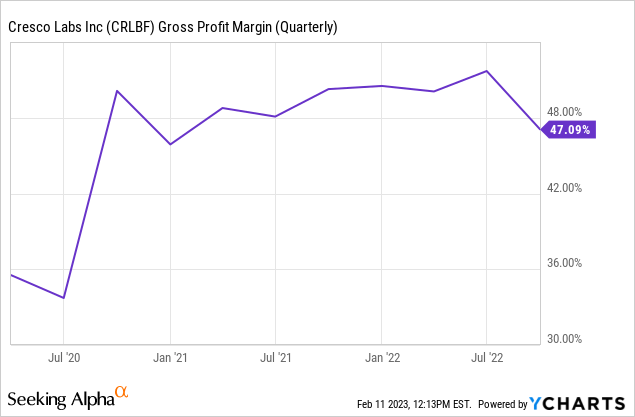

Adjusted gross profit of $100 million was driven by gross margins being at 47% but which trended down sequentially as a result of what management described as actions taken to boost long-term profitability. This included the closure of certain facilities and associated inventory adjustments. Gross margins would have been at least 340 basis points higher if these were excluded.

Core profitability, which I define as cash flows from operations, was positive with $25.6 million in cash provided from operating activities during the quarter. The company exited the quarter with cash and equivalents of $130 million against long-term debt of around $380 million. With positive cash flows generated in the last reported quarter, Cresco just had to repeat this feat to maintain a long runway and not have to lean on external funding in future quarters.

Critically, Cresco remains suspended at a point defined by uncertainty. This is uncertainty around its acquisition, around the legalization of federal cannabis at a federal level in the US, and around the direction of revenue growth. I’m neutral on its commons but we could see its unfavourable valuation dynamic change once these are all addressed.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment