I wrote an article last week parsing out the winners and losers of the digital ad industry following the implementation ATT (App Tracking Transparency). I shared this image and said the following:

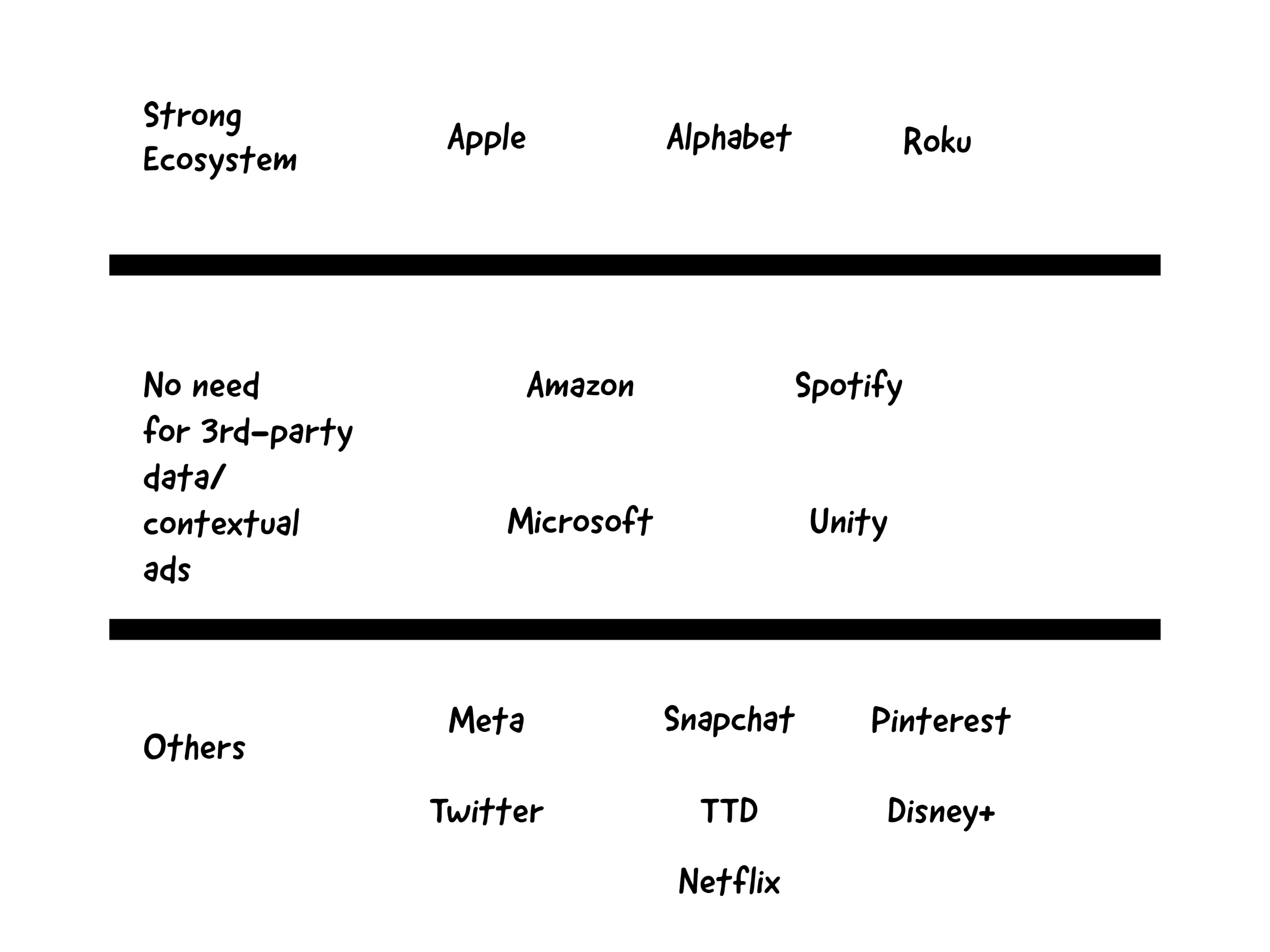

Winners and losers of ATT (created by user)

Because companies like Apple, Alphabet, and Roku control their ecosystem, they have perfect view of their customer data whether on their own apps or on the competing apps residing in their ecosystem. So they have a breadth of data of which they have full control.

Comparing that to the bottom group, they have their own data, but thanks to ATT they don’t have full visibility into their users, which affected their monetization capability.

I then went on to describe how ATT would affect each company, the likely winners, and the road to success in the industry going forward. The results from Pinterest (PINS), despite the positive reaction in after-hours trading, revenue only grew high single-digits in q2 and management guided to mid single-digit growth in Q3. This result is consistent with where I placed Pinterest in the image above. Pinterest does however have an advantage going forward in that can develop an e-commerce offering and use that to have more data about its users.

The Biggest Winner

I accidentally forgot to write about the biggest winner of all from the implementation of ATT; Apple Inc. (NASDAQ:AAPL) itself! ATT basically cut-out important user data that was previously collected by digital ad companies. That change affected their ability to monetize their users through ads. There is a subtle detail about Apple’s definition of ATT that advantages the company greatly compared to companies like Pinterest.

App Tracking Transparency allows you to choose whether an app can track your activity across other companies’ apps and websites for the purposes of advertising or sharing with data brokers.

The key word here is “other.” So companies do not need to ask permission for storing users activities on its own apps. So while digital ad companies lost the signal on what users were doing outside their apps, all of the users’ activity takes place in Apple’s ecosystem. This means that Apple doesn’t need permission to track that activity, given it is taking place in its own ecosystem. and all of a sudden Apple has all the data advertises need to monetize it for itself. The Apple Search Ads is an example of the benefits that Apple could reap from such an interpretation of ATT. Previously app developers could have gone to advertise at YouTube for example in search of users who could download their app. But if YouTube has lost the signal on Apple users, where would developers find a better place to advertise their app than on the App Store itself. Furthermore, what would stop Apple from acquiring or developing a search engine that can compete for Google’s business on iPhone. Apple doesn’t need to do that for now, from the New York Times:

Apple now receives an estimated $8 billion to $12 billion in annual payments – up from $1 billion a year in 2014 – in exchange for building Google’s search engine into its products. It is probably the single biggest payment that Google makes to anyone and accounts for 14 to 21 percent of Apple’s annual profits.

The pace of growth of that fee is astounding, and Apple could keep extorting Alphabet Inc. (GOOGL) for more or else it creates its own search engine.

Impact on Stock

Amazon.com Inc. (AMZN) managed to build a $30 billion advertising business in a few years, and it has nowhere near the data Apple has. I fully expect Apple to have a bigger advertising business than Meta Platforms Inc. (META) if not Google itself in 10 years. That means an additional $40-$75 billion in net income, that’s an additional $4.4 a share to its 2021 EPS of $5.61. And given Apple’s pricing power should reflect in a lower discount rate, it’s certainly feasible that Apple is selling at 14x earnings just from its current business and advertising, or that the company would sell for $287 a share if its P/E multiple remains the same ($10.01* P/E of 28.7 based on 2021 earnings). Investors would also get the optionality in the potential AR and EV businesses.

Risk

The obvious one is regulatory intervention related to Apple’s anticompetitive behavior. Apple is single-handedly upending the digital advertising industry as evidenced by q2 earnings and q3 guidance. It might be acceptable if the motive was promoting user privacy. However, if it turns out the company did that to advantage its ad business, then I wouldn’t be surprised if the FTC steps in.

Conclusion

Apple’s ATT change has wreaked havoc on the digital advertising industry, but it could stand to benefit given Apple has all the data other digital ad companies lost. One example of how Apple could benefit is in the potential growth the company’s search ads business could see as a result of ATT. Apple could even take on Google in search and win serious market share. All that could translate to a stock price of $287 in a bull case. The biggest risk however is that the FTC could step-in to address Apple’s anticompetitive behavior. The stock is a buy nonetheless on the merits of the current business alone.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment