Michael M. Santiago/Getty Images News

British American Tobacco (NYSE:BTI) ended FY 2022 with strong growth in its non-combustible product category that is putting the tobacco company on track to achieving profitability in FY 2024. Besides strong revenue and volume momentum in alternative products such as Vuse and Velo, the firm currently provides dividend investors with a 7.2% dividend. British American Tobacco also generates a material amount of free cash flow which supports the dividend and limits down-side risks. BTI’s valuation based off of earnings and the company’s positive business trajectory in new tobacco categories make the stock a very interesting buy for dividend investors. I don’t see a reason for BTI’s share price weakness and believe the market has turned too bearish on British American Tobacco in recent months!

Alternative product categories continue to see momentum

It is not much of a secret that the share of smokers is in a long term decline which is profoundly affecting the earnings prospects of the tobacco industry. It is therefore a key priority for tobacco companies like British American Tobacco to develop new product portfolios that accommodate changes in customers’ smoking preferences.

Approaching near-term profitability in new product category

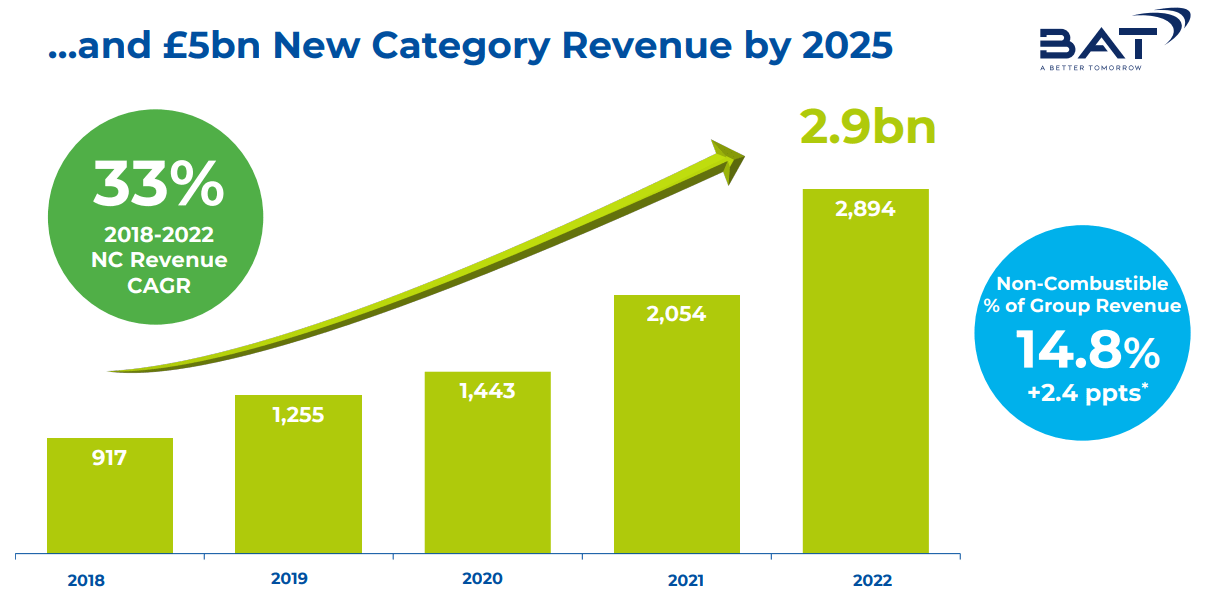

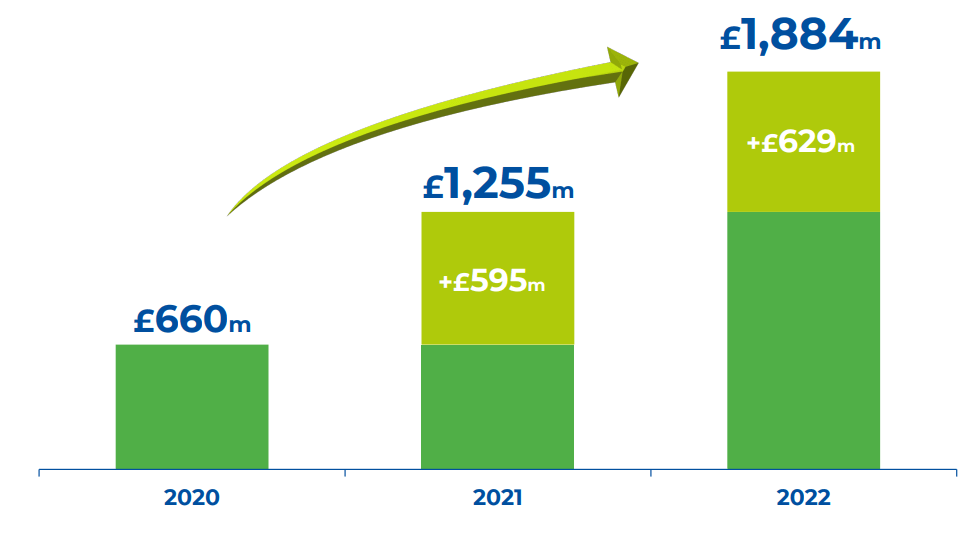

British American Tobacco’s alternative tobacco categories consist of the three brands Vuse, which are vape products, glo, which are BTI’s heated tobacco products, and Velo, which are nicotine pouches and lozenges. These alternative nicotine products are seeing strong customer acceptance, especially in the younger demographic in key markets such as the US and the UK. As a result, British American Tobacco has laid out a plan to aggressively grow alternative product revenues to £5.0B ($6.1B) by FY 2025, implying an annual average top line growth rate of 20%. British American Tobacco ended FY 2022 with alternative product revenues of £2.9B ($3.5B), showing an impressive year over year growth rate of 41%. Because British American Tobacco is aggressively investing in alternative tobacco products as well as marketing, I expect this momentum to continue in FY 2023.

Source: British American Tobacco

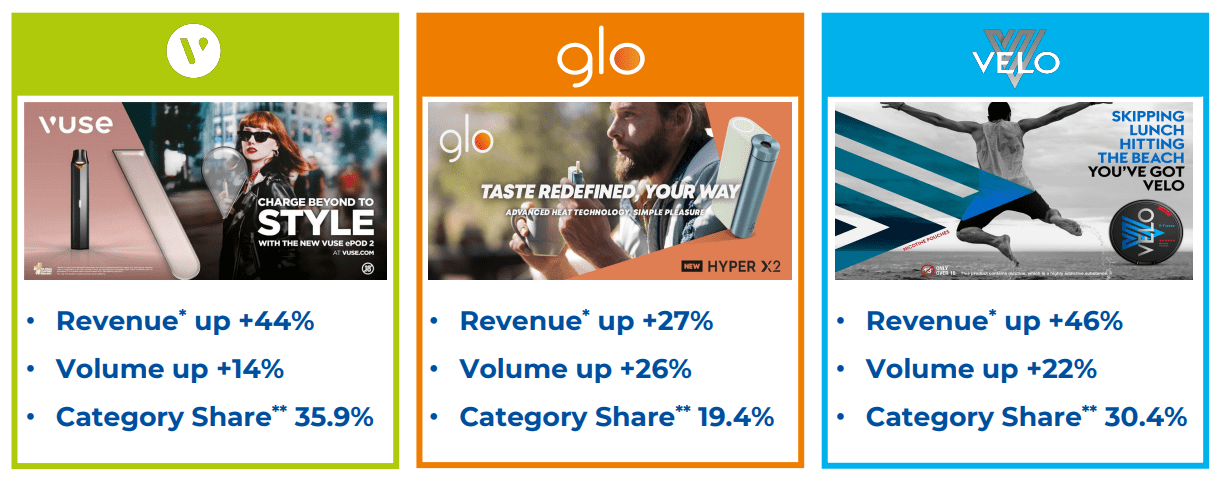

Vuse and Velo were the two strongest performing brands in British American Tobacco’s new category portfolio in FY 2022 as they continued to see revenue growth rates in excess of 40%. Revenue growth has been driven chiefly by strong customer adoption which is driven by double-digit volume gains. Vuse, BTI’s vape brand, generated 44% revenue growth in FY 2022 and the brand now has a value share of 36% in the US.

Source: British American Tobacco

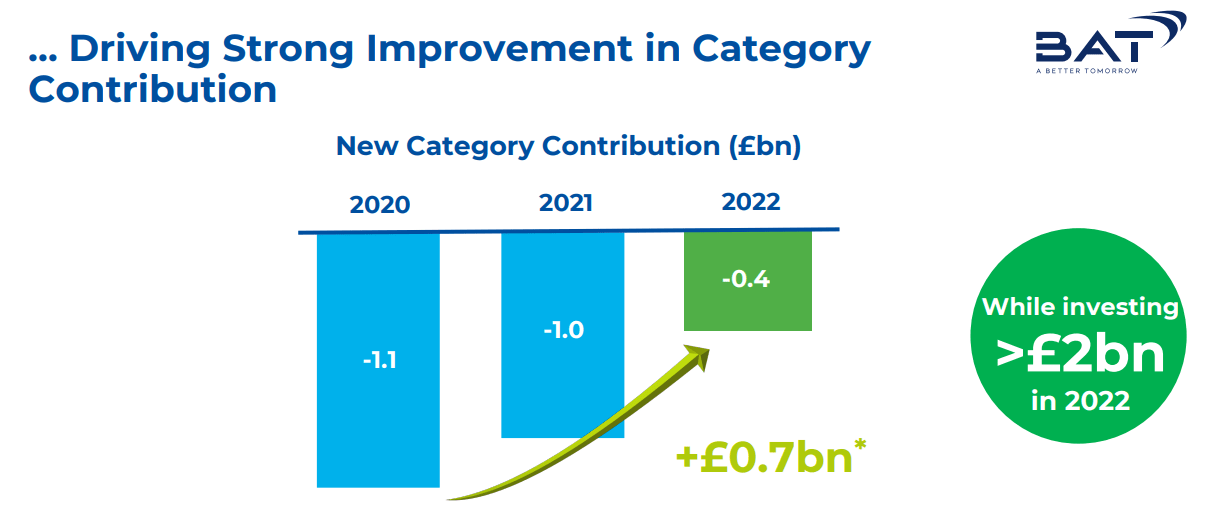

A clear path to profitability

Heavy investments in alternative tobacco products are starting to pay off for British American Tobacco. The company invested more than £2.0B ($2.4B) in the development of its alternative product brands last year and the new category portfolio is set to make a positive profit contribution in FY 2024.

Source: British American Tobacco

Effective cost savings program

British American Tobacco has implemented a cost savings program that initially called for cost cuts of £1.0B ($1.2B) which the company well exceeded in FY 2022. Total cost savings in FY 2022 amounted to £1.9B ($2.3B) which is accelerating BTI’s path towards profitability. I believe the reach of profitability in the new product category could be a strong catalyst for share price appreciation.

Source: British American Tobacco

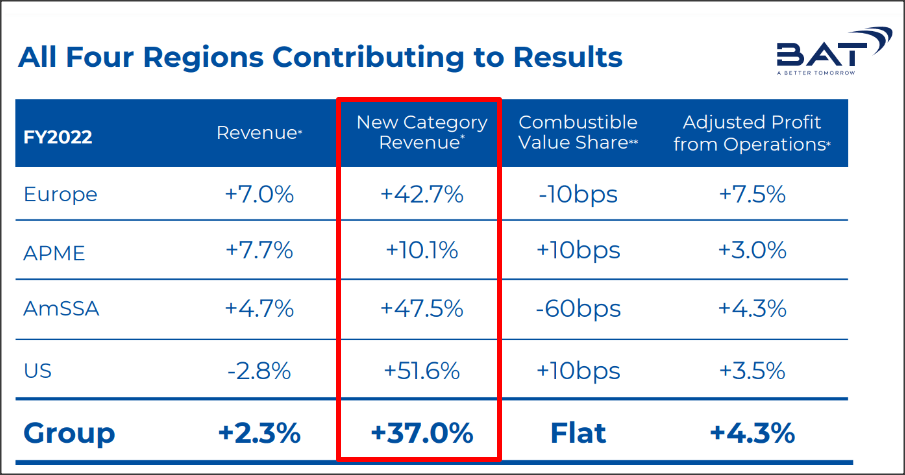

New categories and non-US markets driving growth

British American Tobacco reported 2.3% consolidated revenue growth for FY 2022 (in constant currencies), but the majority of this growth occurs in new categories (as just discussed), but also in non-US markets. Europe is especially doing well for British American Tobacco, largely due to the roll-out of alternative products in Scandinavian countries like Sweden and Norway. New categories saw 37% revenue growth in FY 2022 (in constant currencies) to £2.9B ($3.5B). New categories had a revenue share of 10%. Longer term, I see this revenue share go to 20% for BTI.

Source: British American Tobacco

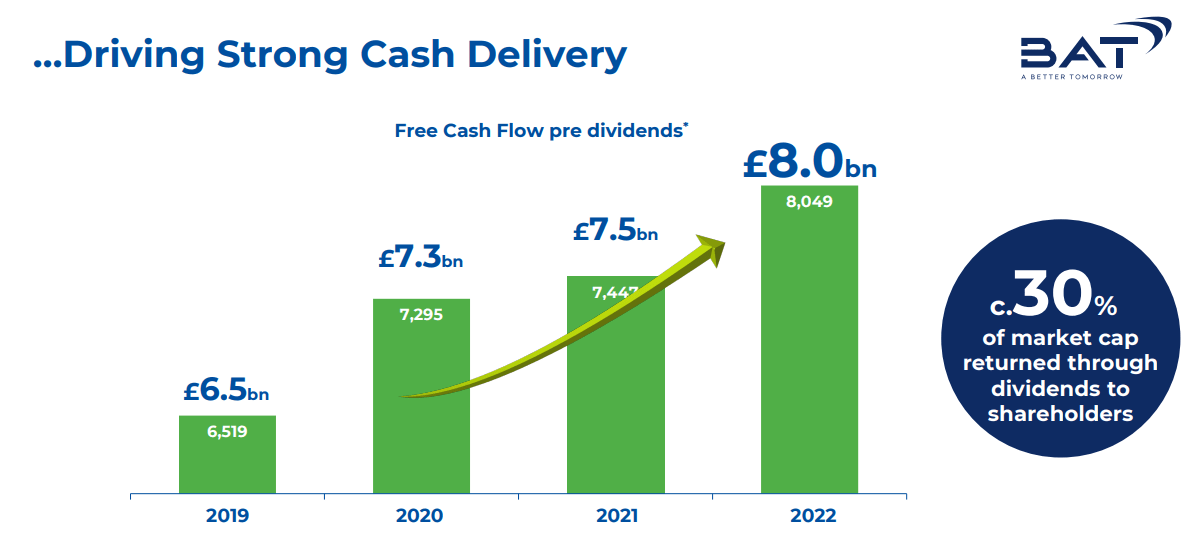

Upswing in free cash flow support by new category growth

BTI’s free cash flow is sufficient to pay shareholders a strong dividend. But it is also a potential stabilization factor that could limit BTI’s down-side potential going forward. BTI reported £8.0B ($9.7B) in free cash flow for FY 2022, showing a 7% year over year improvement. The growth in free cash flow is driving by cost savings, volume gains as well as growing alternative product revenues.

Source: British American Tobacco

BTI’s valuation vs. rivals

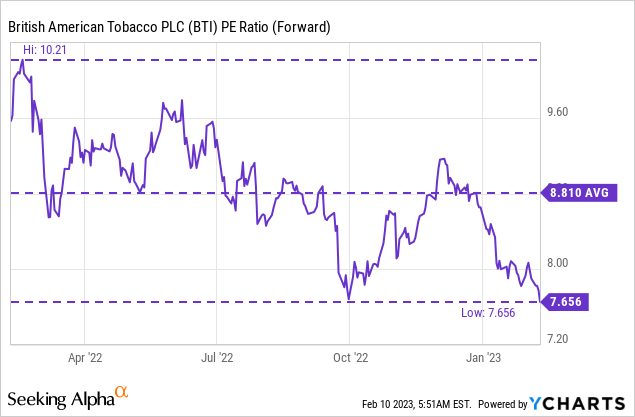

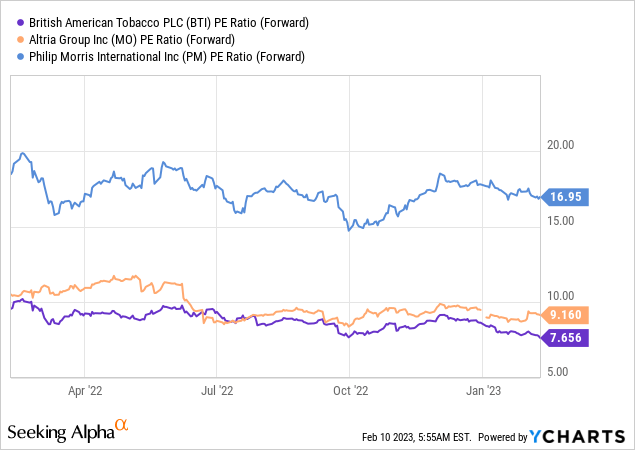

British American Tobacco is not the cheapest of the tobacco sin stocks, but that doesn’t mean that BTI is not an attractive dividend investment. British American Tobacco is expected to see 3.8% top line growth this year and 5.4% next year. The tobacco company’s stock is currently valued at a P/E ratio of 7.7 X which is at the low-end of BTI’s P/E range in the last year. The earnings multiplier used here assumes $4.80 per-share in earnings in FY 2023.

Relative to other tobacco companies, I believe British American Tobacco also compares very favorably: Altria Group (MO) and Philip Morris International (PM) trade at P/E ratios of 9.2 X and 17.0 X which makes BTI the cheapest available sin stock based off of earnings.

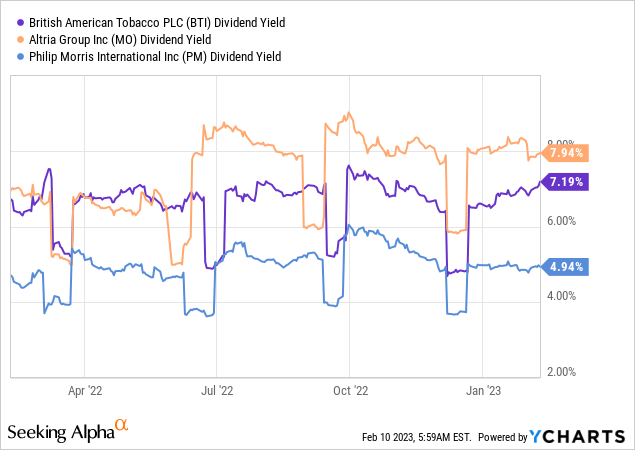

Regarding dividend yield, British American Tobacco offers the second-highest dividend after Altria which currently pays 7.9%. Altria’s yield is solid and covered by adjusted earnings which is why I recommend MO to dividend investors as well.

Risks with BTI

There are a couple of risk factors that investors investing in sin stocks should care about. Anti-tobacco regulation continues to be a big headwind for British American Tobacco as well as for the industry. A ban of e-cigarettes or vape products is also a potential risk for British American Tobacco as it would cut into the growth potential of its alternative product category which is currently driving BTI’s free cash flow and revenue upside.

Final thoughts

The market is wrong in pricing BTI so cheaply considering how much free cash flow the firm generates and how solid the new category momentum has been in FY 2022. British American Tobacco has clear momentum in its alternative products category and reaching profitability in FY 2024 could be a catalyst for the stock. The firm’s strong free cash flow both finances the dividend and supports the share price which has seen renewed weakness since December. I believe that the combination of British American Tobacco’s strong free cash flow, revenue and volume momentum in Vuse and Velo as well as a low valuation based off of earnings add to British American Tobacco’s appeal as a dividend stock going forward!

Be the first to comment