imaginima

Crescent Energy (NYSE:CRGY) was formed by the merger of Contango (MCF) with a Kolberg Kravis & Roberts (KKR) controlled entity. Many of the properties were acquired during the cyclical industry downturn. Others were in other subsidiaries for a while. But the significance of acquiring properties during a downturn is that the breakeven point for that production is often far lower than is the case for organic growth. The reason is that the acquirer is often in the position of being able to pay less for the remaining production than it originally cost in the first place. Then when a recovery has begun (as is the case now) an unusual amount of cash flow and profitability will manifest itself.

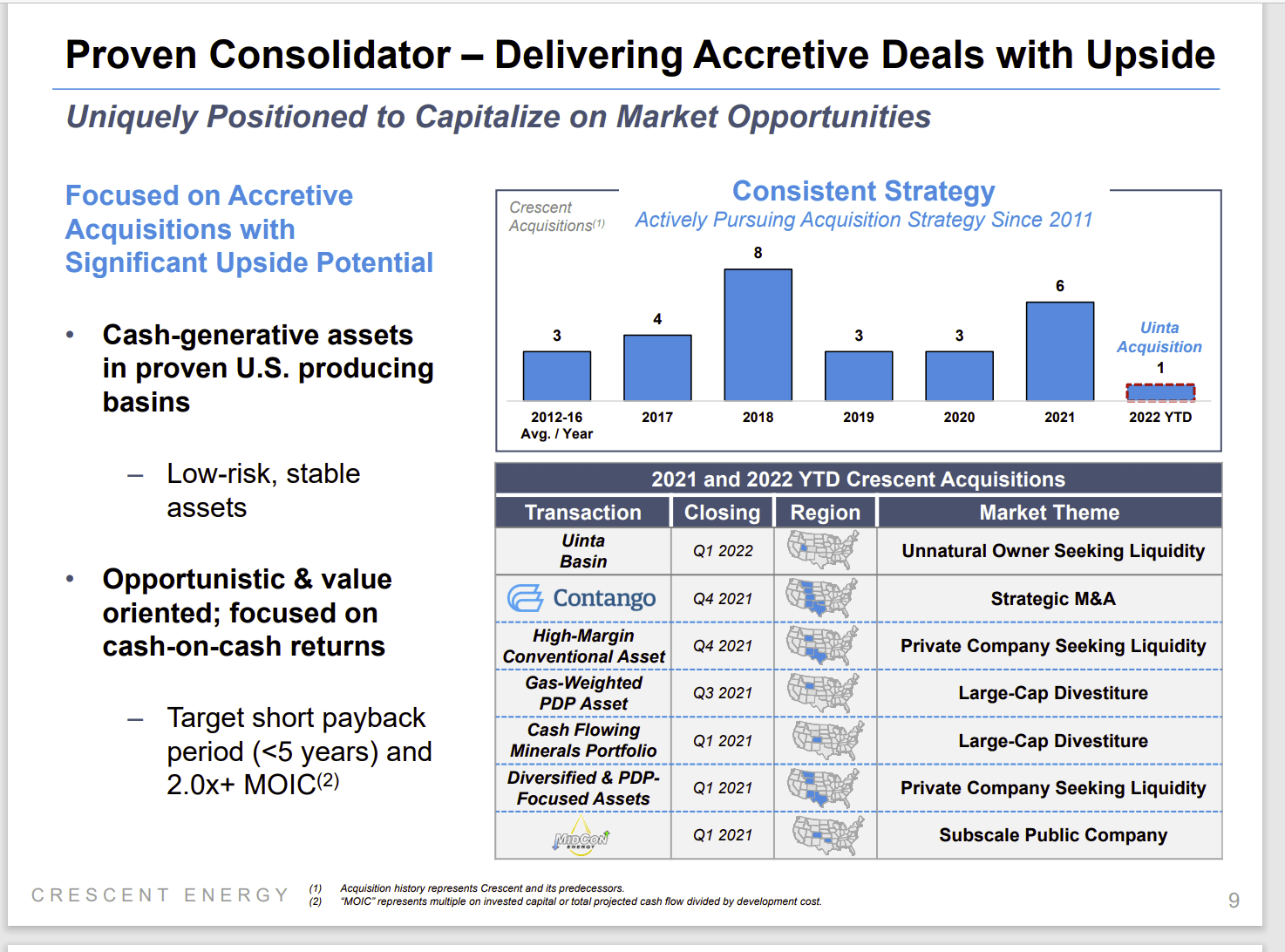

Crescent Energy History Of Acquisitions From Distressed Sellers (Crescent Energy November 28, 2022, Corporate Presentation)

The clear emphasis was on companies that “wanted out” for one reason or another. This put the company “in the catbird seat” when bargaining over the acquisition price. The combination with Contango supposedly brought together two companies with similar ideas about acquiring bargains.

Many of the properties needed optimization to reduce operating costs. This would enable more reserves than were probably booked at the closing of the acquisition. Many of the properties have long-lived production.

But where most companies have to spread the production cost over the well drilling and completion costs, this company has no such obligation for the acquisitions. This management simply paid for a stable (and predictable) production that would produce a cash flow in the future at agreeable prices. The noncash production costs are therefore likely to be far lower than is the case for organic production growth.

The benefit of making acquisitions during the period of 2019 to 2021 was that a lot of forecast pricing was extremely low compared to current forecasts. Some of the properties like the Barnett are probably far more profitable than the sellers would have expected. The extra profitability raises the long-term return on some of these properties.

Overall Strategy

The initial strategy was to acquire established production with a low decline rate that would provide a predictable future cash flow. That would mean low maintenance costs to maintain production because not much new production would have to be added to keep production levels constant with the previous fiscal year.

The cash flow would allow for a quick deleveraging of the company if that was needed. The main goal is to keep ratios conservative so that management can quickly take advantage of any deals that appear. This tends to be a countercyclical strategy. Therefore, not many acquisitions will likely be made during periods of relatively robust commodity prices. Instead, management will wait for a more pessimistic period to make acquisitions. That accounts for the relative lack of acquisitions made in the current fiscal year.

Growth

Instead, management will emphasize organic growth as that should be cheaper in the current economic environment.

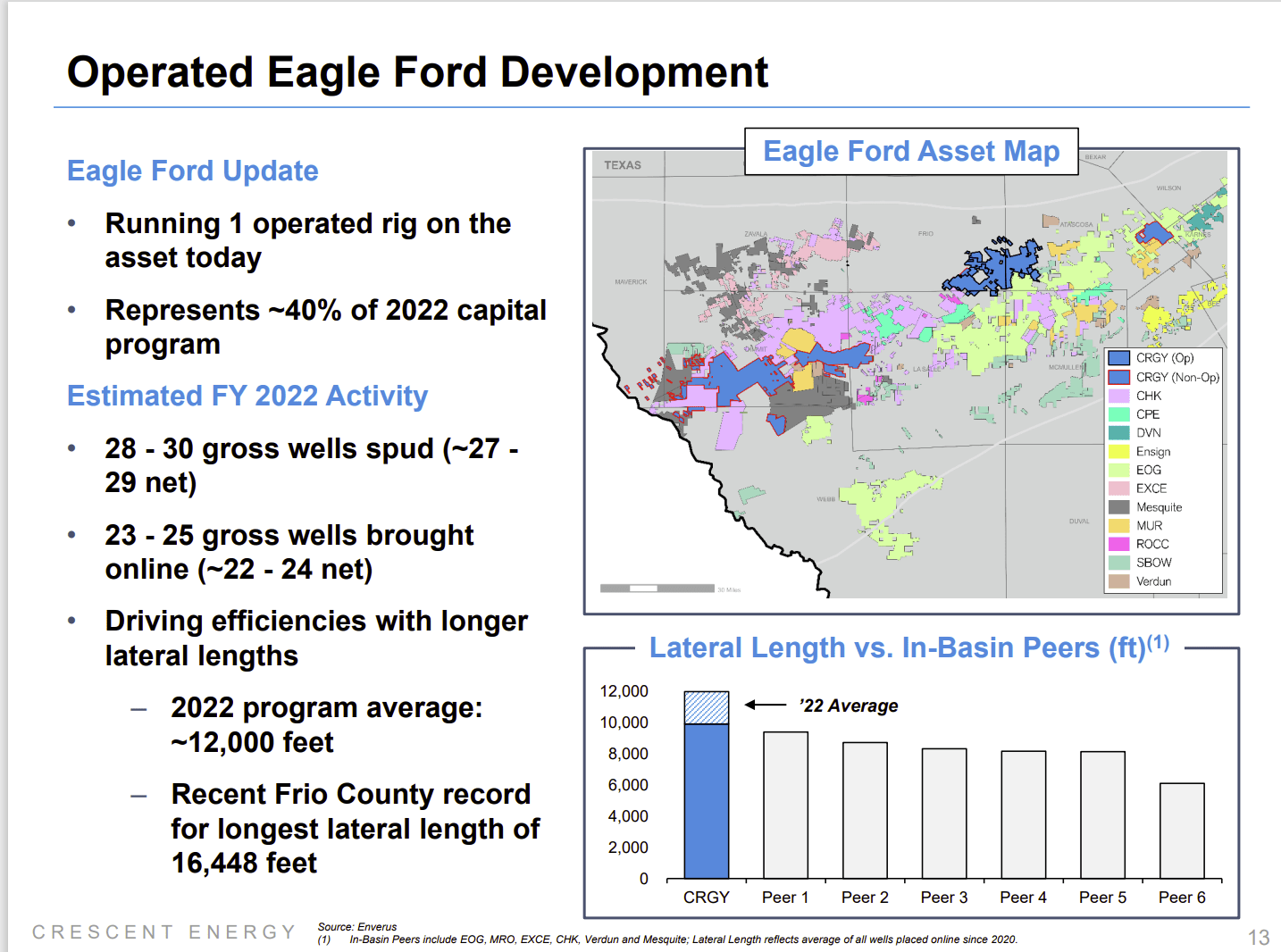

Crescent Energy Eagle Ford Operating Strategy (Crescent Energy November 28, 2022, Investor Presentation)

Probably one of the lowest cost basins in the United States is the Eagle Ford. The returns in this basin are often competitive with the Permian. But there are not the Permian issues like takeaway capacity during the boom times. Last business cycle, the takeaway issues led to an oil price discount and high transportation costs for those affected. In the meantime, Eagle Ford production had access to a surplus. Realized profits by operators turned out to be different than one would have expected due to the realities of boom times.

The Eagle Ford often cash flows during industry downturns due to the low breakeven costs in the basin. Many operators report breakeven times in months in the current commodity price environment. That means that an operator can hedge production if needed to assure a reasonable profit should the outlook for commodity prices weaken. That is just perfect for a company that needs robust cash flow to take advantage of distressed sellers when there are few buyers around.

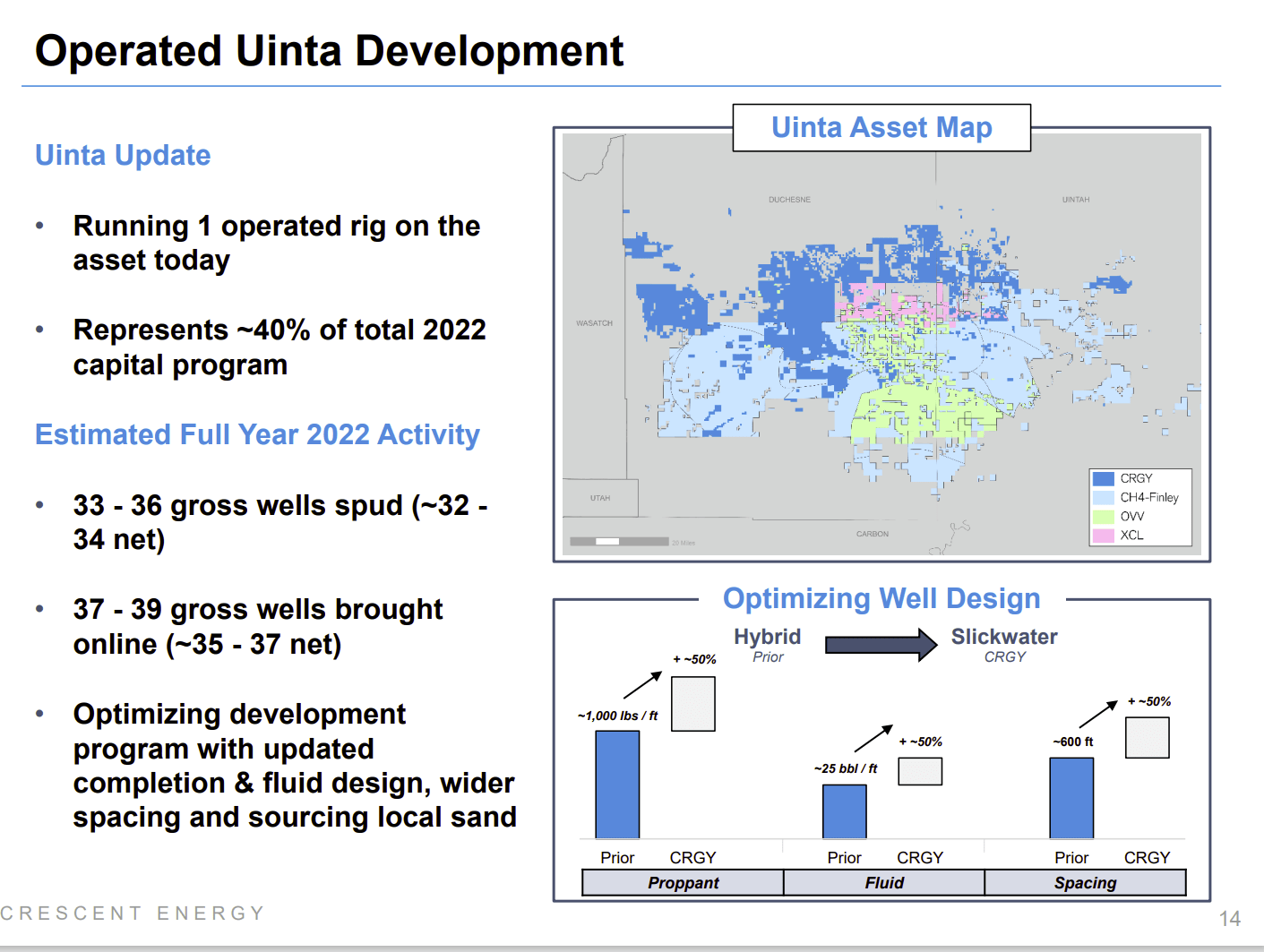

Crescent Energy Unita Operating Strategy (Crescent Energy November 28, 2022, Investor Presentation)

The Unita area has had a reputation for faster well production declines. That has often meant that in the past a greater percentage of cash flow was needed to maintain production. However, this basin should be robustly profitable in the current environment while producing decent free cash flow.

As shown above, management has worked on the well design and completion to hopefully produce better returns on invested money. The faster decline rate can be handled as long as overall production yields an acceptable profit. Right now, that appears to be the case.

Both the Eagle Ford and the Unita point towards a time of organic growth in the future while maintaining a very strong balance sheet to pursue a countercyclical strategy of acquisitions during times of weak commodity prices.

The Future

The backers of this company are known entities that generally emphasize both cash flow and free cash flow. That is in contrast to much of the industry that grew for a long time by debt financing or secondary stock offerings. The entry of a company like Crescent Energy would therefore indicate that prices are very low for such a cash flow strategy to succeed. One might conclude that this is the time to consider investing in the industry while the time to sell will be later in the industry cycle.

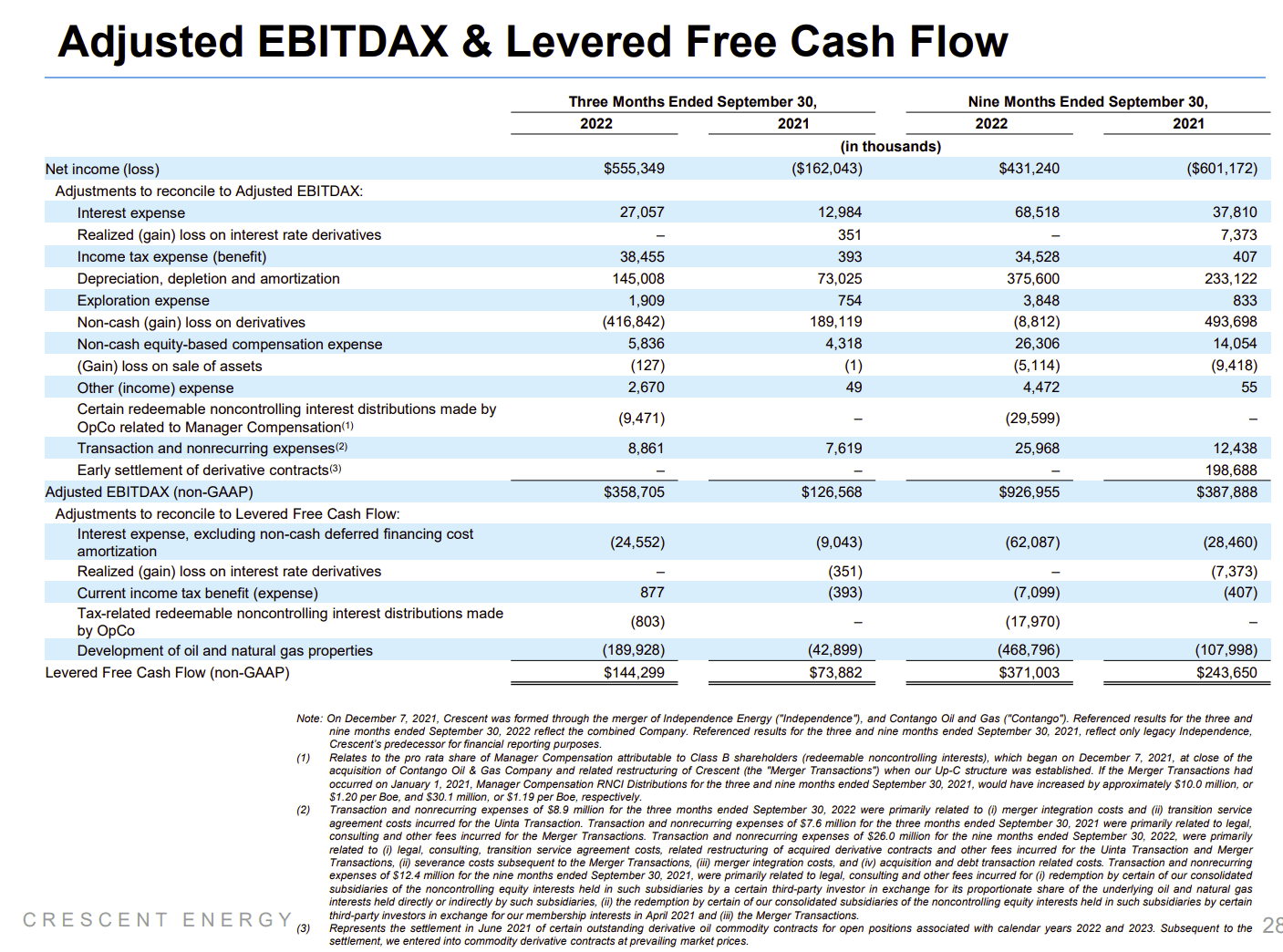

Crescent Energy Free Cash Flow Calculation and Comparison (Crescent Energy Third Quarter 2022, Earnings Conference Call Slides)

This management appears to have a fairly conservative view of cash flow because the “Development Of Oil And Natural Gas Property” line is unusually significant in relative size. But that would agree with the history of the backing parties. The main goal would be for the oil production to grow while at the same time producing free cash flow to provide a decent return on investment.

Income investors can probably look elsewhere as the near-term goals of this management are to optimize operating costs while repaying debt to pursue a countercyclical acquisition strategy.

Compound returns usually generate the largest return. These investors are unlikely to want the majority of free cash flow back as long as they can find future investments that meet a profitability hurdle. Therefore, the dividend is likely to be a small part of free cash flow for the foreseeable future. That dividend is also likely to grow rapidly.

One of the temporary issues is the fee structure with KKR. One of the market issues is confusion with the fee structure for a leveraged buyout which has far higher risk in comparison to something like this where the financial risk is very low. One way or another, this issue will resolve itself promptly. All one has to do is look at the per barrel amounts reported so see that the administrative charges are very reasonable compared to many companies of a similar size.

Rarely do investors get the opportunity to invest alongside investors like John Goff and KKR in a public entity. This is one of those opportunities. Both backers own a substantial amount of stock. Therefore, they are aligned with the common stock shareholders.

As a newly public entity, this stock will likely be cheap until a public track record is established. But the management is unusually experienced for a company of this size. That and the low debt provide a measure of safety often absent in the upstream industry.

Be the first to comment