deepblue4you

Mazda (OTCPK:MZDAY) is pretty reasonably valued among automotive stocks, and we think the next earnings are going to look pretty good as China reopens. Generally, automotive stocks all have some tailwinds from pent-up demand as supply chain issues kept volumes pretty depressed. On the downside, Mazda is not that well positioned for the re-appreciation of the Yen, and of course, economic pressures could have an outsized effect on consumer durables. Mazda looks like a good value, but investors should be careful.

Moving Parts

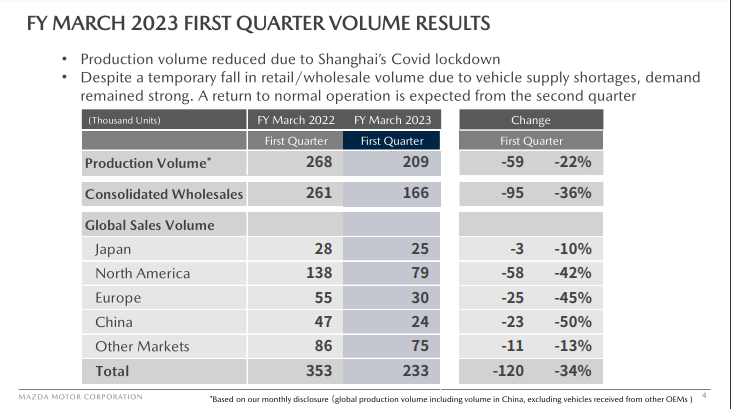

The last quarter was being harangued by issues with lockdowns on the production side in Shanghai caused by COVID-zero policies that are no longer in place. Moreover, demand was particularly depressed in the Chinese end-market as well as the Chinese economy went dormant in 2022. With the end of COVID-zero policies, we expect Mazda volumes to be particularly good in the next quarter in global markets as Chinese production resumes, as well as in the quite important Chinese market.

Volumes (Q1 2023 Pres)

Another factor affecting results a year ago was the ongoing supply shortages causing the inflation we saw in 2022. Semiconductors were still hard to come by at that point and automotive volumes were still depressed. While issues specific to Mazda affected revenue booking last quarter, the YoY comps are not going to be as hard to beat since supply chain issues are resolving rapidly at this point as markets cool down. Still, there should be pent-up demand as deferred purchases come through. The North American data is looking good as of December for Mazda.

On the negative side, there’s of course the higher rate environment, which could be threatening the deferred purchases that are being planned by customers. As a consumer durable, continued high rates put pressure on the velocity of the automotive market. While rates are likely to come down as inflation eases, a Chinese reopening affects global prices and could reintroduce inflation concerns. Sustained higher interest rates are not good for Mazda. In markets outside of the US like Europe, direct inflation from trade dislocation is similarly a threat on demand, and the data shows declines in vehicle registrations.

The other issue is FX. Mazda’s costs are more in Yen than their revenues. With a depreciating Yen, Mazda was doing comparatively better, with less FX-based cost inflation than revenue growth from more valuable dollars coming in from the large North American market. The Yen has roared back as markets speculate against the USD rate regime and because of the debt crisis kerfluffle. This could reverse again if markets aren’t pricing in a longer-than-expected rate decline regime in the US, but generally, the return of the Yen is not that great for investors.

Bottom Line

Valuation is not a major concern for Mazda. The multiple is around 5x in PE, with comps like Volkswagen (OTCPK:VWAGY) lying lower under 4x. It’s perhaps not the very best deal, but much in the same way VW is covered by the new Porsche IPO, Mazda is also covered by non-operating assets of stock in Toyota (TM). There is a good earnings yield here, and a more bothered year by supply chain issues and Chinese markets going dormant means that there is some more relative ground to gain for Mazda to shrink its multiple differential. Still, the issue is more directional – a consumer durable stock is a risk when the market is hard to call. We don’t want to be owners in automotive stocks if or when pent-up demand runs out.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

If you thought our angle on this company was interesting, you may want to check out our idea room, The Value Lab. We focus on long-only value ideas of interest to us, where we try to find international mispriced equities and target a portfolio yield of about 4%. We’ve done really well for ourselves over the last 5 years, but it took getting our hands dirty in international markets. If you are a value-investor, serious about protecting your wealth, our gang could help broaden your horizons and give some inspiration. Give our no-strings-attached free trial a try to see if it’s for you.

Be the first to comment