ablokhin

January 6, 2023 proved to be a really great day for shareholders of Costco Wholesale Corporation (NASDAQ:COST). In addition to benefiting from general optimism in the market, the company’s share price also increased in response to robust sales data covering the month of December. All things considered, the company is performing exceptionally well in the current environment. But this does not necessarily mean that it makes for an ideal purchase at this time. Because of how shares are priced at the moment, I do still believe that a ‘hold’ rating is appropriate for the company, a rating that is indicative of upside or downside potential that would more or less match the broader market for the foreseeable future.

Mixed but generally favorable results

On January 6th, shares of Costco Wholesale roared higher, and were trading up about 6.5% as of the time of this writing, in response to some rather favorable data management revealed. During the month of December, comparable store sales for the company increased by 5.5% year over year, although the firm did see its e-commerce sales drop by 6.4%. Considering the vast majority of revenue comes from in-store, this data is overwhelmingly positive. In dollar terms, sales totaled $23.80 billion, up from $22.24 billion seen one year earlier. For the trailing 18-week period, comparable store sales were even higher, coming in at 6.1%, with e-commerce sales down a more modest 4.8%. If we ignore changes in foreign currency and gasoline prices, comparable sales growth for the most recent five-week window would have been 7.3% compared to the 7.1% experienced for the 18-week window with the same end date. As for e-commerce sales, those numbers are down 5.4% and 3.4% during their respective windows.

In a vacuum, this data is incredibly positive when you consider the general rhetoric surrounding the retail space. Most notably, on January 4th, news broke that rival retailer Target (TGT) had been downgraded from Overweight to Equal Weight because its outlook has ‘deteriorated meaningfully’ because of a sustained period of comparable sales weakness in general merchandise, negative store traffic expected for the final quarter of 2022, and margin recovery issues associated with the COVID-19 pandemic and recent supply chain problems. The same analyst responsible for this downgrade listed Target and Costco Wholesale both as being in the ‘bottom five’ retailers at risk in this environment. So this company-reported data marks a significant change in expectations for investors to ponder.

Although the increase we are seeing in share price is excellent for investors in the company, this does not change my overall view of the firm. In late September of 2022, I wrote an article about the enterprise, detailing how its future looks bright from a profit and cash flow perspective. Having said that, I also mentioned that shares were too pricey at the moment. That ultimately led me to rate the company a ‘hold’. And so far, that call has played out fairly well. While the S&P 500 is up 3.8% since the publication of that article, shares of Costco Wholesale are up only 0.4% despite the surge in price experienced on January 6th.

Author – SEC EDGAR Data

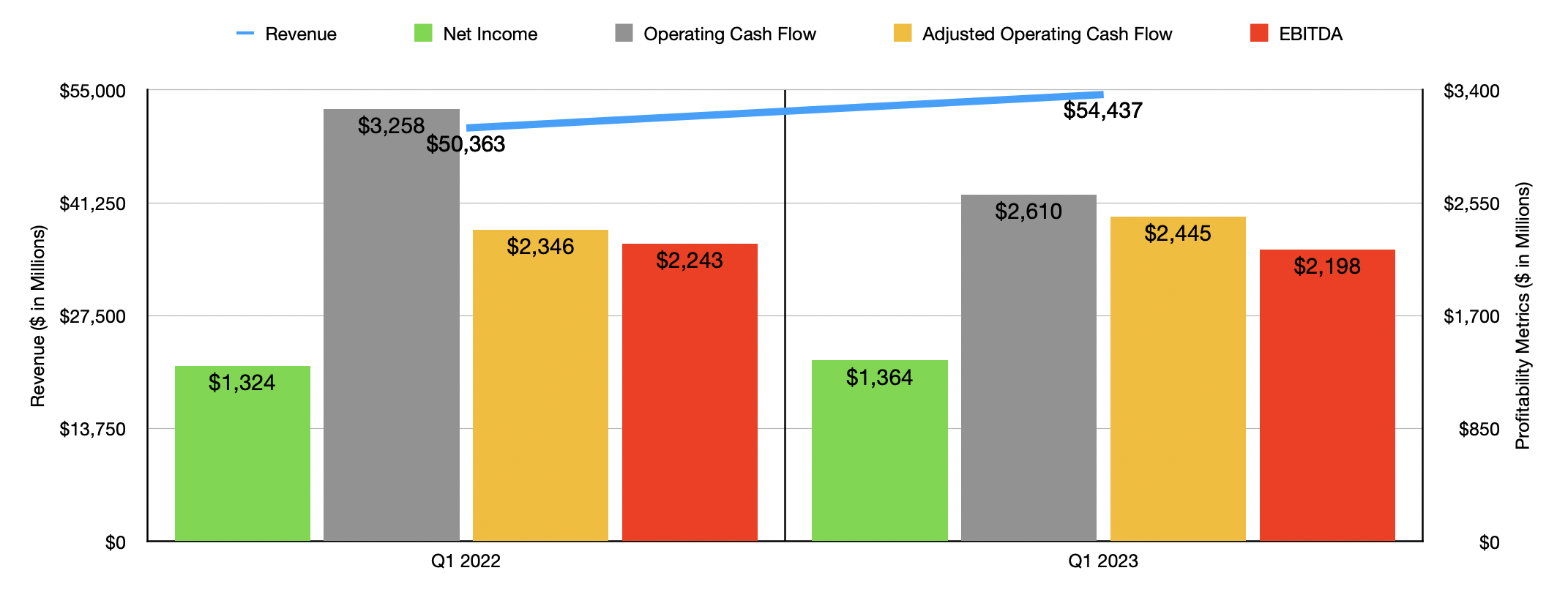

Of course, the past is the past. The bigger question for investors is whether the picture now warrants a revision in my own guidance. Truthfully, I would say that the answer is no. To see what I mean, we need only cover data reported for the first quarter of the company’s 2023 fiscal year. Yes, sales did come in higher year over year, with revenue of $54.44 billion translating to a year-over-year increase of 8.1%. Even though e-commerce sales were down 4% year over year, with that decline coming in at only 2% if we ignore foreign currency and gasoline price fluctuations, overall comparable sales for the company were up. Regardless of foreign currency and gasoline price fluctuations, comparable sales were up 7% year over year. The company also benefited from a 7% increase in paid membership at its locations, as well as from a modest increase in the renewal rate it charges to customers.

With the rise in revenue, profits for the company also improved. Net income of $1.36 billion beat out the $1.32 billion reported one year earlier. At the same time, operating cash flow did worsen, falling from $3.26 billion to $2.61 billion. But if we adjust for changes in working capital, the metric would have risen from $2.35 billion to $2.45 billion. Over that same window of time, EBITDA experienced a bit of pain, declining from $2.24 billion to $2.20 billion.

Author – SEC EDGAR Data

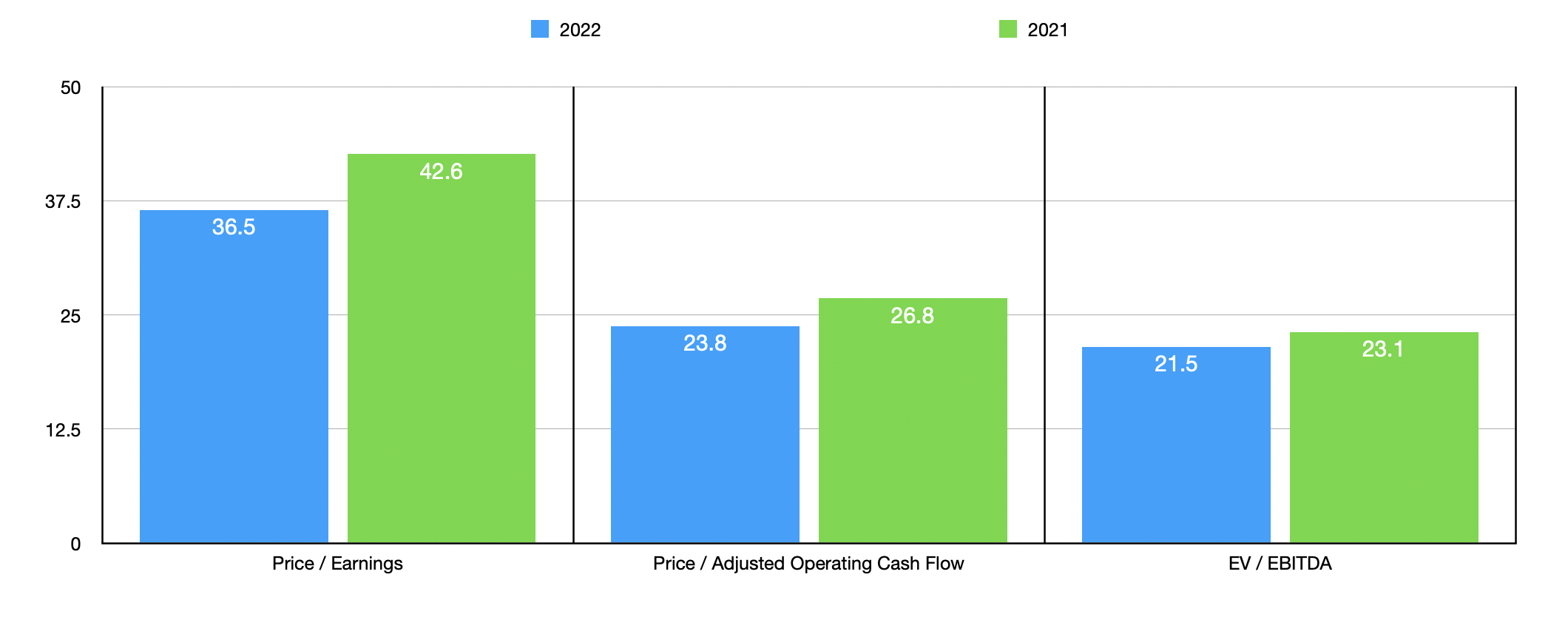

Because management does not offer any significant guidance, and because it is still quite early in the 2023 fiscal year, I do think it would be more sensible to value the company based on data from its 2022 and 2021 fiscal years. Using the data from 2022, the company is trading at a price to earnings multiple of 36.5. That’s down from the 42.6 reading that we get using data from 2021. From 2021 to 2022, the price to adjusted operating cash flow multiple for the firm dropped from 26.8 to 23.8, while the EV to EBITDA multiple declined from 23.1 to 21.5. As part of my analysis, I also compared the company to five similar firms. To be fair, the membership warehouse model really only applies to two of these firms. But the other three are major retailers that vie for customers’ attention, so I believe that including them in the picture is only appropriate. On a price-to-earnings basis, these companies ranged from a low of 7.1 to a high of 45.3. Four of the five firms were cheaper than Costco Wholesale. Using the price to operating cash flow approach, the range was from 3.8 to 20.9. And when it comes to the EV to EBITDA approach, the range was from 3.1 to 16.7. In both cases, our prospect was the most expensive of the group.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| Costco Wholesale Corporation | 36.5 | 23.8 | 21.5 |

| Walmart (WMT) | 45.3 | 17.1 | 16.7 |

| BJ’s Wholesale Club Holdings (BJ) | 19.1 | 13.2 | 11.1 |

| Target | 21.9 | 20.9 | 11.5 |

| The Kroger Co (KR) | 14.3 | 7.1 | 5.9 |

| Albertsons (ACI) | 7.1 | 3.8 | 3.1 |

Takeaway

I fully understand the investor optimism centered around Costco Wholesale at this time. The fact of the matter is that the company is doing very well in what can only be considered a difficult environment. Although some of its profitability metrics are mixed, the adjusted operating cash flow multiple is doing quite well and sales continue to climb at a nice clip. But none of this means that the company makes for a great prospect to consider at this time. Given how pricey shares look, I do think that upside from here is truly limited. And because of that, I cannot in good conscience give the firm a rating any higher than a ‘hold’ at this time.

Be the first to comment