FG Trade

If there’s a single lesson that life teaches us, it’s that wishing doesn’t make it so.― Lev Grossman

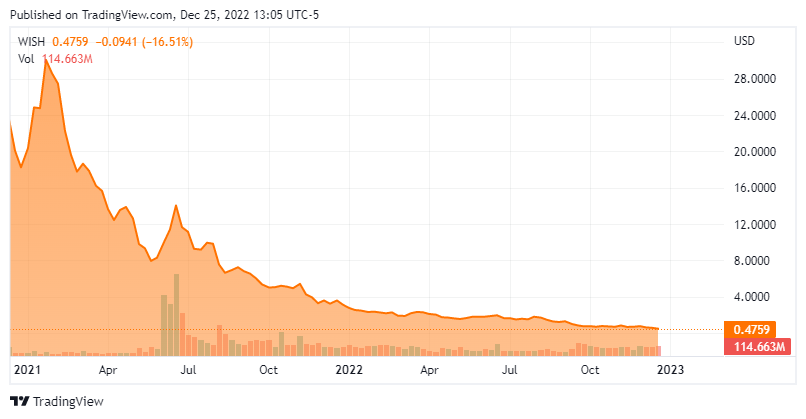

Today, we put ContextLogic, Inc. (NASDAQ:WISH) in the spotlight for the first time. This e-commerce play came public in late 2020 during a huge boom in the IPO space and was founded by ex Yahoo and Google executives. As can be seen below, the stock has been a disaster for shareholders since. However, the shares now sell for a substantial discount to the net cash on its balance sheet. Value Trap or buying opportunity? An analysis follows below.

Seeking Alpha

Company Overview:

ContextLogic, Inc. is headquartered in San Francisco. The company operates Wish, an ecommerce platform that connects users to merchants and other provides marketplace and logistics services to clients. The stock currently trades around fifty cents a share and sports an approximate market capitalization of $350 million.

The company sells novelty and unique items to bargain conscious consumers from merchants, mainly in China as well as other emerging markets. ContextLogic saw sales surge during the pandemic, when most of the population in the western world was either locked down or working from home.

Third Quarter Results:

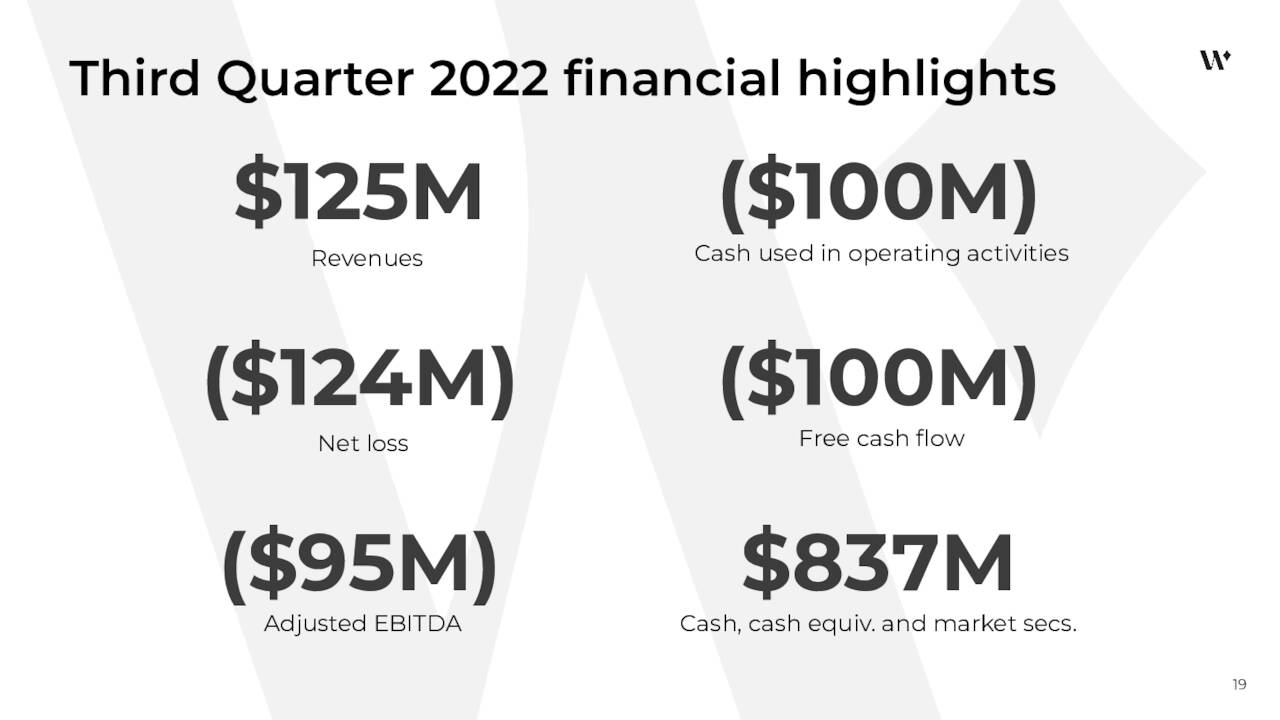

ContextLogic posted third quarter numbers on November 9th. They were disappointing on the revenue side. The company posted a GAAP loss of 18 cents a share, which was a few cents a share above the consensus. However, revenues fell 66% on a year-over-year basis to $125 million, roughly $30 million below the consensus. Core Marketplace sales came in at just $40 million, down 78% from the same period a year ago. ProductBoost revenues were $11 million, off 70% from 3Q2021.

November Company Presentation

Analyst Commentary & Balance Sheet:

Since the company’s last earnings report, Credit Suisse has reduced its price target to $5.70 a share from $7.20 while maintaining its Outperform rating on the stock. UBS cut their price target in half to just .80 a share while maintaining a Neutral rating on the equity, and Citigroup initiated the shares with a Sell rating and a 50 cent a share price target.

November Company Presentation

Approximately seven percent of the outstanding float in WISH is currently held short. Numerous insiders have been frequent and consistent sellers of the stock since lock ups expired. So far, they have disposed of approximately $10 million worth of stock in aggregate here in the fourth quarter to date. After posting a massive loss of $121 million for the third quarter, the company still had just north of $835 million of cash and marketable securities on its balance sheet. The company had negative free cash flow of $100 million in the third quarter, which was actually an improvement from negative free cash flow of $344 million it posted in 3Q2021.

Verdict:

The current analysis firm consensus has the company losing roughly 55 cents a share in FY2022 as sales shrink over 70% to just over $590 million. Sales growth in the high single digits is projected in FY2023, but ContextLogic is expected to post similar losses for FY2023.

Seeking Alpha

The company debuted on the market in December 2020 when IPOs raked in $20 billion for December, an all-time record for the month. Thanks to cheap money from the Federal Reserve, IPO volume would continue to be strong through the summer of 2021. WISH raised just over $1 billion at the time of its IPO giving it a valuation of $17 billion at $24.00 per share. At the time, the company had 100 million monthly active users or MAUs worldwide, selling approximately two million products daily on its e-commerce platform. At the time both JP Morgan and Oppenheimer placed Buy ratings on the stock with identical $30 price targets.

Seeking Alpha

E-commerce retailer Poshmark (POSH) came public soon after ContextLogic, and also has been a disaster for its original shareholders. ContextLogic delivered revenue growth (but not up to original projections) for its first two quarters on the market, but by 2Q2021, revenues started to fall on a year-over-year basis, badly missing projections. As the pandemic ebbed, worldwide installations of its app fell by 13% sequentially in 2Q2021 and the average time spent on the Wish platform dropped by 15% during the same period. WISH also ceased being a ‘meme‘ stock around the same time.

Management turnover also starting to occur around that time, with the company losing its CFO in July. The CEO, who had nearly 60% of the voting shares when the company came public, announced he was stepping down a few months later but would remain on the board of directors. The company announced a new CEO in February of this year, who was CEO of Foot Locker’s (FL) Europe, Middle East & Africa businesses. The company’s previous CEO left the board this summer. ContextLogic then put in place its third leader since going public this September, and he was announced as an interim CEO.

November Company Presentation

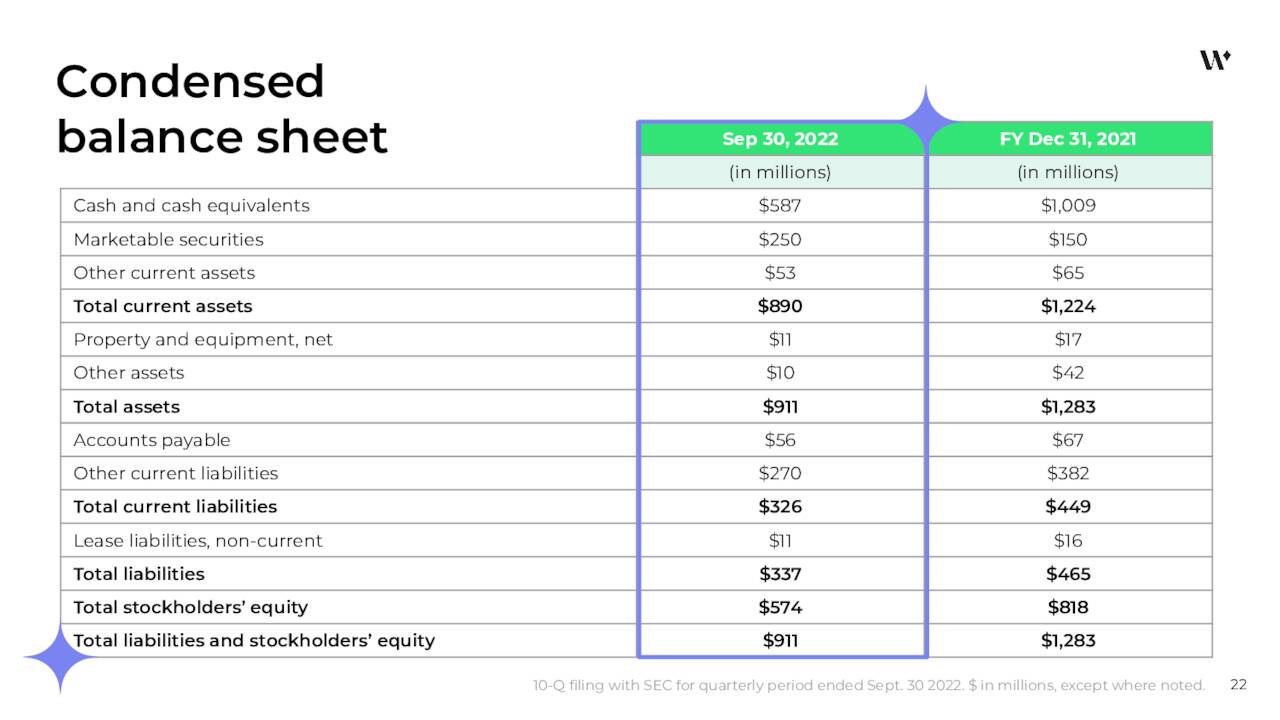

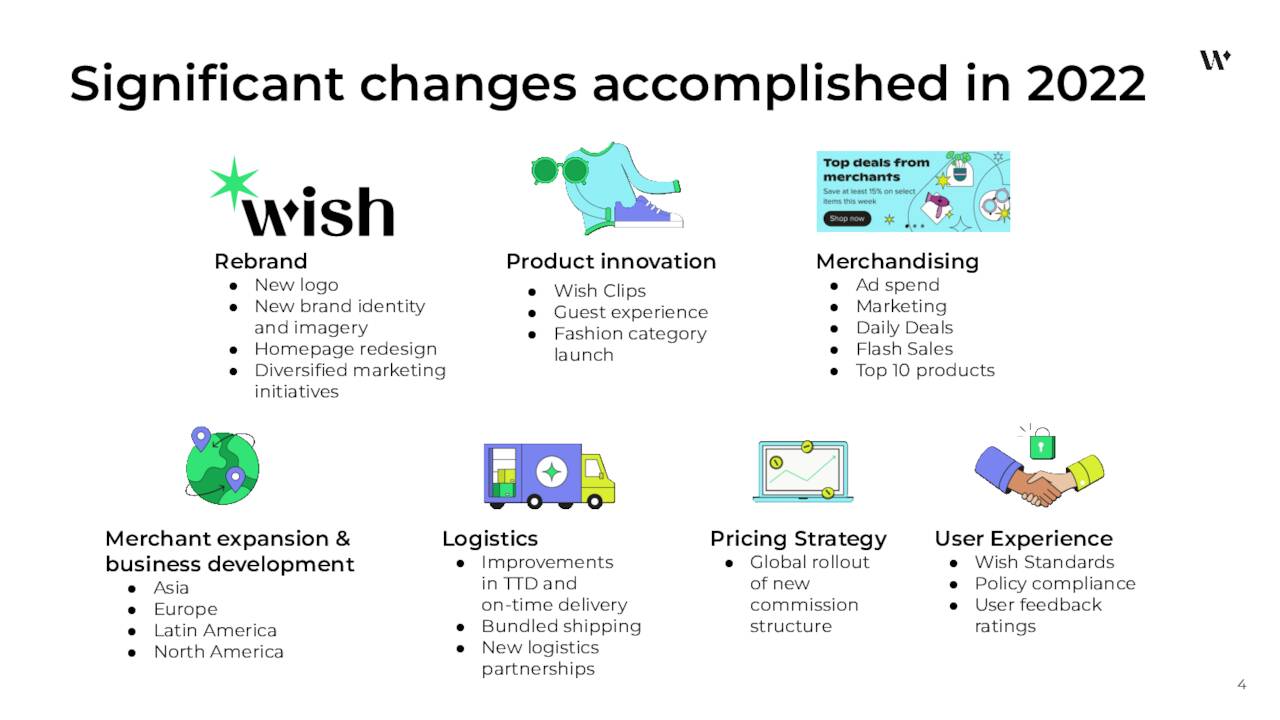

The company has been plagued with slumping demand for its cheap products, the inability to consistently control costs, and a continued large quarterly burn rate. In addition, the firm has been challenged by quality issues and supply chain problems through most of its history as a public company. ContextLogic has made some improvements since coming public, including adding merchant rewards, incorporating live and video shopping, and redesigning its homepage. Management has made some progress reducing the amount of customer refunds and order cancellations (above). The stock also trades for substantially below the value of its cash holdings.

November Company Presentation

That said, it is hard to recommend even a small investment in ContextLogic at this time until investors see some more progress reducing quarterly losses and a new CEO is in place. Therefore, we are passing on recommending even a small ‘watch item‘ position in this name, trading at a significant discount to its cash value.

To grant all a man’s wishes is to take away his dreams and ambitions. Life is only worth living if you have something to strive for. To aim at.“― P.B. Kerr

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment