inarik/iStock via Getty Images

CompX International Inc. (NYSE:CIX) is expecting demand in its marine components business segment. In addition, in a recent quarterly report, management noted EBT growth in both business segments. In my view, further successful management of the ongoing supply chain disruptions and new stock purchase programs would imply a valuation of $24.9 per share. Competitors from China and lack of sufficient internationalization could represent risks, however the company appears cheap at its current market price.

CompX International Delivers Net Sales Growth And EBT Growth In Both Business Segments

CompX International is a North American company dedicated to the manufacture and marketing of security components with various uses, applied to means of transportation, institutional or office furniture, health treatments, the postal sector, and a series of industrial operations.

The company also works in the production of stainless steel, gauges for industrial applications, accelerators, wake improvement systems, and adjustment tabs for finished products and medium-term phases in various industrial areas, mainly for the marine industry.

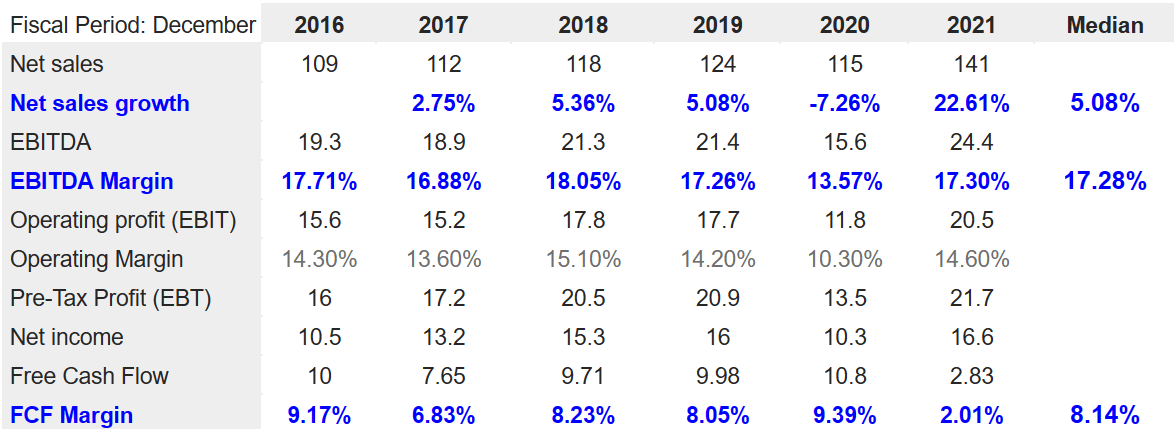

The two large segments into which the company divides its business model are marine components and security products. I believe that CompX is a good read considering that both business segments deliver net sales growth, and the income before income taxes growth is also positive.

Source: 10-Q

Strong Demand In The Marine Components Segment, And Analysts Expect Median Net Sales Growth Of 5.08%

I believe that after the recent words from management in the last quarterly report, having a look at CompX appears to be a must. Management noted strong demand for the products of both segments, and noted that even with competitive labor markets, the company maintained balanced staffing levels, and expects more demand mainly in the Marine Components segment. With this in mind, I would be expecting stable FCF margins in the coming years.

During the first nine months of 2022, we have experienced strong demand at both our segments. We operated our manufacturing facilities at elevated production rates during the first nine months of the year in line with our demand. While labor markets continue to be competitive in each of the regions in which we operate and labor costs continue to rise, we have been able to achieve and maintain more balanced staffing levels aligned with current and forecasted demand, particularly at our Marine Components segment. Source: 10-Q

I am quite optimistic about the company’s efforts with regards to ongoing supply chain disruptions. In my view, if the company continues to successfully manage these disruptions, future FCF margins will likely improve.

Certain of our supply chains, particularly for commodity raw materials, have stabilized while other supply chains remain challenging, and current global and domestic supply chain disruptions continue to impact sourcing certain of raw materials and components due to increased lead times, shortages and transportation and logistics delays. Thus far, we have been able to manage through these disruptions with minimal impact on our operations. Source: 10-Q

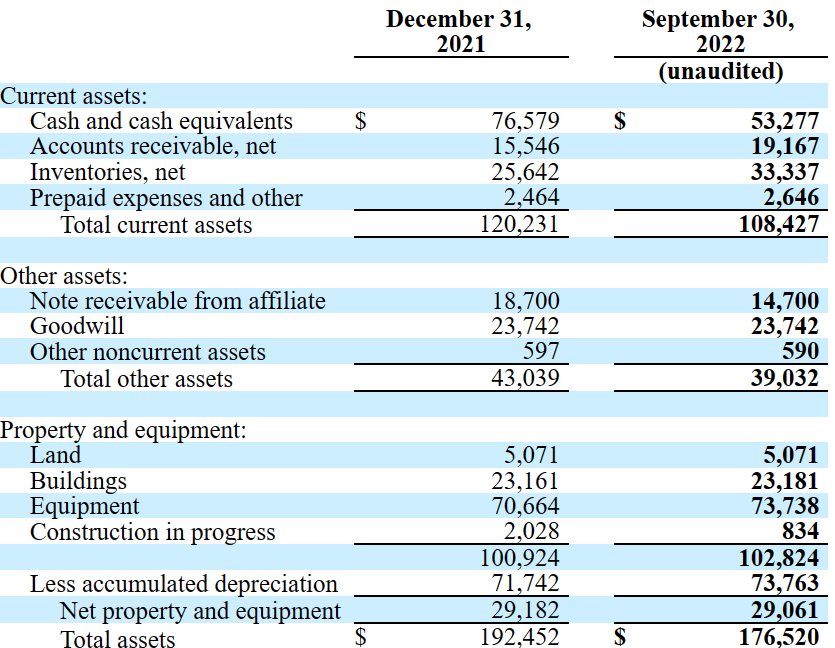

The results obtained for December 2021 included a net sales of $141 million with a net sales growth of 22.61%, EBITDA of $24.4 million with an EBITDA margin of 17.30%, and an operating profit of $20.5 million accompanied by an operating margin of 14.60%. In addition, the pre-tax profit was $21.7 million, with a free cash flow of $2.83 million and a FCF margin of 2.01%. On the other hand, net income closed at $16.6 million. I used some of the following financial stats in my financial models.

Source: marketscreener.com

Sound Financial Situation

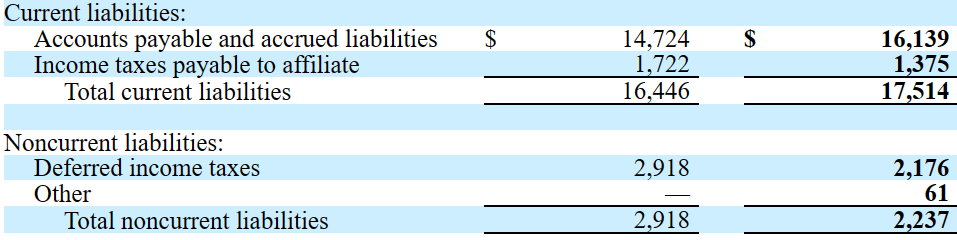

As of September 30, 2022, CompX reported cash of $53 million, with accounts receivables worth $19 million and inventories of $33 million. Total current assets stand at $120.231 million, much more than the total amount of liabilities.

With notes receivable worth $18.7 million and goodwill of $23.742 million, CompX reported total other assets of $43.039 million, buildings of $23.161 million, and equipment worth around $70.664 million. Finally, total assets stand at $192.424 million, close to 10x the total amount of liabilities.

Source: 10-Q

The liabilities include accounts payable worth $14.724 million, along with income taxes of $1.722 million and total current liabilities of $16.446 million. In addition, the deferred income taxes were around $2.918 million. Without financial debt, in my view, most investors wouldn’t be worried about the obligations reported by CompX.

Source: 10-Q

Further Demand In The Marine Components Segment Could Lead To A Valuation Of Close To $24.9

Under normal conditions, I believe that further demand in the Marine Components segment will likely help reduce any eventual reduction in the FCF margins in the Security Products business segment. In this regard, the company offered further explanation in the following words.

Thus far, the softening in demand Security Products has experienced in the transportation market has been more than offset by continued strong demand in other markets, particularly the government security and office furniture market.

Marine Components demand remains strong and with the implementation of price increases for the new model year at the beginning of the third quarter, we expect to maintain gross margins comparable to 2021 at the segment during the fourth quarter. Source: 10-Q

Besides, I would expect that the company’s stock repurchase program will likely bring the interest of new investors. As a result, I believe that the cost of equity could decrease, which may bring lower cost of capital, and may enhance the fair price.

At September 30, 2022, we have 523,647 shares available for repurchase under a stock repurchase program authorized by our board of directors. Source: 10-Q

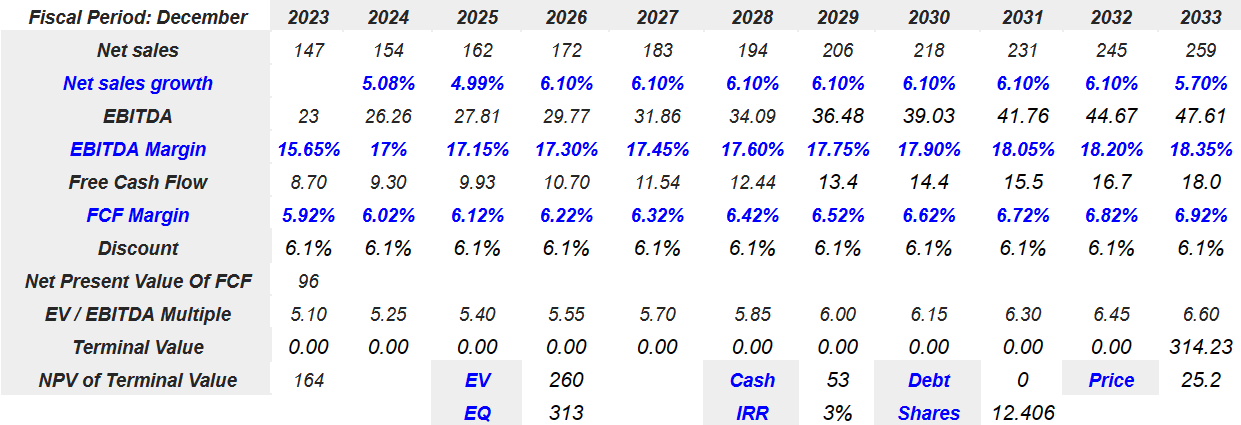

Under the previous conditions, I assumed that CompX would deliver 2033 net sales growth of 5.70%, EBITDA of $47.61 million, and an EBITDA margin of 18.35%. In addition, 2033 free cash flow would stand at $18 million with a FCF margin of 6.92%.

Source: Author’s Financial Model

If we assume a discount of 6.1%, the net present value of FCF would stand at $96 million. Besides, with an EV/EBITDA multiple of 6.60x, the terminal value would be $314.23 million accompanied by a NPV of terminal value of $164 million. The enterprise value would stand at $260 million with an equity valuation of $313 million, a fair price close to $24.9, and an IRR of 3%.

Lack Of International Expansion Could Imply A Valuation Close To $15.5 Per Share

According to its own statements in the last annual report, the company obtains more than 10% of its profits from a single contractor, which indicates lack of diversification. Besides, lack of expansion in the international markets manifests certain limitations of its business model. Without exposure to other markets, in my view, an economic recession in the United States would hit the company’s financial figures quite a bit.

Regarding the trade of products for marine installations, CompX appears to experience a certain bonhomie in the market, which, although it is still competitive especially at a regional level where small producers have very low shipping costs, does not have the same levels of competition that it has in the security product sector. In my view, this is mainly due to the immersion of the Chinese industry in the local market as well as the introduction of products from industries of different countries with low production costs, which achieve the trade of similar products, and directly alter the arrival of CompX.

For this reason, I believe that it is essential that management innovates by increasing its licenses, undoubtedly a strong point to demonstrate the value and quality that distinguishes it from this type of products from cheaper economies. In any case, competition currently means a clear risk factor for the company’s operations, which, although it is not radically affected at this time, must maintain its quality standards, and allocate budgets to research to not only sustain but also increase and diversify its client portfolio.

The inability to reach out to new clients and the lack of skills to keep current commercial agreements active are also first-hand risk factors in terms of the development of the company’s business model, since it is directly related to the productive capacity and the flow of its products. Under this scenario, I assumed that CompX would fail to maintain certain agreements active, which may bring lower revenue growth than expected.

On top of this, we can also add the obvious variation in the price of raw materials as well as transportation costs and the unpredictability that is currently present in the global economy. The company discussed these risks in the last quarterly report.

In addition, we are experiencing increased production costs including higher labor and shipping costs and, although prices for certain raw materials have begun to stabilize, costs of many of the raw materials we use including zinc, brass, stainless steel and aluminum remain elevated above pre-pandemic levels. Source: 10-Q

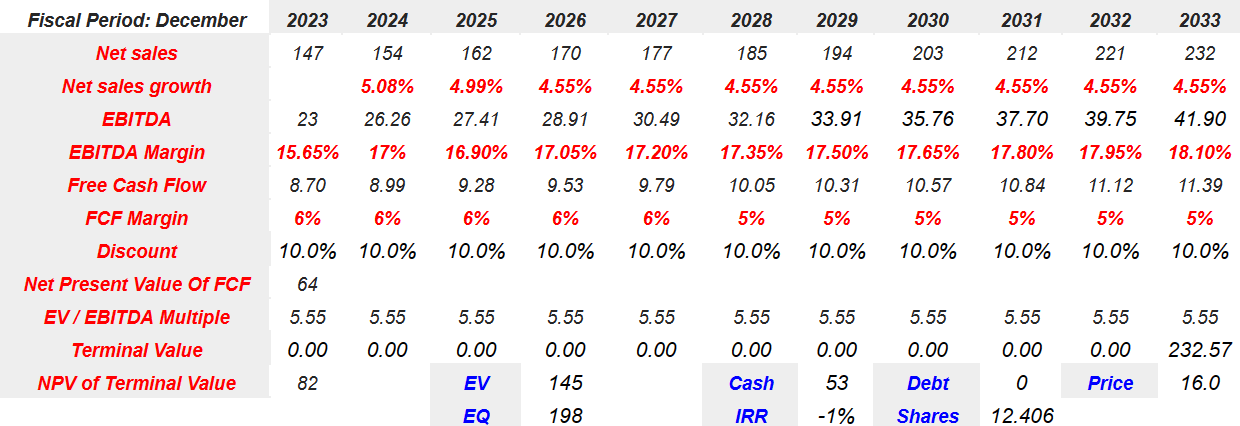

Under the previous risks, I expected net sales of $232 million with net sales growth of 4.55%. Besides, I assumed 2033 EBITDA of $41.90 million with an EBITDA margin close to 18.10%. The free cash flow will likely be around $11.39 million accompanied by a FCF margin of 5%.

Source: Author’s Financial Model

If we include a 10% discount, the net present value of future FCF would stand at $64 million. Also, with an EV/EBITDA multiple of 5.55x, the terminal value would be around $232.57 million, and the NPV of terminal value would be $82 million. Besides, I obtained an enterprise value of $145 million, an equity valuation of $198 million, and a fair price close to $15.5.

Conclusion

CompX International is experiencing significant demand in marine components, and appears to be managing the ongoing supply chain disruptions well. In my view, under normal conditions, I would expect further free cash flow growth and an implied valuation close to $24.9 per share. I obviously envision risks from competitors from China and lack of sufficient internationalization. With that, in my view, CompX appears quite undervalued.

Be the first to comment