MediaProduction

After the run we’ve had in the markets, I believe we should start to see the more defensive option-income funds perform relatively better over the more aggressive leveraged closed-end funds (“CEFs”), many of which have had strong advances over the past month and have moved to high market premiums.

That assumes that the broader markets take a breather here after a surprisingly bullish August so far that has confounded many bears who expected further downside. But with a strong jobs report and lower inflation numbers from CPI and PPI earlier this week, investors have jumped back into the markets full force.

Or maybe it’s been more of a dumb money retail crowd clamoring to put cash back to work while institutions are forced to cover their shorts and hedges. Whatever the reason, I thought it might be productive to see what has worked among my Actionable Buy and Buy rated equity CEFs and exchange-traded funds (“ETFs”) from the Equity CEF/ETF Portfolio spreadsheet and what might work better if the next couple months in September and October live up to their more notorious bearish history.

Aggressive/Leveraged CEFs Or Defensive Option-Income CEFs Now?

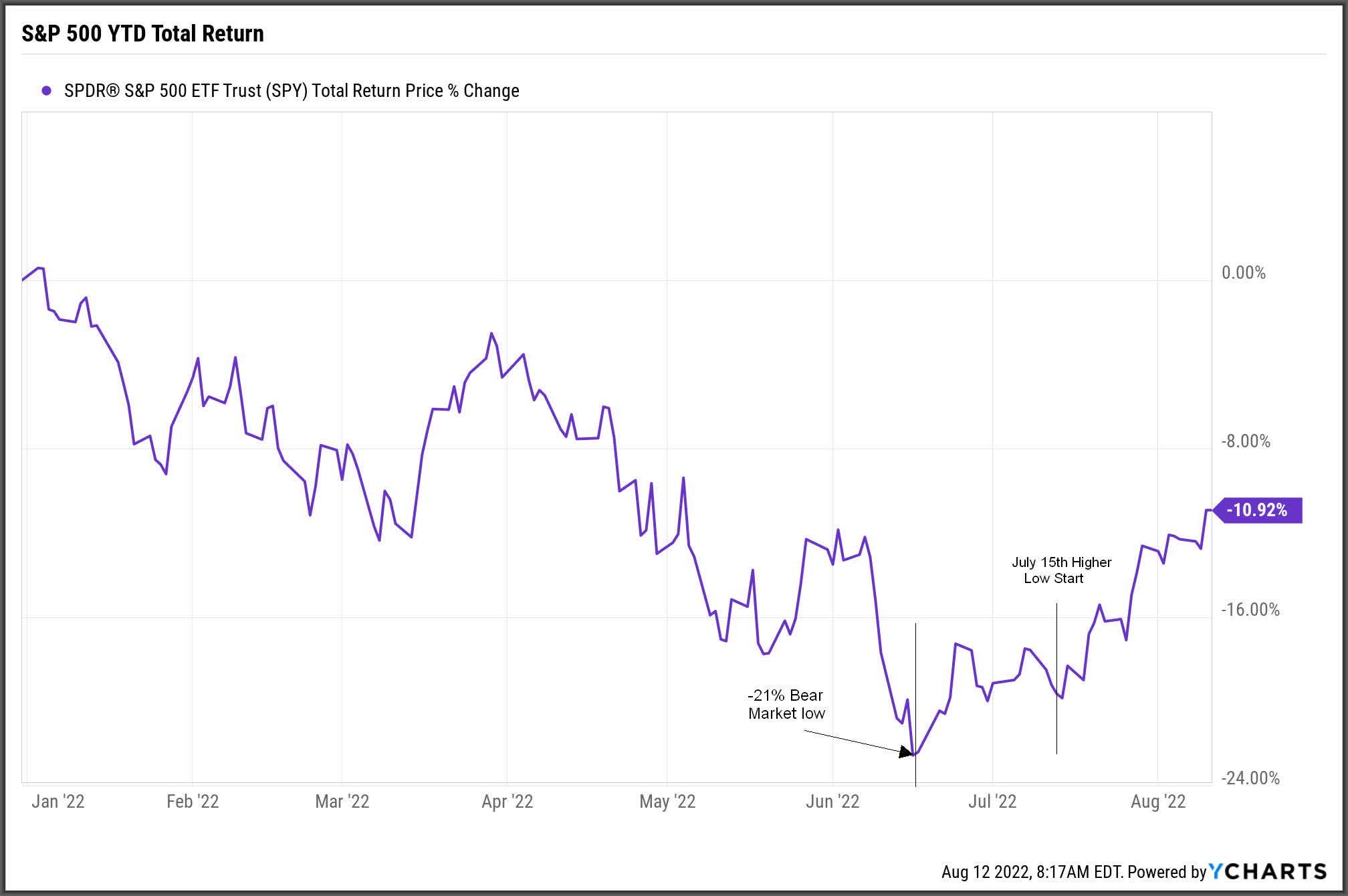

But let’s first see how these CEFs and ETFs have performed in a bull market environment which has seen the S&P 500 (SPY), $419.99 current market price, recover well over half of its losses YTD.

Ycharts

In this exercise, I’m going to use July 15th as a starting point since not only did that mark a recent low point in the markets (though a higher-low from mid-June), but it also coincided with the third Friday of the month, which is an option rollover day. That is, July options expired on July 15th while August options were initiated on July 15th and will expire Aug 19th.

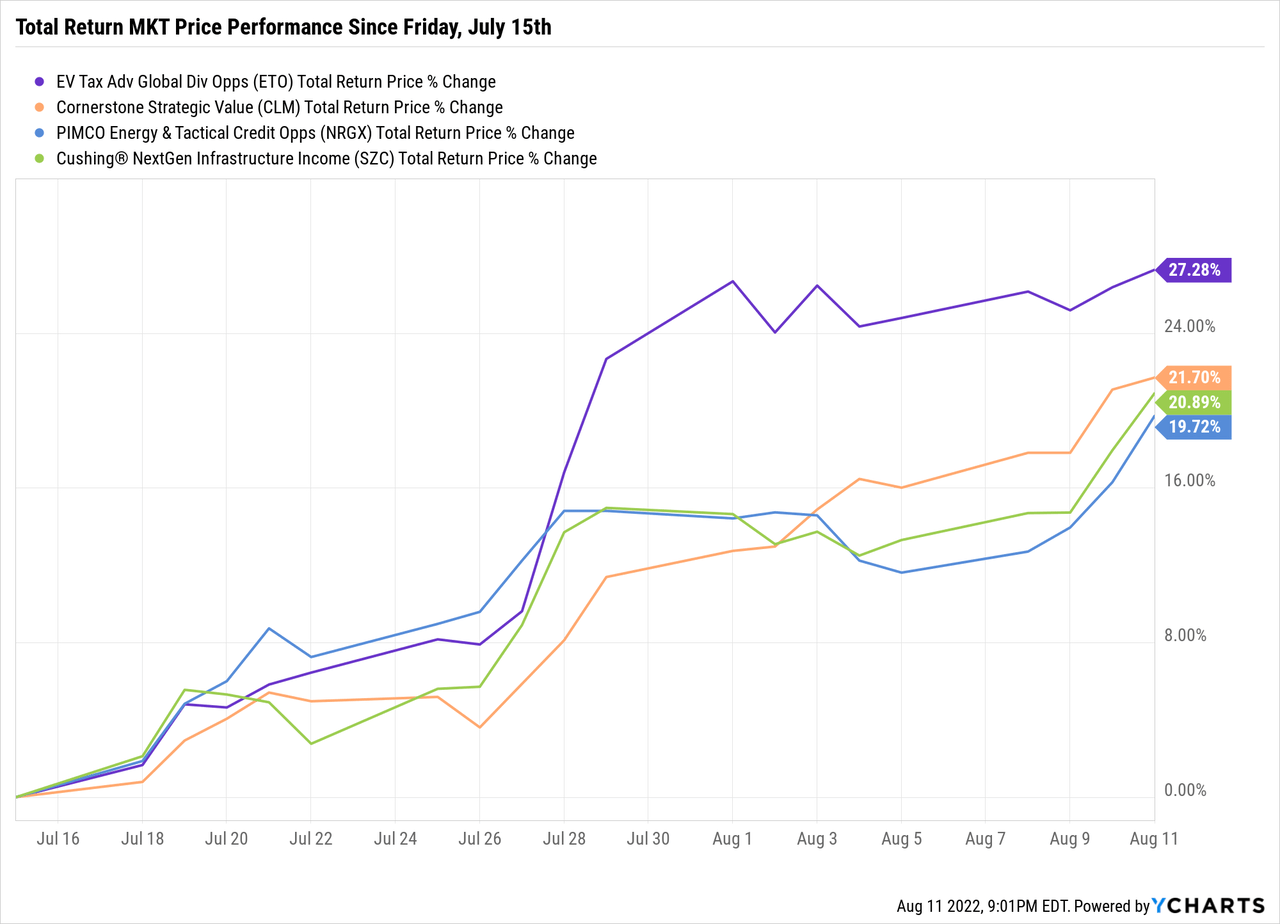

The first four funds are the of the aggressive and/or leveraged type CEFs and they include the Eaton Vance Tax-Advantaged Global Dividend Opportunities Fund (ETO), $28.80 current market price, the Cornerstone Strategic Value fund (CLM), 10.81 current market price, the PIMCO Energy & Tactical Credit Opportunities fund (NRGX), $15.30 current market price and the Cushing NextGen Infrastructure Income fund (SZC), $44.58 current market price.

All of the funds that will be shown below are rated either a Buy or Actionable Buy in the Equity CEF/ETF Portfolio and they all represent medium to large positions of mine, though some like ETO, have been sold down recently.

Ycharts

Note: I also have a large position in the Cornerstone Total Return fund (CRF), which is up a similar return as CLM at +20.3%. The Cornerstone funds CLM & CRF are not leveraged but I do consider them aggressive positions

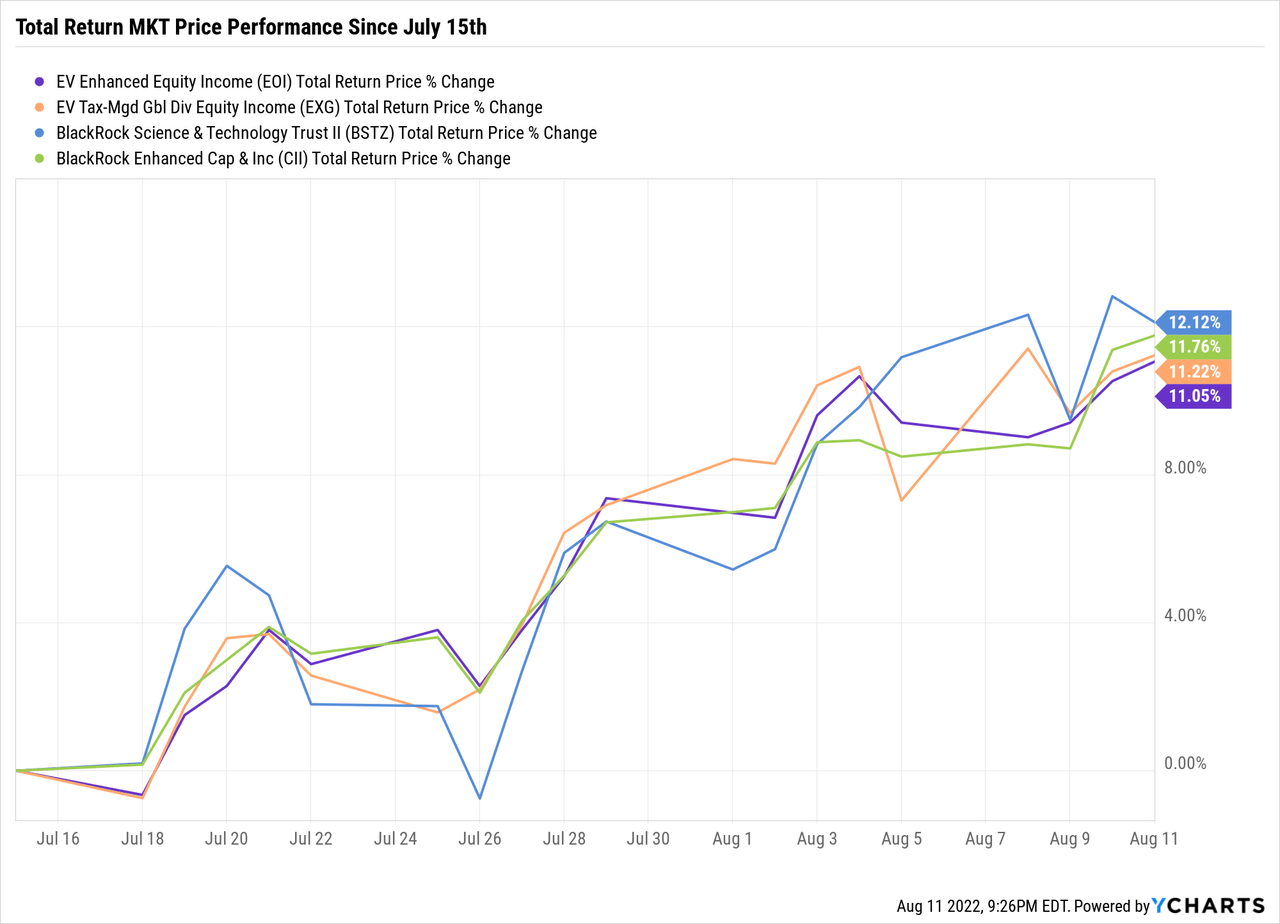

The second portfolio grouping do use option-writing but are what I would call the moderately defensive option-income CEFs and they include the Eaton Vance Enhanced Equity Income fund (EOI), $16.90 current market price, the Eaton Vance Tax-Managed Global Diversified Equity Income fund (EXG), $8.96 current market price, the BlackRock Science and Technology Trust II (BSTZ), $22.46 current market price and the BlackRock Enhanced Capital & Income fund (CII), $20.16 current market price.

Ycharts Ycharts

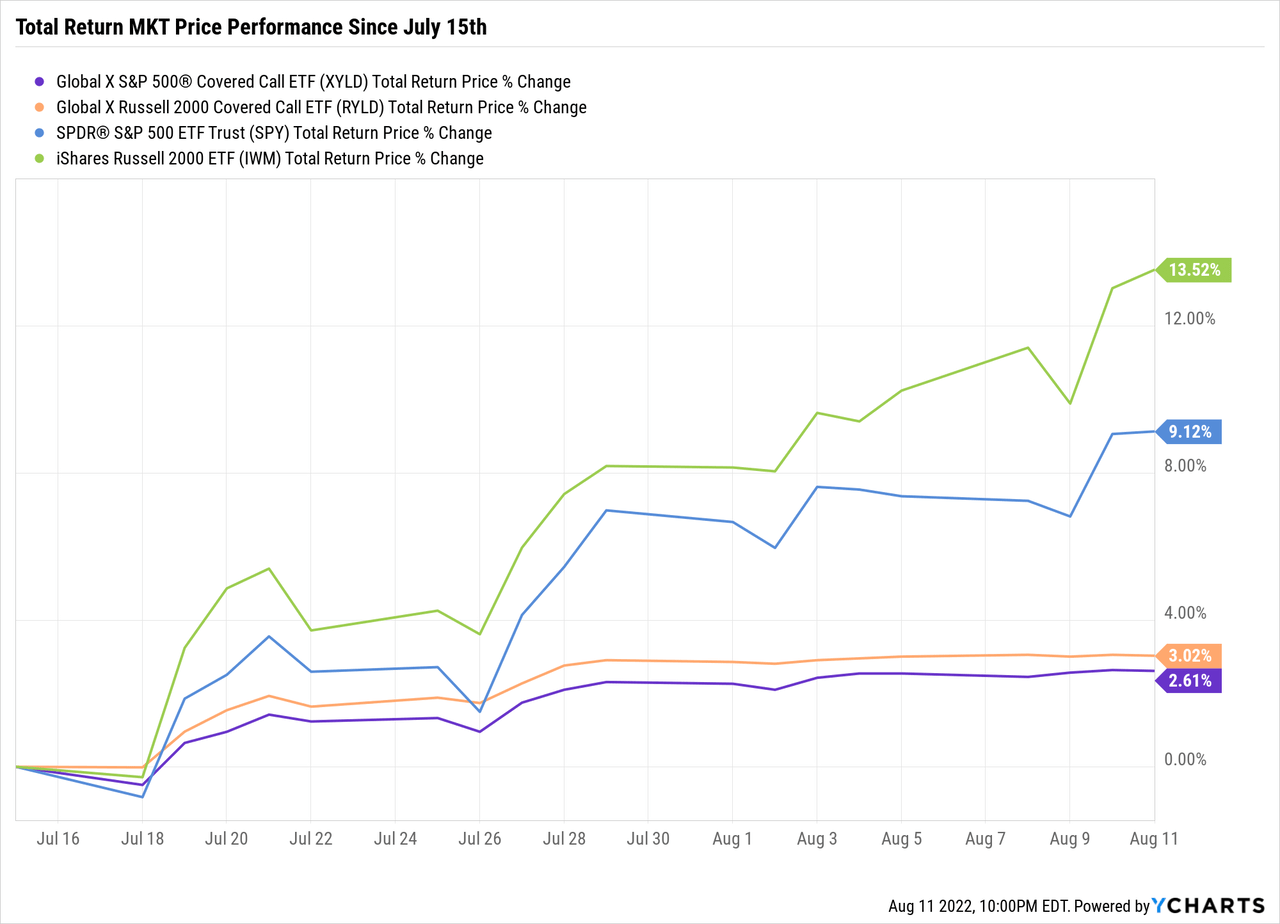

Finally, I wanted to show you the two Actionable Buy ETFs I have a large position in, the Global X S&P 500 Covered Call ETF (XYLD), $44.03 current market price and the Global X Russell 2000 Covered Call ETF (RYLD), $21.21 current market price.

For comparative purposes, I’ve also included the benchmarks for XYLD, the S&P 500 (SPY) and for RYLD, the Russell 2000 Small Cap ETF (IWM).

Ycharts

As you can see, the returns of XYLD and RYLD over the past month or so pale in comparison to their benchmarks, SPY and IWM. This is what can happen when funds that sell index options At-The-Money on 100% of their portfolio value, do so at a market low which also happened to coincide with a monthly option rollover.

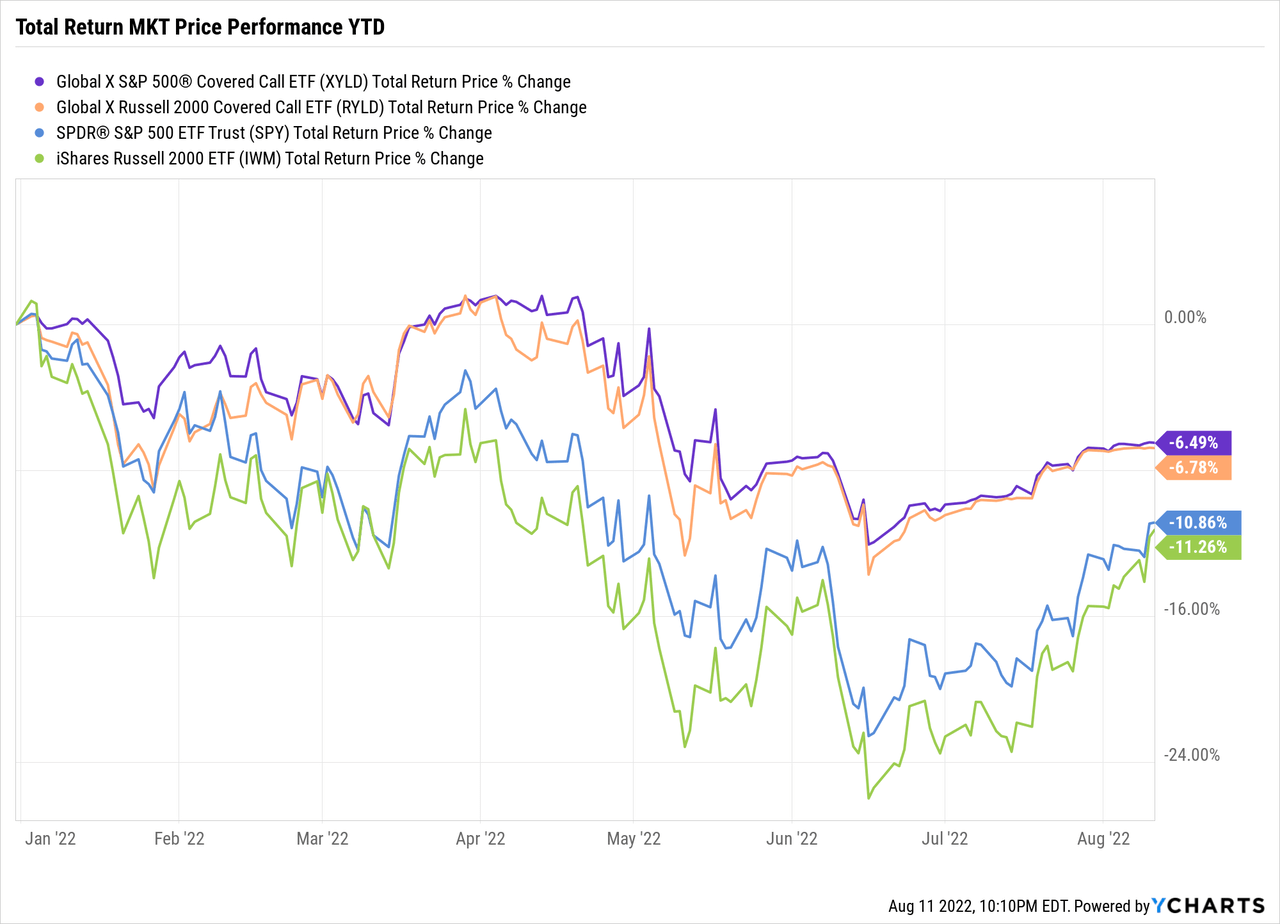

Though the returns for XYLD and RYLD are minimal since July 15th, on a YTD basis, XYLD and RYLD are still outperforming their benchmarks, though the margin has narrowed quite a bit.

Ycharts

But this is why you need to have a diversified portfolio of equity CEFs and ETFs that can outperform during strong market periods as well as flat to even bear market periods.

All of the funds mentioned above can be seen in a spreadsheet if you click on the link in the latest Equity CEF/ETF Portfolio update from July 29th or just click here:

Conclusion

I believe the low-hanging fruit of this market advance, and probably the high-hanging fruit as well, have just about been picked clean and yesterday’s reversal, which was tied to a weakening bond market, may signal a change in leadership from the aggressive/leveraged CEFs to the more defensive option income CEFs.

And considering the valuation changes we’ve seen over the past month with many of the aggressive/leveraged CEFs rising to double-digit premiums, like ETO at a 13.7% market price premium and other buy rated funds like the Calamos Global Dynamic Income fund (CHW), $7.78 current market price at a 11.6% market price premium and the Liberty All-Star Growth fund (ASG), $6.76 current market price, at a 13.5% market price premium, I’m more inclined to sell down some of these positions than add to them.

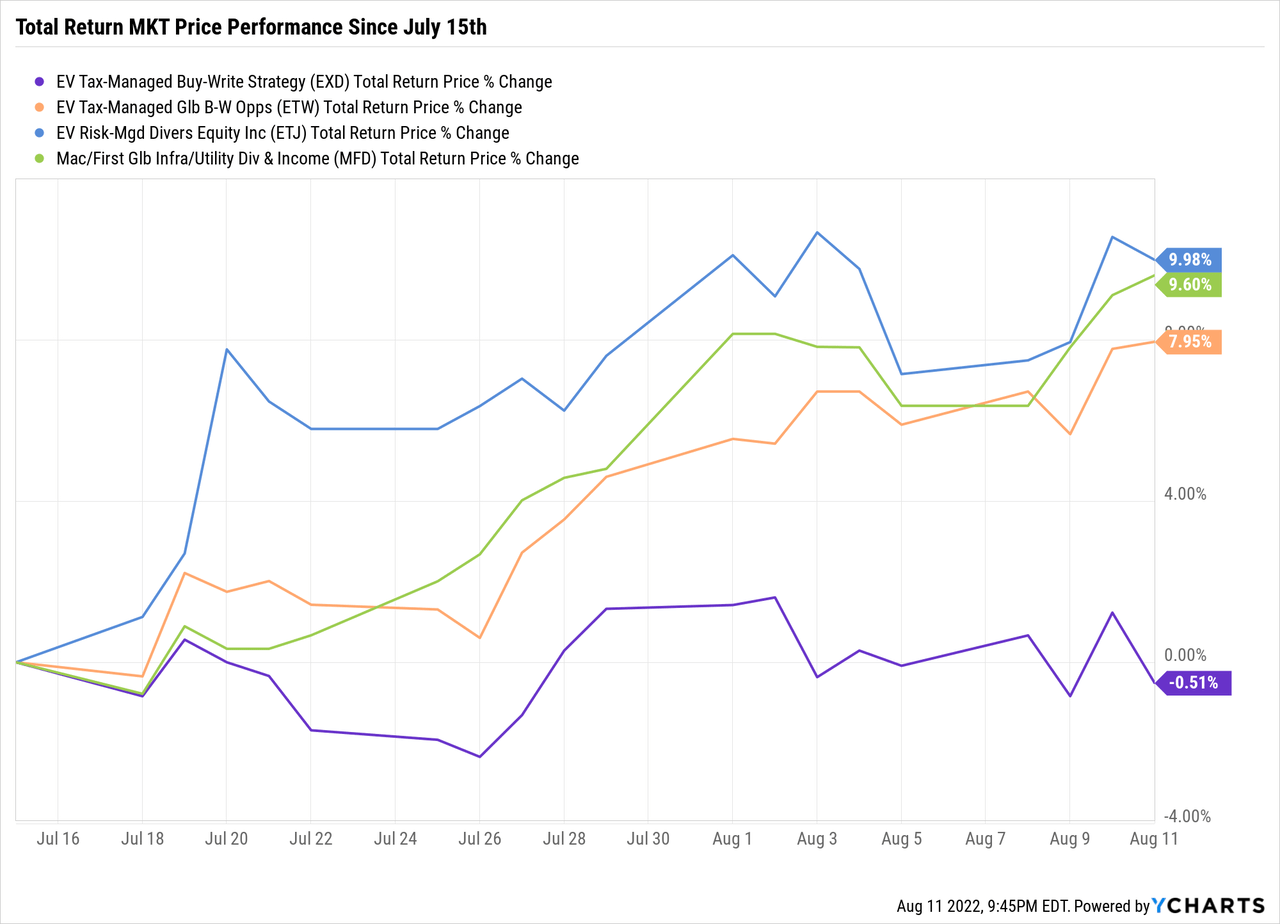

What would I be looking at now if the next two months prove to be more difficult? I still think the Eaton Vance Tax-Managed Buy-Write Strategy fund (EXD), $10.56 current market price, is relatively underpriced and if you have a taxable account, EXD offers an 8.1% annualized yield that is essentially tax-free due to the large ROC in its distributions.

EXD has virtually the same stock portfolio and the same option strategy as the Eaton Vance Tax-Managed Buy-Write Opportunity fund (ETV), $15.57 current market price, a much larger option-income CEF that trades at a 14.0% market price premium while the much smaller EXD trades at a 2.9% market price premium.

It doesn’t take many shares to move EXD down, and that’s what seems to have happened after a strong move in June, but considering how defensive the fund is, you really don’t take much of a risk in EXD in case we go into a down period.

And if you can take advantage of the ROC in the distributions, due to EXD’s accumulated losses before it changed its strategy in February of 2019 to an ETV clone, you could generate tax-equivalent yields as high as 11% depending on your tax-bracket.

Note: ROC is considered non-dividend income on 1099’s and thus, is not taxable in the year received though you are supposed to lower your cost basis by the ROC amount. Thus, ROC is deferred until you sell the position

I can’t say where the markets go over the next month or two, which also includes a Federal Reserve meeting on September 20th-21st, but if history is any guide, I think it makes sense to re-balance portfolios into the more defensive option-income CEFs that trade at reasonable valuations still.

Be the first to comment