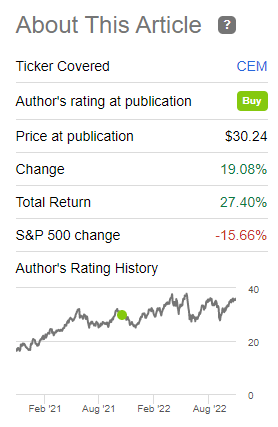

We wrote about ClearBridge MLP and Midstream Fund (CEM) in the past, assigning it a Buy rating on the back of the improvements in the underlying asset class and the CEF’s holdings. The fund has provided a 27% total return in the period, with the S&P 500 down -16% during the same time-frame:

Author Rating Performance (Seeking Alpha)

It has not been a linear ride for CEM, with significant volatility along the way. Expect more as we are heading into the end of 2022.

We believe we are currently witnessing a bear market rally, with another leg down to develop in the overall equity market shortly. While CEM represents the MLP asset class which is on the mend, it will not escape the overall market move. We expect a dip in CEM, which will represent a better entry point for the fund.

Rising Leverage Costs

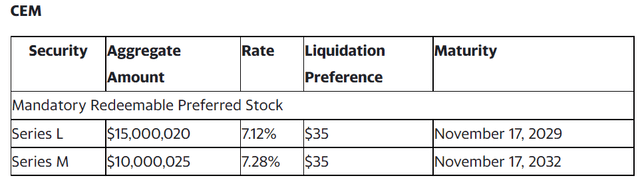

A recent development for the CEF has been the raising of new leverage:

NEW YORK, November 18, 2022–ClearBridge MLP and Midstream Fund Inc. (NYSE: CEM), ClearBridge Energy Midstream Opportunity Fund Inc. (NYSE: EMO) and ClearBridge MLP and Midstream Total Return Fund Inc. (NYSE: CTR) (each a “Fund” and together, the “Funds”) announced today that each Fund completed private placements of fixed-rate Mandatory Redeemable Preferred Stock (“MRPS”) on November 17, 2022, raising additional capital for each Fund. Net proceeds from the offering will be used for general corporate purposes and to refinance existing leverage.

New Capital (Press Release)

While it is always a positive when an entity can access the capital markets, for CEFs it is a bit different. Given the subordination of the common equity, preferred shares placement is a given, with the cost actually making the difference. For the latest preferred stock placements the spread paid by the fund is fairly wide (around 300 bps for the 7-year placement), while the all-in cost is extremely high. Series L pays investors 7.12%, while Series M offers a 7.28% yield.

The new placements are fairly expensive when compared to older shares:

Cost of Capital (Annual Report)

The above table is from the most recent annual report, available on the fund’s website. We can see that the average cost of capital for the existing preferred shares is around 4.2%. The cost has now jumped almost 2x to 7.2%. That is a massive increase which is going to eat into the cash-flows available to pay the common shareholders. Unlike floating rate debt, which resets lower as Libor/SOFR decreases, the new debt issuances are fixed rate. That means that the higher costs have moved higher until the preferred shares maturity dates, which are in 2029 and 2032, respectively.

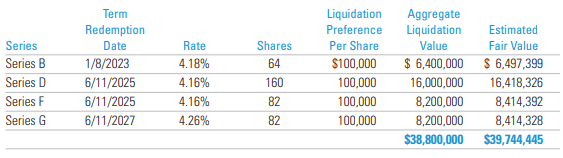

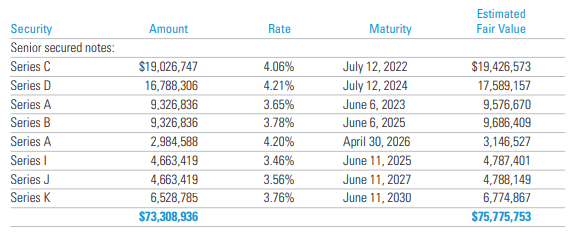

The fund also layers in leverage via the issuance of senior notes:

Senior Notes (Annual Report)

The same theme is playing out here as well. The cost to place this type of debt is around 4%, much lower than the cost of capital for the newly issued preferred shares. Term, fixed rate debt is a double edged sword – while attractive if risk free rates keep increasing, it can become extremely expensive when rates decrease.

We can see how the new preferred share issuance is going to refinance some of the upcoming maturities in both the senior secured notes and existing preferred equity. While preferred stocks generally do not have a defined maturity date and can be “rolled-over” by funds, the CEM shares are “Mandatory redeemable preferred stock”, giving them a term structure. Although the new preferred shares are attractive from a yield perspective, they are not currently listed on any exchanges:

Listing (Annual Report)

Performance

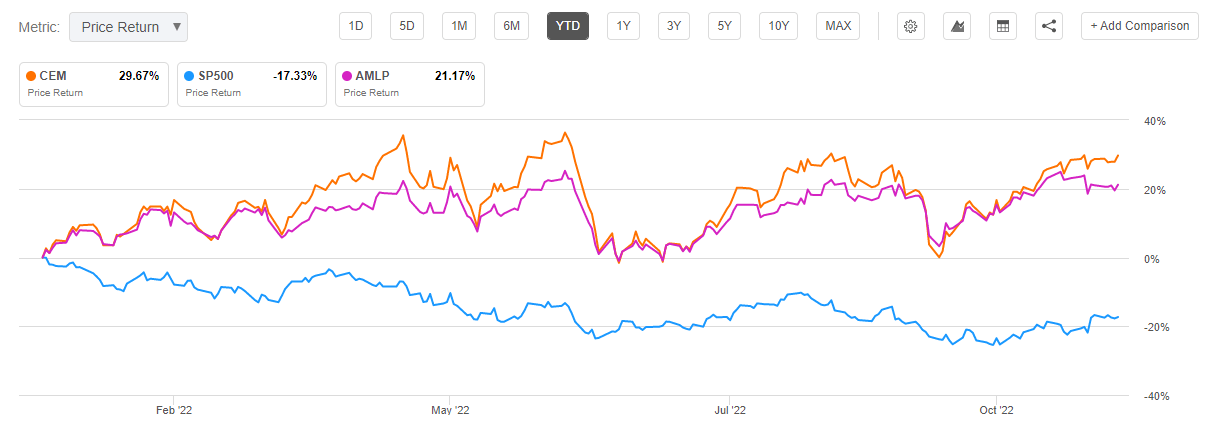

CEM is up substantially in 2022, beating the unleveraged MLP ETF AMLP:

Performance (Seeking Alpha)

The MLP asset class is become more and more a pure yield play. That means that the capital gains from the discounts seen during the Covid crisis are behind us. As a yield play CEM has now become a bit more unattractive given its rising cost of funds.

Conclusion

CEM is a closed end fund focused on MLP equity. The vehicle is up substantially in 2022, on the back of improved underlying corporates’ balance sheets and revenue streams. We rated CEM a Buy in the past, and the fund has outperformed, being up 27% since our rating versus a loss of -16% in the S&P 500. With the fund now placing new preferred shares at very expensive all-in yields, we are moving to Hold on the name. We would like to see the fund retrace some of its gains with the overall market before going long again. The newly issued preferred shares offer extremely attractive yields exceeding 7%, but unfortunately they are not currently listed on any exchanges.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment