Funtay

The global energy industry has been one of the most volatile sectors over the past three years. In 2020, widespread lockdowns led to massive declines in production. While demand for energy products has remained near record levels since then, global oil output is only finally starting to return to normal. OPEC oil production also continues to rise despite recent cuts and speculation of further reductions. At the same time, the US government is ending its oil market stimulus via the Strategic Petroleum Reserve release.

2023 is likely to be an interesting year for the energy market. In my view, we will soon see the test as to whether or not the oil market has “returned to normal” or will fall back into a shortage. With the price of oil down dramatically over the past nine months, large producers such as Devon Energy (NYSE:DVN) have seen their stock price decline. DVN is among the larger oil producers and trades at an attractive TTM “P/E” of ~6.5X. With crude oil and natural gas significantly lower than last year, Devon will likely face significant EPS declines this year.

Devon Faces A Volatile Macro Landscape

Larger energy companies like Devon are highly dependent on the economy and uncontrollable dynamics in the energy market. Devon’s managers can pursue growth or consolidation strategies but can not control the volatile price dynamics of oil and natural gas. As such, when considering “macroeconomy-dependent” companies like Devon, investors must consider the firm’s macroeconomic landscape closely.

If 2023 is the “year of recession,” as many economic analysts predict, producers like Devon will likely face volatility as energy prices decline further or rise if demand does not fall as expected. In my view, considering the oil market supply is still below pre-COVID levels, and oil has reduced materially, the market seems to be bracing for a considerable decline in energy demand. Like the global shipping market, I believe lackluster supply may offset the recessionary decline in energy demand, potentially leading to higher oil prices.

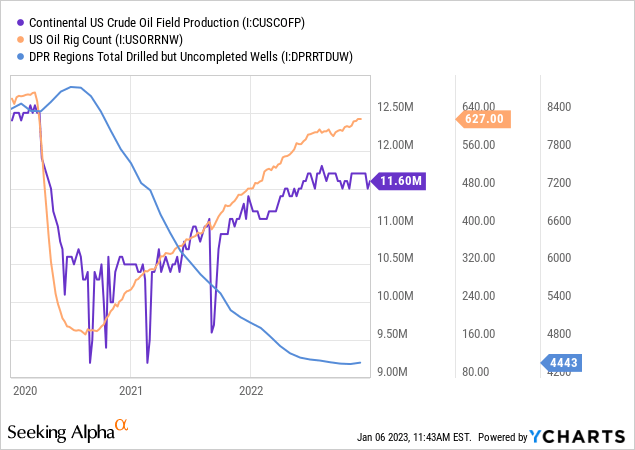

Firstly, US oil production is still considerably below pre-COVID levels despite a significant rise in the US oil rig count. The rig count continues to rise, but production is not increasing. In my view, this is likely due to the massive output declines seen in new oil wells (~70% during their first 24 months). Over the past two years, many energy producers have utilized previously “Drilled but Uncompleted” oil wells to increase output without investing heavily in new drilling. Those younger wells are experiencing steep production declines today, so more aggressive (and expensive) drilling is necessary to offset the drop. See below:

As stated by many oil market analysts, the dependence on “DUC” wells post-COVID creates a huge production growth barrier that may take some years to overcome. While international data is far more opaque, the same factors limit OPEC+ production growth. OPEC+ production has risen materially, but it remains below the group’s quota level – a historically rare occurrence that indicates strain on behalf of producers.

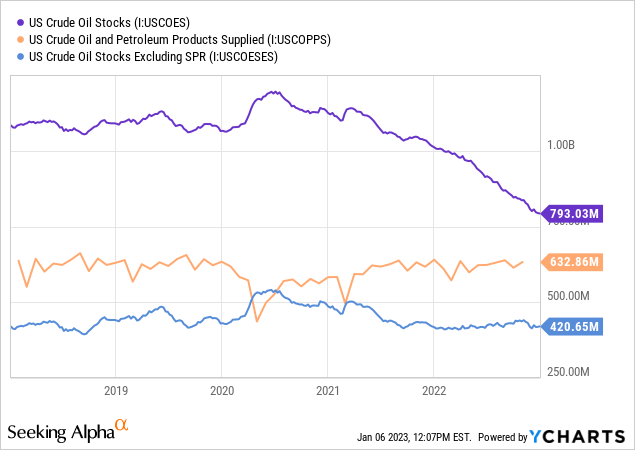

Due to weak global production and increased US exports to Europe, US crude oil inventories are at extreme lows. Last year, the immense release of government-owned oil caused commercial oil inventories (“oil stocks excluding SPR”) to remain flat. Still, with oil demand at record levels (“products supplied”) and SPR sources ending, I believe we will soon see a significant decline in commercial inventories. See below:

Overall, I believe this situation indicates a bullish potential for the crude oil market. Oil demand remains materially above output, and there are numerous barriers to production growth in the immediate term. Most US oil companies, including Devon, have shifted their focus away from growing output toward maintaining output and paying higher dividends or reducing leverage. Further, with oil down to ~$74, most US producers will see minimal profits from drilling new wells considering “new well” breakevens are now around $50-$70.

Natural gas is similar, although US production has grown considerably faster – with the caveat of much more gas going to Europe via LNG to offset lost Russian sources. Natural gas prices are also down significantly, partially due to the abnormal winter heat wave impacting many countries worldwide. At only ~$3.75, natural gas producers (like Devon) will likely make very little profit (or lose money) on new drilling. Last year, when natural gas was much higher, drilling activity rose tremendously. Today, the natural gas rig count is decreasing as producers are backing away. Thus, although Devon will face pain in the short run, I believe it sets the market up for even more significant output cuts that may cause a sharp reversal in prospects later this year.

Demand Remains Strong As Supply Falls

Energy prices are now down significantly from 2022 highs. One cause is the immense support from SPR releases into the private market that artificially boosted US (and foreign) commercial oil availability. The Biden administration is now reversing-course and planning to refill the SPR next month, taking supply out of the retail market. If the SPR release was akin to a “dovish” Fed policy, the White House is certainly shifting to “tightening” the oil market, likely leading to higher prices.

Of course, if the global economy enters a recession, then demand for oil and other energy products supplied by Devon should decline. I believe this potential is largely priced into the oil market, considering prices are down so much despite supply-side weakness. US and global manufacturing and banking data indeed signal a recession; however, employment data remains relatively strong, and unemployment is still falling. US oil consumption remains near record levels despite the economic slowdown, and with employment abnormally strong, I believe oil demand may remain high even if the economy enters a recession. At least, I do not think demand will fall as much as it has in past recessions, such as 2008.

What is DVN Worth Today?

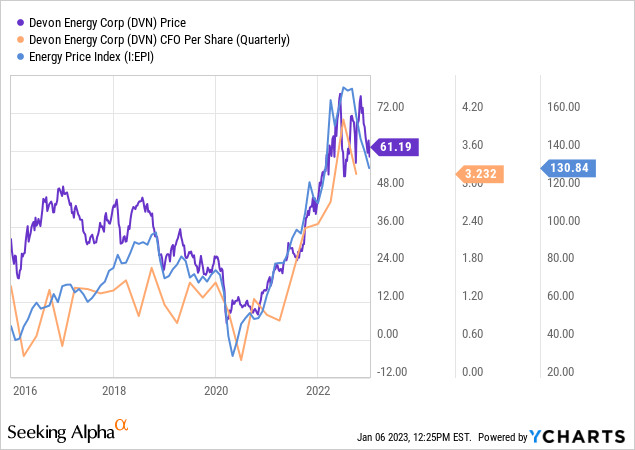

Devon had a stellar 2022 with the highest earnings and cash flows in years. The company used much of this cash flow to reduce its overall leverage level, making it more resilient in the face of another energy price collapse. The company’s cash flow and price are closely correlated to the Energy Price Index – an aggregate measure of various fossil fuel commodities. See below:

I believe the Energy Price Index is likely closer to the 110-120 level if measured today following the recent declines in natural gas and oil. The index also historically lags behind the energy futures market. Around the end of 2021 to early 2022, when prices were near today’s levels, Devon generated around $2.4 to $2.7 in cash flow per share. The company’s costs may be higher today (seen in sector-wide cost inflation), but its production has also increased over the past year, so I expect its Q4 2022 cash flows to be around the same. While Q1 2023 is still early, energy prices have been in a substantial trading range and are not trending as strongly, so this quarter may yield similar results.

Devon historically trades at a price-to-cash-flow around 6X, though with significant variance. While that is a lower valuation, it accounts for the elevated risk within the sector and its higher real deprecation. Estimating its quarterly cash flow per share at $2.60 ($10.40 annually), I believe its fair value is around $62 per share today, or 6X its estimated cash flow. Unsurprisingly, DVN is trading very close to that price today, indicating it is fairly valued given no expected oil price change.

The Bottom Line

By itself, DVN is not remarkable and offers no strong catalysts due to operational or managerial plans. Of course, that fact is one reason I like the company, as it provides a dependable way to speculate on energy prices. Smaller producers can deviate more from energy prices, while energy conglomerates like Chevron (CVX) have such broad businesses that they’re less correlated to the cost of oil.

Overall, I am bullish on DVN because I believe oil and natural gas prices will likely rise this year. DVN is trading at its estimated fair value, which should increase significantly if petroleum products see another wave higher. There are a few key catalysts that could boost oil prices. The most immediate of these is the switch from SPR withdrawals to refills, directly reducing oil availability in the commercial market. Tied into that is the low domestic and global oil production associated with low international drilling rates, higher depletion rates, and supply constraints from the Russian war. While that war will ideally end soon, I do not expect Russian trade to resume so quickly due to likely geopolitical pressures and infrastructure constraints (see pipeline explosion).

It is possible, if not very likely that oil and gas demand will decline in 2023 due to an economic slowdown. However, with aspects of the economy remaining resilient (such as employment) and the Chinese economy reopening, demand may not decline as much as the market currently expects. Further, it seems more likely that global supply will be strained more than demand, particularly considering energy firms will likely avoid investing with energy commodity prices falling near breakeven levels.

That said, a global recession is Devon’s most significant risk factor since it remains unclear how large, long, or widespread it will be. It is entirely possible that a more profound and prolonged recession negatively impacts oil demand sufficiently to cause prices to become more depressed. It is also possible (though seemingly unlikely) that OPEC+ acts to increase production faster. While I believe DVN offers significant upside associated with a bullish oil trend, that is certainly not guaranteed. Energy investments like DVN are more volatile than most, so investors should exercise caution – particularly in the unstable economic environment.

Be the first to comment