Ibrahim Akcengiz

Selloff Building Long-Term Upside for Growth

Market Overview

Growth equities entered a bear market in the second quarter as worsening inflation and aggressive actions from the Federal Reserve weighed on corporate results and investor sentiment. Persistent price pressures, global supply chain disruptions and rising recession risks drove the S&P 500 Index down 16.10% for the quarter, capping its worst start to the year (-19.96%) since 1970.

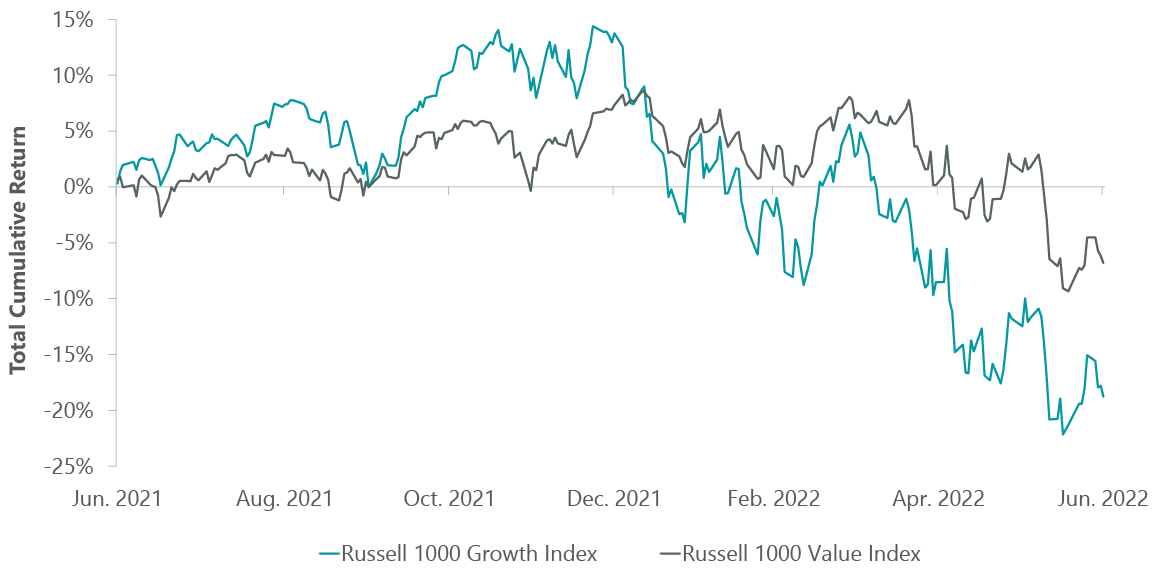

Rising interest rates continued to weigh most heavily on growth stocks, whose future earnings are discounted, with the benchmark Russell 3000 Growth Index falling 20.83% for the quarter and underperforming the Russell 3000 Value Index by 842 basis points. Growth trails value by 1,500 bps year-to-date. To put this in perspective, the underperformance of growth compared to value over the trailing three and six months is among the most severe in the Russell 3000 indices dating back to 1995.

A worse than expected 8.6% Consumer Price Index reading for May pressured the Federal Reserve to raise rates 75 bps in June, the largest hike since 1994, and project ambitious tightening through the rest of the year. The 10-year Treasury yield surged to a four-year high of 3.5% in mid-June, eventually finishing 67 bps higher for the quarter at 3.01%.

The U.S. economy contracted in the first quarter and the outlook for GDP growth has tempered as more liquidity leaves the financial system. While consumer demand has mostly held up, a shift in spending patterns from goods to services led to big first-quarter earnings misses and lowered outlooks for several retailers and social media platforms that are leading digital advertisers. Though not immune to the broader market pullback, the ClearBridge All Cap Growth Strategy outperformed the benchmark during the second quarter. As we discussed last quarter, steadily growing, highly free-cash-flow-generative and more moderately valued companies have supported results through the rout for growth stocks (Exhibit 1). These quality growth businesses with strong leadership positions and effective management teams have been able to execute through a challenging macro environment. We believe such companies should emerge even stronger on the other side of the downturn.

Exhibit 1: Growth/Value Gap Continues to Widen

As of June 30, 2022. Source: FactSet.

Portfolio Positioning

The continued selloff in the market in the second quarter offered entry points into a number of pipeline ideas that were significantly more expensive months ago but are now becoming more appropriately valued. We took advantage by adding three new names during the second quarter: Sherwin-Williams (SHW) in the materials sector and Stryker (SYK) in the health care sector are expected to provide greater stability to the portfolio while Airbnb (ABNB) in the consumer discretionary sector increases exposure to reopening and services spending.

The addition of Sherwin-Williams, a manufacturer of paints and coatings for professional, industrial and retail customers, adds resilience in the current inflationary environment. Paint is a relatively small part of total project input costs which can be passed through with price during inflation, and the company has a track record of successfully managing through periods of increased commodity costs. We are attracted to the company’s durability of growth by operating a strong franchise with both organic growth and consolidation amassing a strong portfolio of brands. We like Sherwin-Williams over competitors in the paint industry due to higher volumes, a domestically focused revenue base and strong relationships with the home builder and pro community. We believe the company will be able to keep pricing and expand margins as commodity pressures ease.

We added to our countercyclical health care exposure with the purchase of medical device maker Stryker. The company is a quality compounder in medical technology with higher growth from taking unit share in orthopedics. Stryker’s execution in its medical and surgical equipment businesses have also consistently generated premium growth and it is investing in new software for its robotic-arm assisted surgery, hip stem, and stroke care solutions. The company’s procedure-based business has been strong as it continues to take share in the growing end-markets of knee and hip surgeries, and hospital and ambulatory surgery center growth continues post-COVID.

Airbnb is the leading online platform for alternative accommodations globally. We believe the company is well-positioned to capitalize on the large and growing market for travel and experiences, with the potential for growth in e-travel to be higher post pandemic due to pent-up demand and increased work from anywhere flexibility. Airbnb is highly profitable today, though we see room for further margin expansion ahead. Furthermore, secular underpinnings to growth, a more variable cost structure and strong balance sheet should help the company drive better through-cycle performance as compared to its consumer discretionary peers.

The severity of the current selloff, exacerbated by extreme negative investor sentiment, especially toward growth stocks, has compressed the multiples of a number of portfolio companies despite strong fundamentals and led us to add to several existing positions. One example is cybersecurity software provider, CrowdStrike (CRWD), which continues to execute well against a robust demand environment for its endpoint security solutions with quarterly results and forward guidance outperforming expectations. We similarly added to disruptive growth companies HubSpot (HUBS) and Doximity (DOCS) during the quarter.

During times of volatility, we also make efforts to manage risk and protect investor capital. This can involve trimming back or selling stocks with near-term risks or lack of visibility. We exited a position in omnichannel cosmetics retailer Ulta Beauty (ULTA) as our thesis had largely played out in terms of a post-COVID 19 earnings recovery. Although department store closings were not as extreme as we originally thought, Ulta has steadily gained share over the last several years and its partnership with Target represents a new avenue to gain customer loyalty. That being said, we are wary about the resilience of the consumer and Ulta faces similar labor cost inflation as other retailers which could crimp margin expansion in coming quarters.

Outlook

The aggregate result of these transactions is a more concentrated portfolio with higher active share that best represents our highest conviction names. We constantly analyze our positions to determine which to hold and which to add to on weakness. Most of our recent additions have been in areas where we see the greatest earnings visibility and valuation support, while we have been staying put or cutting back on holdings in the most expensive areas of technology and the Internet. That said, we maintain a watch list of companies and some dry powder to respond to dynamic market conditions. Further clarity on the extent of Fed tightening and the slope of the yield curve will give us greater confidence to be buyers of select growth companies.

As fear continues to rise in the markets, owning industry leaders with balance sheet strength and flexibility is essential. Sturdy businesses with tailwinds have seen their share prices correct along with more speculative companies and a recession is becoming the consensus view. After the sharp correction, we feel we are getting closer to levels for stock prices and sentiment where risk/reward becomes asymmetric to the upside. We believe a pickup in merger & acquisition activity would be an early signal that undervalued assets are becoming monetized. The collapse of growth valuations has been painful but establishes a strong base for long-term investors like us who are able to look out five to ten years.

We have brought down financial leverage in the portfolio and are confident in the seasoned management teams running the companies we own. Going forward, we will continue to apply a high conviction, business owner’s approach while seeking to maintain balance and be opportunistic with portfolio additions. The Strategy has historically generated solid relative results during market corrections and, despite recent performance struggles, we are committed to the formula that has compounded growth for our investors: a focus on stock selection for the long term. We remain dedicated to conducting robust fundamental analysis that leads us to attractive growth opportunities and managing a portfolio with a diversified set of drivers over a 3-to-5-year time horizon. We believe that a duration of growth mindset is a key differentiator that should play out as normalization of the market and economy continue.

Portfolio Highlights

The ClearBridge All Cap Growth Strategy outperformed its Russell 3000 Growth Index benchmark in the second quarter. On an absolute basis, the Strategy had losses across eight of the nine sectors in which it was invested (out of 11 sectors total). The lone contributor was the consumer staples sector while the primary detractors were in the IT, consumer discretionary and communication services sectors.

Relative to the benchmark, overall sector allocation contributed to performance. In particular, an overweight to the health care sector, an underweight to the consumer discretionary sector and stock selection in health care drove results. Conversely, stock selection in the IT, industrials and consumer discretionary sectors and an underweight to consumer staples weighed on performance.

On an individual stock basis, positions in Vertex Pharmaceuticals (VRTX), Monster Beverage (MNST), Twitter (TWTR), UnitedHealth Group (UNH), and Ionis Pharmaceuticals (IONS) were the leading contributors to absolute returns during the period. The primary detractors were Amazon.com (AMZN), Nvidia (NVDA), Meta Platforms (META), Microsoft (MSFT) and Broadcom (AVGO).

In addition to the transactions mentioned above, we exited positions in Medtronic (MDT) in the health care sector and Pentair (PNR) in the industrials sector.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment