Justin Sullivan/Getty Images News

About forty years ago when the market was emerging from the largest bout of high inflation in history I decided to buy banks. The market was cheap and banks were cheaper. This raised a basic question: should I buy the best or should I buy the cheapest? With banks it’s a question which never goes away. On the one hand, banks are banks are banks. On the other hand there are major differences in emphasis. Some large banks put quite a bit of emphasis on consumer banking, for which NIM (Net Interest Margin) is the major factor. Some derive a large part of revenue and earnings from Wealth Management, an area sometimes classified as a Private Bank when clients are primarily the very affluent. Some make a lot their money in investment banking, for which the earnings can be great but are lumpy and unpredictable because of the ebbs and flows in the level of mergers and acquisitions.

Citi is set apart by the fact that it has a large international cross-border presence. One of its major operational goals is to be the leader in cross-border banking and global wealth management. These areas have the potential to be highly profitable, but they come with special risks. Citi ranks high among global banks (#6) but as a result is more vulnerable than the other three major American banks to events outside the United States. It is, for instance, the U.S. bank most impacted by the Russia-Ukraine war, with exposure to both countries as well as to the rest of Europe for which trade sanctions impact cross-border banking. Its major specific problem currently is its $7.9 billion investment in Russia which it is attempting to sell. Investors should be aware that an exit from that investment will be difficult and a large write-off is entirely possible.

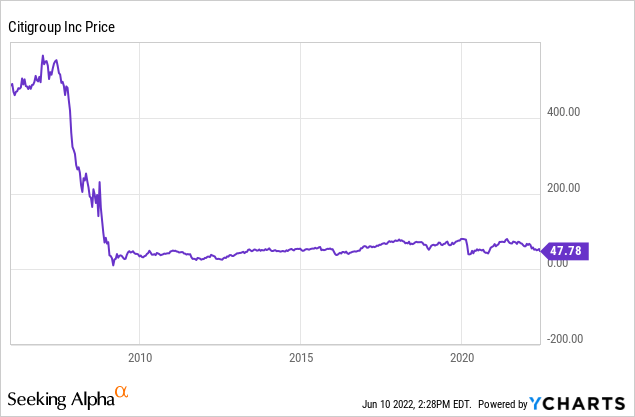

Over the years Citigroup has acquired a reputation as the worst major U.S. bank. In the housing/credit default swap financial crisis of 2007-2009 it was the biggest loser, and not coincidentally the biggest miscreant. Then-CEO Charles Prince ignored the report of a senior executive who ultimately became a whistleblower. Citi received a major government bailout which came with partial government ownership and supervision. Its stock fell to a price below $1 and it was still trading around $4 when on May 9, 2011, it executed a one for ten stock split. That raised its stock price to a respectable $40. For shareholders that reduced the number of shares owned by a factor of 10 so the reverse split didn’t help. However, it enabled Citi to resume paying dividends at a rate of $0.01 (yes, that’s one penny). The split was actually carried out after C stock had quadrupled off the bottom. If you think that the $40 price isn’t very different from the current price you are absolutely right. To be scrupulously fair, Citi stock traded at a price around $80 three times in recent years, in 2018, 2020, and 2021, before falling steadily in 2022 to its present price around $47. That’s not a lot of progress to make for more than a decade. Here’s how that looks on a chart:

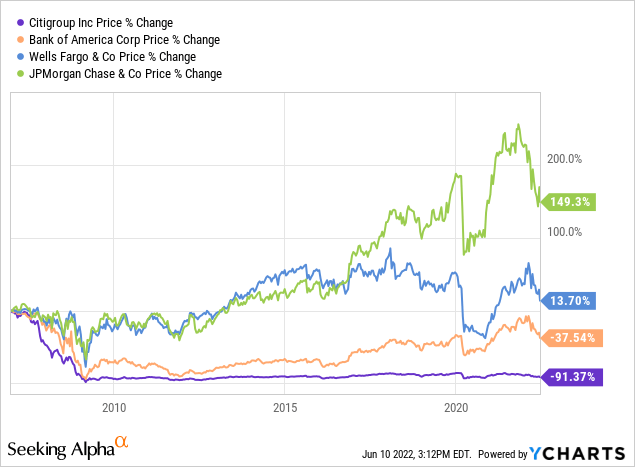

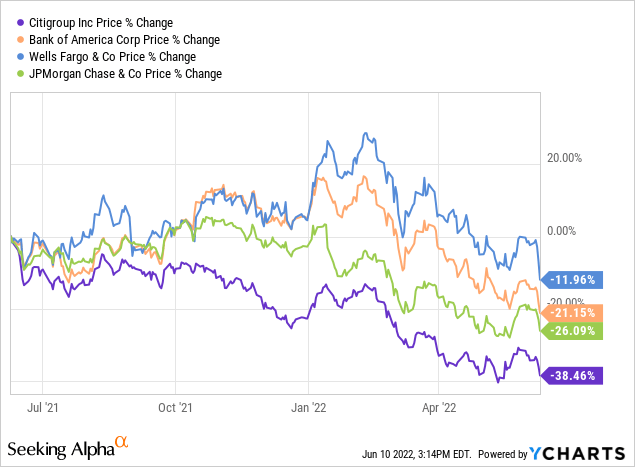

There’s always an “on-the-other-hand”. Citi is now ridiculously cheap in comparison to the market as a whole and other banks of similar size. Its P/E ratio of about 7.5 is around 30% lower than the P/E ratios of Bank of American (BAC) and Wells Fargo (WFC), both of which are about 10.5, and a bit lower than that by comparison with JPMorgan (JPM), which as the leader of the four major banks may be entitled to at least a small premium. A lower P/E implies that the market requires a cheaper price to entice buyers of the stock. Inversely, the dividend yield of C, above 4%, is the cash return the market requires compared to about 2.5% for BAC and WFC and 3.13% for JPM, which has a higher payout ratio. Here are two comparison charts for the four major banks, the first going back to 2007 and the second for the past year:

The longer term chart shows that JPMorgan earned its place as the best big bank, at least when looking through the rear view mirror. Bank of America and Citi suffered more or less equally in the initial collapse of 2008-2009, but Bank of America rallied much more strongly off the low as Brian Moynihan assumed the position of CEO. Citigroup basically flat-lined and provided no capital gains to speak of for the entire recovery period. For the last year Wells Fargo has been the star while Citi continues to come in last.

Is it now so cheap that it’s the best buy among the majors? Warren Buffett may think so. The May 16 13F filing for the first quarter of 2022 showed that Berkshire Hathaway (BRK.A)(BRK.B) had initiated a position buying 56.16 million shares for $2.95 billion. That made Citigroup the fifteenth largest holding in Berkshire’s portfolio. It is fairly clear that it was Buffett himself who bought it. It has the value characteristics which appeal to Buffett plus the 4% dividend yield which in Buffett’s case replaces the very low current yield on short term Treasury Bills.

Should Citi’s Checkered Past Be A Present Concern?

Citigroup has a lot to live down. If you look at Citi’s history on Wikipedia you notice a number of events which I remember well. Citi is one of the oldest American companies and it had a pretty good first century and a half, but the past fifty years or so have been filled with missteps. Citi has a multi-decade record of getting into and out of mergers and acquisitions without much to show for their effort. Much of the shuffling in and out of mergers took place under the leadership of Sandy Weill as CEO then Chairman from 1998 to 2006.

Weill’s successors as CEO, especially Chuck Prince, did little to improve the erratic performance of a company famed for self-aggrandizing behavior at the top. Prince achieved fame mainly for the following quote which he made in 2007 as the mortgage/collateralized debt swap bubble reached its peak: “When the music stops, in terms of liquidity, things will be complicated,” Prince said. “But as long as the music is playing, you’ve got to get up and dance.” Within a few months Prince had been sacked, the Federal Reserve had assumed control, and Citi’s investors had been basically wiped out. The successors of Weill and Prince at Citigroup were left with a bank which looked like the metaphoric equivalent of major German and Japanese cities after World War II – rock piles and rubble. Michael Corbat, CEO from 2012 to 2021, is credited as making an improvement simply because things stabilized during his regime.

Current CEO Jane Fraser may turn out to be a good choice for building a better future, but it’s far too early to announce a verdict. Fraser came up through Citi’s investment and global banking division, becoming Global Head of Strategy and Mergers and Acquisitions in 2007 and CEO of Citi Private Bank in 2009 where she had great success. Her later positions gave her experience with the various other units at Citi, including service as CEO of Citigroup Latin America, where her tasks included “instilling a more U.S. like culture.” What she apparently learned from the experience was that U.S. consumer banking culture cannot work in other countries except for Singapore, Hong Kong, the UAE, and London. One of her first initiatives as CEO was to sell the consumer banking units in 13 other countries including China, India, and Russia.

“Creating a Winning Culture” is listed prominently as one of Citi’s three major goals in the slides for the recent 1Q earnings call. This is an extraordinary goal for a large company with 210 years of history. Where were previous CEOs and many present board members? Mike Mayo, probably the best bank analyst on Wall Street and certainly the one who asks the most pointed questions on earnings calls, noted as much in a question asked at the 4Q 21 annual earnings call on January 14:

MikeMayo

I have one more question. What’s the hardest part of the cultural change?

JaneFraser

Probably it’s been breaking down some of the silos. And that — the point on the principles we laid out, Mike, have connected is really a key piece of it. We’ve — we rolled out some new leadership principles last year, and it’s very much around how do we get the firm very well connected and really realize the full synergies … So breaking some of those old habits, I would say, the new structure is certainly helping as are the different initiatives we’re taking.

MikeMayo

And how long do you think that will take? Because you’re breaking down a culture that’s been ingrained for quite some time.”

Earlier in the earnings call Mayo asked a key question which I will let stand by itself without the effort at an answer:

But the biggest question that I and, I think, many investors have, is when all is said and done, who is Citigroup? What’s the most simple statement you can give on who and what Citigroup represents?”

What Did The March 2 Investor Day And The Most Recent Earnings Report Tell Us?

The eagerly awaited Investor Day on March 2 was a major disappointment to Citi investors. CEO Fraser herself said “It’s not a surprise that we’ve been outperformed and failed to meet the expectations of our investors.” You can look at that sort of admission two ways. One is that the CEO recognizes the need for immediate and drastic change. The other is that the data that comes with it is going to be a downer and reinforce a long history of failure.

The analyst response suggests that Investor Day went over with a loud thud. Mike Mayo, always to the point, commented two days later that he doesn’t think “he’s ever heard Citigroup use the words “failed” and “underperformed” more than at the Investor Day. SA News noted the following morning that Citi stock was “falling about 2.5% in Thursday morning trading. KBW downgraded the stock to Market Perform due to elevated expenses and a “prolonged outlook for subpar returns.”

What troubled analysts most was the low targets set compared to those at other major banks and the expected time required to reach them. Here’s a table of medium and long-term ROTCE targets assembled by Bram Berkowitz in his article on Investor Day.

| Bank | ROTCE Target | Time Horizon |

|---|---|---|

| Citigroup | 11%-12% | Medium-term |

| Wells Fargo (WFC -6.07%) | 15% | Long-term |

| Bank of America (BAC -3.88%) | 15% | Medium-term |

| JPMorgan Chase (JPM -4.60%) | 17% | Medium-term |

| Goldman Sachs (GS -5.65%) | 15%-17% | Medium-term |

| Morgan Stanley (MS -4.63%) | 20% | Long-term |

Source: Financial Statements, Earnings Call

The table is worrisome on two counts, (1) that Citi sees itself closing ground on its peers too slowly and (2) that compensation and bonus award to top executives is so vaguely based. CEO Fraser’s response to (1) on Investor Day was to say, “We’ve taken a number of bold moves already to focus Citi on core strength. This is an organic growth strategy … it will take time.”

The latter (2) is an issue that Mayo (once again) has complained of going all the way back to his testimony to the Congressional Financial Committee in the aftermath of the 2009 disaster and even to Congressional Hearings on Sarbanes Oxley in 2002. His premise: with goals for senior executives undisclosed, C has a long history of putting shareholders last while the very different situation for management is “heads you win, tails you also win.” Lest you think that I overemphasize Mayo’s view I will note that there is actually a Harvard Business School case based on his 2011 testimony to Congress.

Despite an earnings and revenue beat, Citi’s April earnings report does little to improve the Investor Day presentation. The bad news starts with the Russia/Ukraine problems above which were hard to escape for a bank with an international focus. The $7.9 billion in exposure to Russia cannot be mitigated by saying that Citi is looking to sell out. Who will the buyer be? A few companies have their problems with Russia, but as Citi isn’t an oil company you have to look at its probable Russia write-off as an unforced error. Bear in mind that the Russia exposure amounts to about 8% of market cap.

The major issue, not of a one-time nature, is the persistent increase in expenses which continue to pull ground on revenues at a disturbing rate. The below numbers (in millions) are extracted from the Financial Summary included in the April 14 Quarterly Press Release:

| 1Q21 | 2Q21 | 3Q21 | 4Q21 | 1Q22 | From 4Q | YOY | |

| Total Revs | 17753 | 19867 | 17447 | 17017 | 19186 | 13% | (2%) |

| Total Exp | 11471 | 11413 | 11777 | 13532 | 13165 | (3%) | 15% |

On the Earnings Call Transcript, Citi responders put a positive spin on the downtick of 3% in expenses from Q421 but the YOY number showing that expenses had gained 1500 basis points were disappointing. Mike Mayo chipped in alongside analysts who were upset with the rising costs, but he stuck to his surprisingly optimistic view that the new CEO was “facilitating business repositioning, capital reallocation, and cultural reinvigoration.”

On May 16, speaking to CNBC on the date of Berkshire Hathaway’s 13F filing which included the $3 billion investment in Citi, Mayo said that Buffett’s move was a powerful endorsement of CEO Fraser and warranted an upgrade of Citi to buy with a target price of $70, an increase of about 40% from its price at that time and close to 50% from its present price. He stressed that the next two or three years were going to be difficult, but if you are a long term investor like Buffett it was a good moment to buy. He also strongly recommended banks in general with Bank of America still his favorite, but he expressed doubts about JPMorgan and speculated that Buffett’s sale of JPM might have been due to its own $10 billion bump up in expenses. The great virtue to Citigroup, Mayo added, was its extraordinarily cheap price.

Buybacks And A Date To Keep An Eye On: June 26

The relatively modest amount of buybacks has been a bit of a sore point for investors and analysts. What’s up with a bank selling around 60% of Tangible Book Value (as of March 31) which isn’t buying up its own shares as fast as it can drop buy orders? At that ratio of price to book share repurchases are highly accretive to shareholder value.

The answer is more complicated than it seems at first glance. For the fourth quarter of 2021 Citigroup voluntarily continued the suspension of buybacks after the Fed had said OK, “pausing” until quarter one 2022. Here is what CFO Mark Mason said about the pause in the Q3 Earnings Call.

We’ve been looking at the pricing and economics around those impacted by SACR. And we’ve been looking at our capital actions to buybacks, and we’re going to pause buybacks in the quarter just for this quarter and resume those in the first quarter, probably at the levels close to what we saw in the third quarter and so lots of work around that.”

So that’s some odd syntax to obscure the reason for Citi’s buyback pause. Other banks were apparently not impacted by SACR, which is the acronym for Standardized Approach to Credit Risk, the Basel guidance for bank capital which can vary quite a bit among banks. It carries great importance to U.S. bank regulators. Stress tests are conducted by the Federal Reserve annually for systemically important banks to assure that they have adequate capital for a “severely adverse scenario.” Citi passed the 2021 stress test, but was near the bottom of the banks tested.

Citi’s CET1 (Common Equity Tier 1 Capital) dropped to 11.38% in Q1 2022, presumably fine even with the new minimum of 10.5%. It has a 2022 target of getting the number back up to 12%. A number of factors, some of which are beyond their control, can have an impact on this. One is the decline in prices of their fixed income portfolio of $16.6 billion. This is of course a paper loss as their fixed portfolio will largely be held to maturity at which time it recaptures its full value (unless it engages in swaps in order to take advantage of tax losses). Their Russian exposure of $7.9 billion is another factor and some analysts have raised the question as to whether the 13 foreign consumer banking units being disposed of have been sold at a profit or a loss, a subject on which top management was evasive at a recent earnings call.

It’s a fairly good bet that all of the above played a part in the decision to continue the pause on buybacks in 4Q21. In the first quarter they did $4 billion of share repurchases, so presumably whatever problems they had during 4Q21 they managed to figure it out. We won’t have to wait for long. The Fed releases the results of stress tests on June 26 and we will see if Citi passed and where they ranked among companies tested. If you want to buy Citi you might wait to see what happens.

Ratings Summary, Factor Grade, Quant Rankings

Sector Financials

Industry Diversified Banks

Ranked in Sector 204 out of 646

Ranked in Industry 21 out of 55

The above rankings aren’t bad for a company with a weak short and long-term record for earnings and cash flow growth, share price, and friendliness to shareholders along with low visibility on future growth. Despite its score of F for Growth its A- for Valuation and A+ for Profitability pull it back into the Hold area for the SA Model. I guess summing it up, you just keep in mind that what you are buying is Deep Value. The consensus for both SA Authors and Wall Street analysts is a Buy, although SA authors are split between Stronger Buys and Sells.

Is C Stock A Buy, Sell, Or Hold?

There’s no question that Citi is dirt cheap. That’s the starting point for considering Warren Buffett’s Q1 buy of $2.95 billion of its common shares. That’s not the whole story, however. Pretty much everything was wrong with the strategy and operations of Citigroup until a little over a year ago. Shareholders were taken for granted while top leadership acquired and flipped companies as large as Travelers (TRV) with little thought and no success. CEO Jane Fraser who took over a little more than a year ago has moved to develop a long term identity and plan for Citi, and Buffett seems to be persuaded.

If nothing else, Citi is by far the cheapest major bank, and in an environment which may be much more favorable for large banks than the market realizes, may position Citi for a huge bounce off whatever lows it reaches in the present down market. Because of its low P/E ratio it might be argued that Citi is likely to fall less than other banks if the market continues to tank and then bounce higher faster as the market recovers. Its dividend may also provide some protection, and if all is well with its stress test results (to be announced June 26) it should be able to carry out large share buybacks at a price making them very accretive to continuing shareholders.

The problems at Citi are not small, but they are at least obvious and generally recognized. Expenses continue to pull ahead of revenues, and until they are brought under control, there won’t be much incoming cash to spare for other capital allocation. It will be a struggle to get out of Citi’s $7.9 billion exposure to Russia. Citi also needs a clear strategy with which its 11-12% ROTCE can close the gap to the ROTCE level of other major banks which starts at 15%. Getting executive pay to correspond to actual achievement is another task for Fraser. It’s hard to break bad news to people you work with every day and depend on.

Barring an event like a stress test failure or other catastrophe, Citi is likely to be a decent holding for dividend oriented investors even without immediate growth. The long-term success of CEO Fraser will determine if healthy growth will arrive within a few years and make Citi a great holding if bought at the current price. For the intermediate term I’ll accept analyst Mike Mayo’s target of $70, assuming that all banks do well and Citi has reasonable operational results.

As for the simple Buy/Sell/Hold decision I don’t own it, so Hold makes little sense to me. It’s a wishy-washy term that amounts to saying no comment/no decision. If I owned it, however, I wouldn’t sell unless an opportunity to take a helpful tax loss presented itself. If so, you could likely think hard for a month and a day and buy it again if it is something you want to own. There are risks here, but they are well defined. I’m going to rank it a Buy, if it fits the needs of your portfolio, with the disclaimer that I am not likely to pile into it myself at the present time.

Be the first to comment