Joe Hendrickson

Situation Overview

Cinemark (NYSE:CNK)’s entire cap structure has been under pressure in 2022. The equity is down 36% over one year and the unsecured bond dropped from $105 to well below $90. There are a few ways to rationalize why CNK’s capital structure has underperformed. The sentiment has turned vastly negative toward theater operators after Cineworld filed for bankruptcy. Also, as part of the consumer discretionary index, entertainment companies became difficult to own with the looming recession due to the central bank tightening financial condition.

Seeking Alpha

TRACE

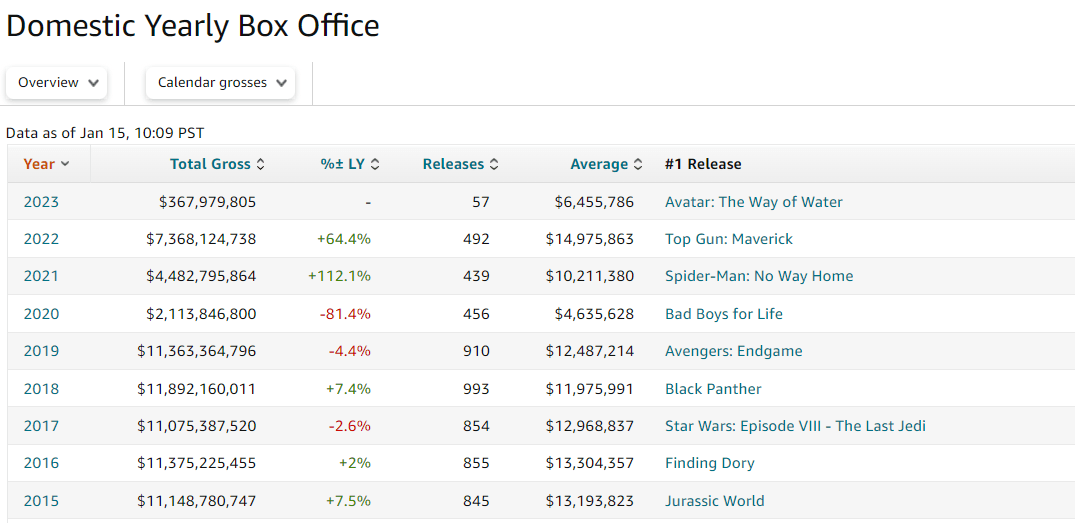

Underneath the negative headline and the broad market volatility, the fundamental of theater space is improving. While the domestic box office has yet to recover to the pre-COVID level, there is momentum behind this recovery trend. The industry research group expects the domestic box office to grow by 12% and the global box office to grow by 21% in 2023. However, this projection is still ~25% below the last three pre-pandemic years.

Box Office Mojo

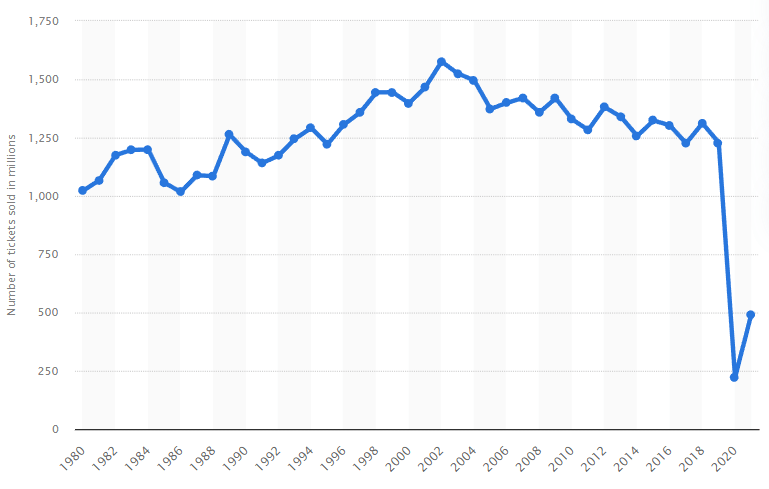

Moreover, the number of movie tickets sold in the US and Canada peaked in the early 2000s because consumers have access to a variety of video entertainment options. While the industry is able to increase ticket prices and consolidate to generate revenue growth, these two revenue growth levers won’t play a big role going forward. First, there are simply no more meaningful consolidation targets domestically. Also, for CNK specifically, the average ticket price of the last three quarters shows a worrying sign of deflation ($9.27, $9.11, and $8.73). This could mean that movie theaters don’t have much pricing power and CNK might have to reduce its ticket price back to the high-$7 and low-$8 pre-COVID range.

Overall, the theater industry has yet to recover from the damage done by COVID: revenue is lower, free cash flow is lower, and leverage is higher. While CNK is still a viable business, the quality of the business has certainly degraded. And because of the higher leverage, equity investors are forced to become credit investors and hope the business rebound meaningfully to be able to grow into the current cap structure.

Statista

Financial Modeling

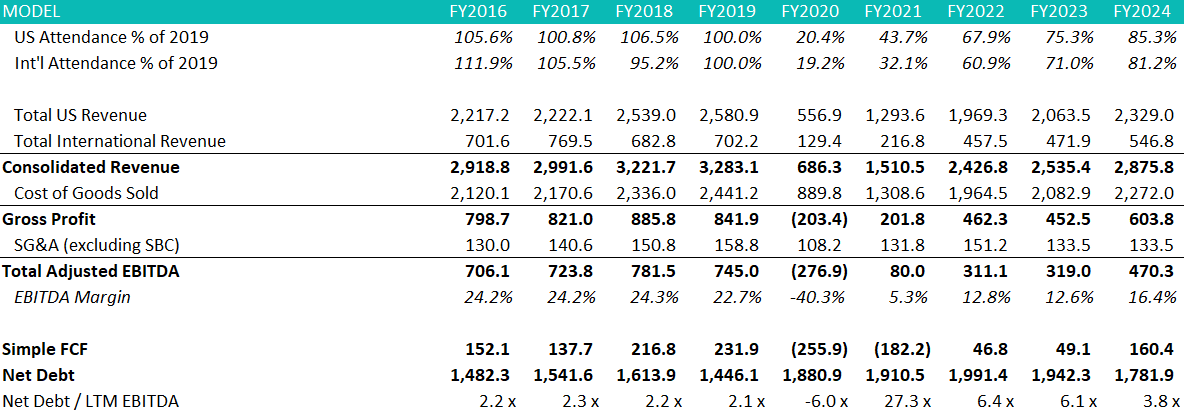

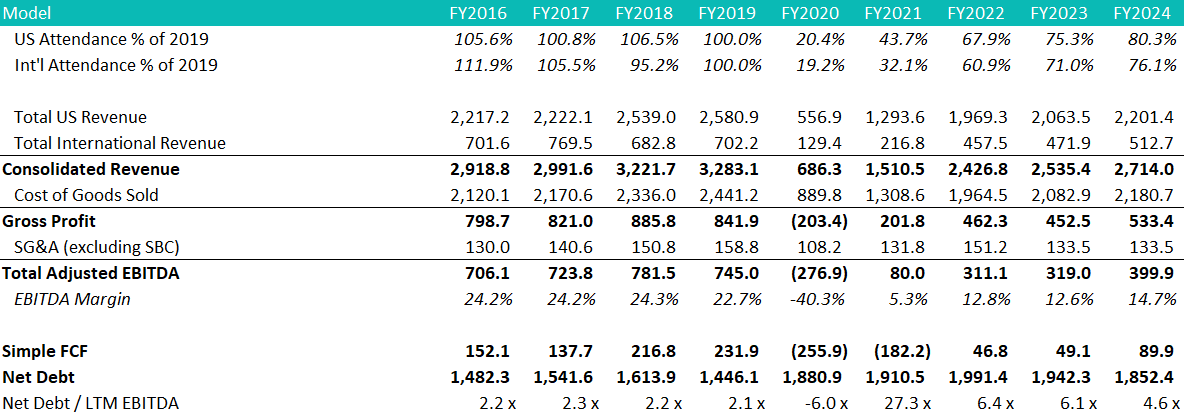

CNK probably exited 2022 at ~70% of 2019 attendance and plug in the industry research firm projection (more specifically, I assumed 2023 box office will be 25% below pre-COVID level) and assume a moderate margin expansion, CNK can generate a base-case EBITDA of ~$320 million by my estimation. It looks like the anticipated leverage inflection point will have to wait until 2024 when a combination of further EBITDA growth and cash build will reduce the leverage to 3.8x, from 6.1x in 2023.

Author’s Estimate

However, if the domestic box office only recovers to 80% of 2019 in 2024, then the deleveraging is pushed out for another year as expected, only falling to 4.6x. In any case, 2023 is most likely another “lost year” for CNK and the bulls will have to believe (1) the depressed domestic box office is not structural and (2) the box office will recover meaningfully sometime in 2024 or 2025 to provide CNK with an easy refinancing window.

Author’s Estimate

Capital Structure

CNK remains a highly levered company. I have CNK leverage close to 6.0x on my (perhaps pessimistic) FY2023 EBITDA of ~$320 million. Keep in mind that this is not assuming any recessionary disruption to the box office recovery. Luckily CNK doesn’t have any major maturity until 2025, when the term loan, 8.75% senior secured notes, and the convertible notes become due.

CNK should be able to refinance and/or extend the term loan since the term loan is levered sub-2.0x through. The 8.75% senior secured notes can be taken care of using cash on hand. I’m a little worried about the converts for the equity because one of the remedies could be an amend-and-extend with a lower conversion price, which is going to put pressure on the equity due to delta hedging by the convert arb players. Of course, CNK could tap the secured market to retire the convert outright, but it will become subject to the market condition at that time.

10-Q

Game Plan

Since the market historically ascribed an 8.0x EV/EBITDA valuation to CNK, CNK’s EBITDA clearly needs to recover meaningfully to backfill the current 10.0x valuation. Owning CNK equity is a bet on the degree of the recovery of the box office. Using the 2019 attendance as a goal post, the number needs to be in the 85% to 90% range of 2019 level to make the math work. As shown in the above cap table, CNK equity is trading ~10.0x of my FY2023 EBITDA estimate. My crystal ball is foggy as usual but I think there are a couple of reasons to believe the box office could recover. First, I don’t think the viewing behavior has changed too much. Second, after experimenting with direct-to-streaming movies, major studios are realizing the importance of the theatrical window once again. On the flip side, the looming recession risk is a wildcard. I’m also personally tired of watching the Avenger type of movies (simple plot married with great visual effects), but I’m only a data point of one. On balance though, I don’t feel like there is enough margin of safety in CNK equity right now and given the recent equity rally, I will be on the sideline as far as CNK equity is concerned.

The two series of unsecured bonds (5.875%/2026 and 5.25%/2028) look interesting to me, especially the 5.875%/2026. The net leverage through the unsecured part of the cap structure is ~4.4x (much more reasonable) and there is $460 million of convert and $1.3 billion of equity market cap below you (~$1.8 billion of junior capital before the unsecured bond is impaired). CNK has +$600 million cash on hand and FCF positive so I don’t expect CNK to run into any liquidity problems. Given all these positive credit attributes, I believe the ~10% yield is more than enough for the risk. I believe CNK bulls are better off holding the unsecured bonds – you have some downside protection, a higher degree of safety of capital, and an equity-like return for the next 3 years.

Risk

The risk to my bearish view on CNK equity is a soft landing scenario, but I believe even if a soft landing scenario played out, CNK equity still doesn’t work unless the box office recovers, which is also related to non-macro factors (e.g. moviegoers viewing habit).

The risk to my bullish view on CNK senior unsecured bonds would be a more severe downturn of the macro economy and the associated box office pressure. At 89 cents on the dollar, the 5.875%/2026 bond is creating CNK at ~4.0x EV/EBITDA (vs. FY2023 EBITDA estimate of $320 million), a large margin of safety against the 8.0x historical valuation multiple.

Conclusion

Falling from $40 to $10 doesn’t make CNK cheap. The industry is still in flux and the balance sheet is much more levered than before. CNK’s EBITDA needs to recover in order to backfill its current valuation and cap structure, which could be disrupted by a recession sometime in 2023 or 2024. The equity is a pass for me, but the senior unsecured bonds look interesting as an alternative for the CNK bulls – it’s essentially the same bet but the risk and reward is much better in my opinion.

Be the first to comment