Kameleon007

Investment Thesis

Lindsay Corporation (NYSE:LNN) should benefit from the increased net farm income due to the higher Agricultural commodity prices. Even though Ag commodity prices have declined since their May 2022 highs, they remain significantly above their pre-Covid levels. The company should also benefit from the ongoing drought conditions in core-midwest markets of North America, as farmers want an efficient irrigation system. In the international market, the company should benefit from the increased project activity due to the growing food security challenges in Central Asia and the Middle East. The company’s infrastructure segment should benefit from the Infrastructure Investment and Jobs Act (IIJA) funding of $1.3 trillion.

The margins should benefit from moderation in inflationary cost pressures and higher price realization. The company is also looking for opportunities to improve its productivity and grow margins. The stock is currently trading at a discount to its five-year average forward P/E. While some investors are worried about moderation in topline growth after a very strong last couple of years, I believe these risks are already priced in at the current valuations. Hence, I have a buy rating on the stock.

Revenue Outlook

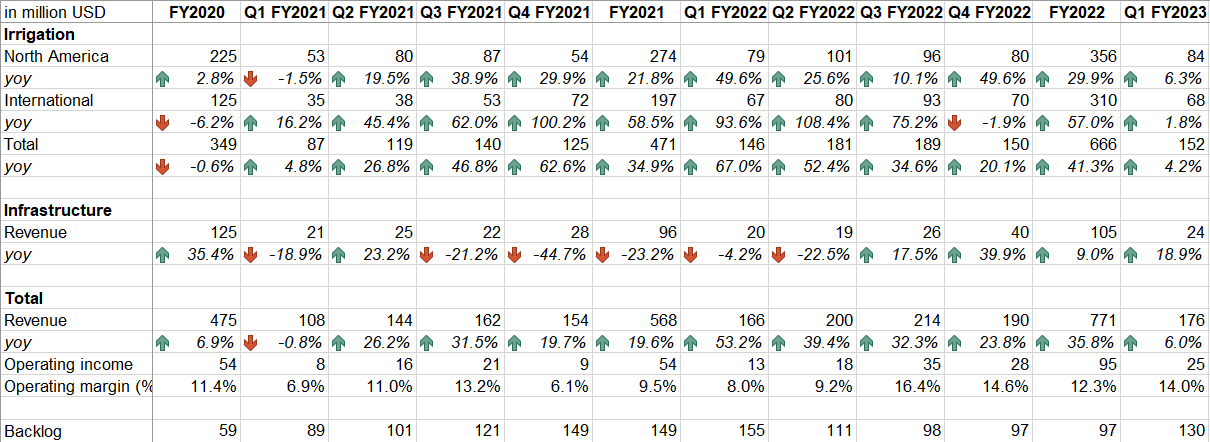

LNN experienced strong double-digit growth in FY2021 and FY2022 due to higher net farm income thanks to increased agricultural commodity prices. However, Ag commodity prices have declined from their May 2022 highs, and, as a result, LNN is witnessing some moderation in growth. In Q1 FY23, the revenue in the irrigation segment increased 4% Y/Y with 6% Y/Y and 2% Y/Y growth in the North America and international irrigation markets, respectively. The segment’s revenue growth benefited from 7% to 8% pricing growth and flattish volume, partially offset by unfavorable currency translation. The revenue growth in the North America irrigation market was driven by higher price realization and flat unit sales volume. In the international market, the higher sales in Brazil and other markets more than offset the impact of lower sales in Ukraine and Russia, as well as a one-time benefit from a $9 mn project sales in Egypt in the prior year’s first quarter.

The revenue in the infrastructure segment grew 19% Y/Y due to higher sales of Road Zipper systems, partially offset by lower Road Zipper lease revenue and lower sales of road safety products.

The company’s backlog in the quarter declined 16% Y/Y to $129.6 mn due to the improvement in supply chain constraints.

LNN’s historical sales (Company data, GS Analytics Research)

Looking forward, in the North America irrigation market, the price realization continues to remain strong, which should benefit the revenue growth in FY23. Additionally, the supply chain constraints that impacted the company’s business over the last few quarters have started to moderate. This should help convert the backlog into revenue at a good pace in FY23.

The prices of agricultural commodities such as soybeans (S_1:COM), wheat (W_1:COM), corn (C_1:COM), etc. are below their 2022 highs, but they are still trading at higher levels compared to pre-Covid levels. So, the farm economics are still healthy.

The drought condition in the North American market is leading to increased demand for efficient irrigation systems, and LNN is positioned well to take advantage of this opportunity. While the drought conditions in the far west have eased, the conditions in the core-midwest markets, including Nebraska and Kansas, have worsened. This should benefit the company’s revenue in FY23.

The international market is seeing the same market fundamentals, such as increased agricultural commodity prices and higher net farm income. The project activity in Central Asia and the Middle East continues to remain strong as food security remains a challenge in these regions. The World Bank as well as the countries themselves are taking initiatives to increase farming activities. This should benefit LNN given its exposure in the international market.

In the infrastructure segment, as the construction work ramps up after the winter season (in the back half of FY23), the demand for road zipper lease business should start improving. The segment should also benefit from the Infrastructure Investment and Jobs Act (IIJA) related funding.

Overall, I believe the company’s revenue should benefit from healthy farm-level economics, drought conditions in North America, easing supply chain constraints, and IIJA funding. However, tough comps from FY22, when farming activities saw an increase following the reduction of wheat and other crop supplies from Ukraine, should result in much more modest growth compared to the last couple of years.

Margin Outlook

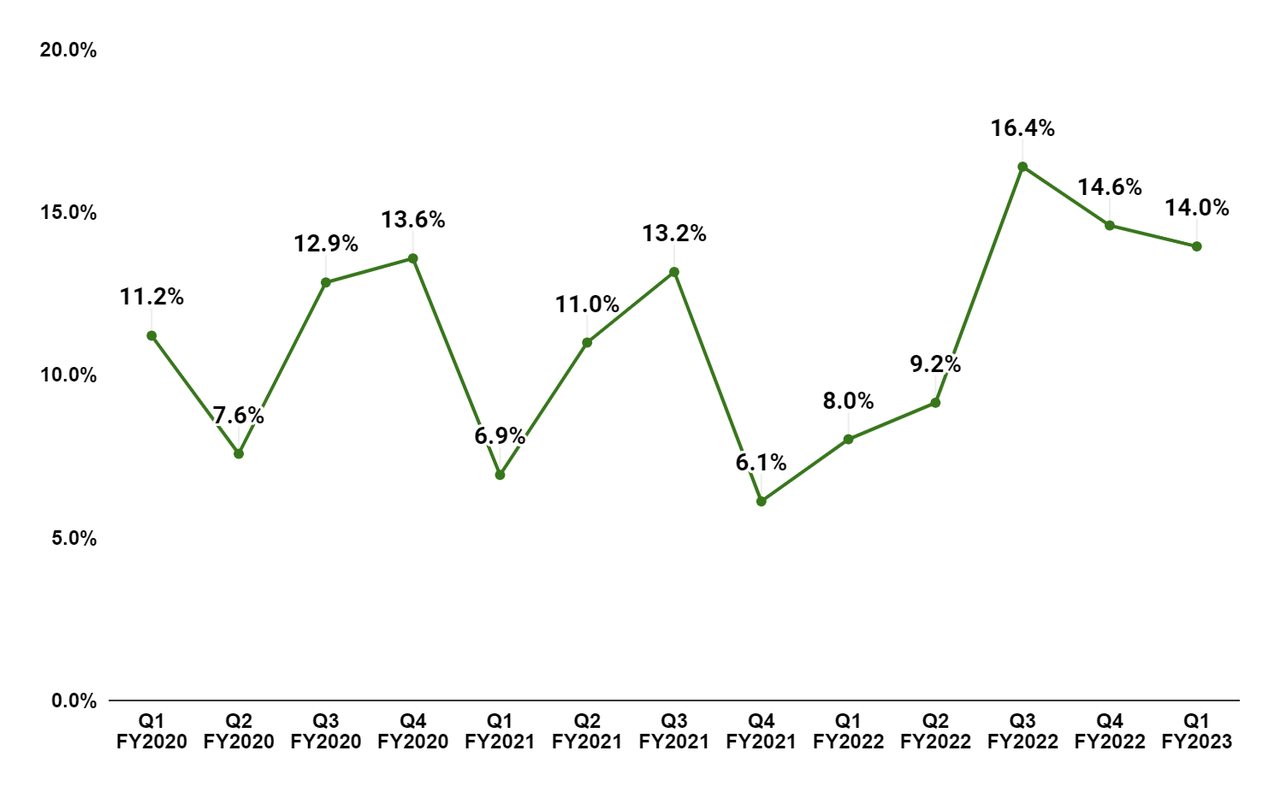

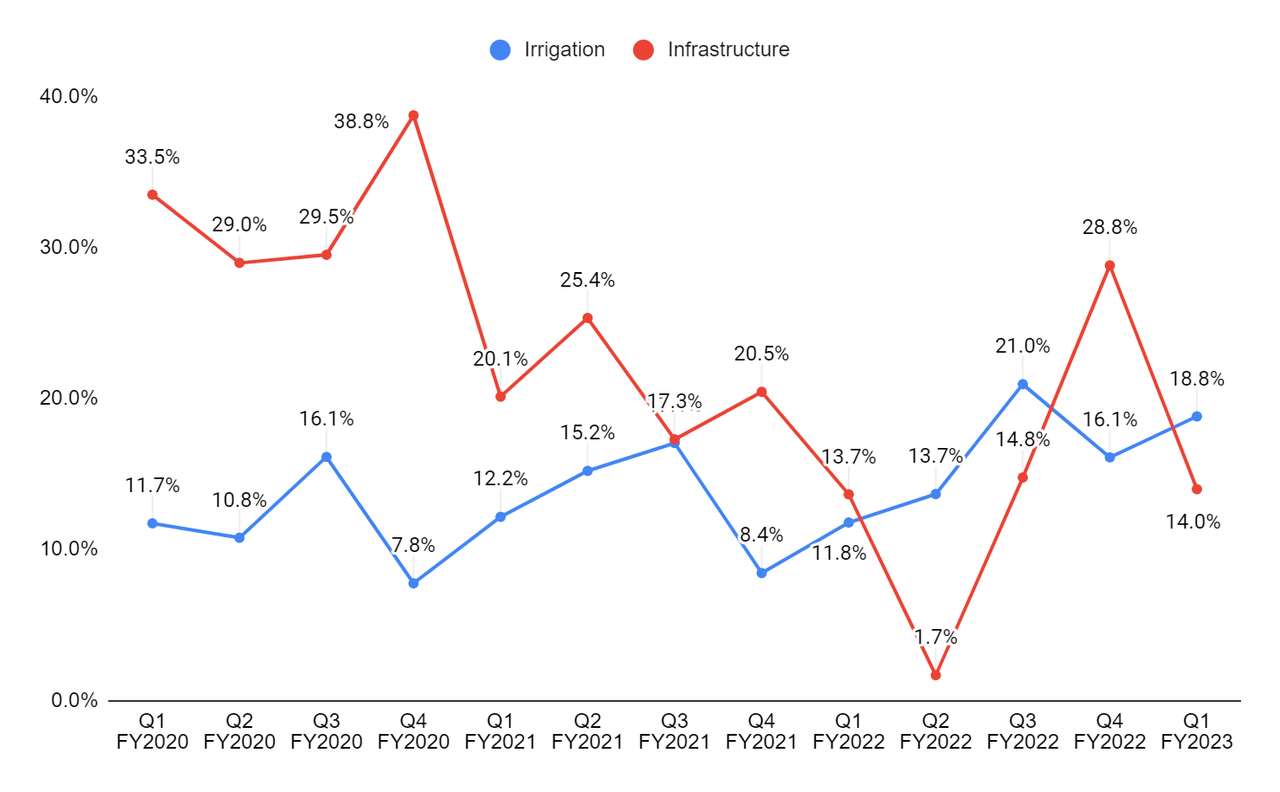

The operating margin in Q1 FY23 increased by 600 bps Y/Y to 14% due to higher price realization and moderate inflationary cost pressures. The operating margin in the irrigation segment increased 700 bps Y/Y to 18.8% due to improved price realization, a decrease in input cost inflation, and a favorable margin mix from higher sales in the international market. Additionally, the company benefited from easing comps, as in Q1 last year, the company’s operating profit was negatively impacted by ~$5 mn headwind resulting from the impact of the LIFO method of accounting for inventory. Under the LIFO method, the latest raw material prices are recognized in COGS rather than ending inventory, and this becomes a headwind during periods with rising raw material prices.

In the infrastructure segment, the operating margin improved by 30 bps Y/Y to 14% due to higher revenue and lower input cost inflation, partially offset by a less favorable margin mix due to lower road zipper lease revenue.

LNN’s operating margin (Company data, GS Analytics Research) LNN’s segment wise operating margin (Company data, GS Analytics Research)

Looking forward, as the inflationary pressure continues to moderate, LNN’s margin should improve. The LIFO headwind that the company saw during the inflationary raw material environment should turn into a tailwind as raw material prices correct. Along with this, the pricing actions taken over the last few quarters should benefit the margins. The company is also looking for opportunities to improve its productivity and grow margins. Hence, I am optimistic about the company’s margin growth prospects.

Valuation & Conclusion

The stock is currently trading at 22.34x FY23 consensus EPS estimate of $6.81 and 21.02x FY24 consensus EPS estimate of $7.24, which is at a significant discount to its five-year average forward P/E of 34.14x. Investors seem to be worried about a slowdown in topline growth after a very strong last couple of years. However, I believe this slowdown is already getting reflected in the stock price at the current valuation. The company can still post good earnings growth despite moderating topline growth, given its good margin improvement prospects. The margins should benefit from the moderation in higher input costs, higher price realization, and productivity improvement opportunities. Given the good margin growth prospects and lower-than-historical valuations, I have a buy rating on the stock.

Be the first to comment