NoDerog

All stock charts are courtesy of Barchart.com unless otherwise noted.

All currency amounts are in U.S. Dollars unless denoted otherwise.

The following True Vine Letter was originally published for Premium subscribers on November 29, 2022. The chart has been updated.

This Letter is a follow-up to a recent Letter where I selected Church & Dwight (NYSE:CHD) as #8 on my list of 8 large capitalization (cap) stocks to buy in a capital flight away from a debt doom loop (or just after a major stock market sell-off).

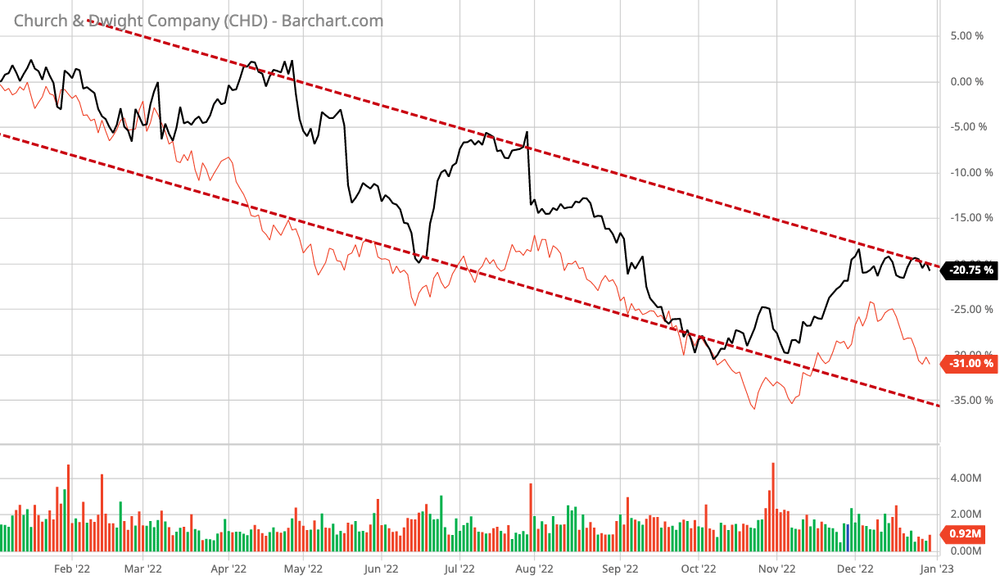

Let us start with the following daily chart which compares CHD (black line) to the iShares 20+ Year Treasury Bond ETF (TLT) (red line) which is a proxy for long duration U.S. Treasury bonds:

Barchart.com

The dotted red lines are the weekly trend channel for CHD.

As you can see here, shares of CHD have been trending lower in lock step with long-term interest rates. If long-term interest rates are going to move higher—which I think they will due to the significant amount of debt the U.S. Treasury will have to sell in the very near future—then shares of CHD are likely to take another dive lower.

Shares of CHD are trading for about 19 times my 2023 of estimate of free cash flow. This is a little over a 5% free cash flow yield. For a durable business like Church & Dwight with stable cash flows, this is a decent price but not an exceptional value. It has the conservative elements of a bond, yet with significant long-term growth upside. Investors buying here are unlikely to lose money over a 3 to 5 year time horizon and likely to double their money by the end of the decade. However, investors who can get the stock for $60—a 25% decline from current levels—would be able step into it with a 7% free cash yield and the potential to triple or even quadruple their money by the end of the decade. Here is where I hope my previous analysis of bond market liquidity can add value. Another strong upward spike in interest rates, coupled with a severe stock market sell-off, has the potential to drive CHD to the $60 level. The caveat here is that if the recessionary outlook continues to worsen, investors may dump cyclical stocks (Banks, Energy, Industrials, and Materials), and soak up Treasury bonds and safer Consumer Staple stocks like CHD. In other words, fearful investors may come to the rescue of the bond market—keeping long-term yields suppressed—which would likely be bullish for CHD. Given all this, my approach here has been to start a very small position in CHD (below $80) in more conservative portfolios but I plan on making it a larger core position in all portfolios if the stock sells off hard to the $70 and potentially $60 level. To be more clear, I’m talking about something like a 1% position now and potentially a 4% or 5% position if the stock declines to $60.

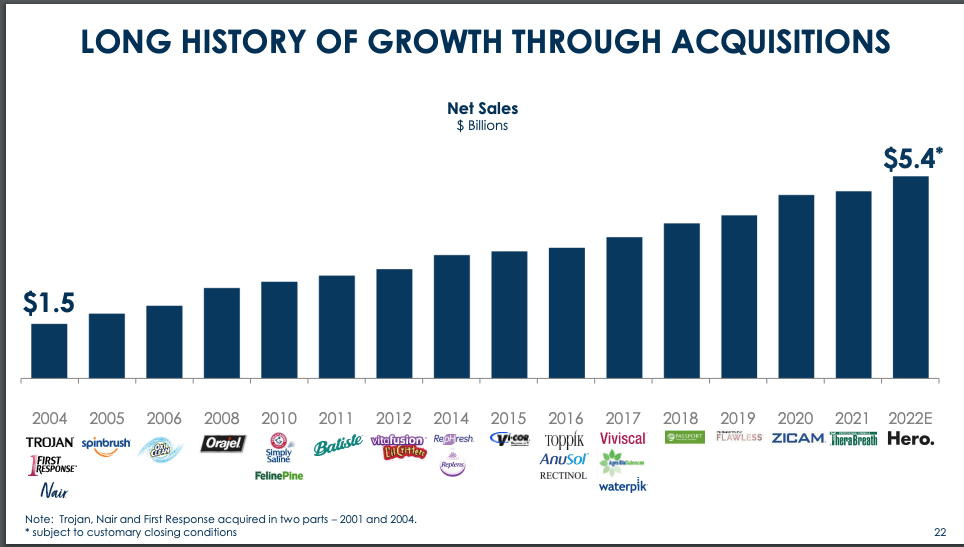

I put together a long-term financial model on CHD which enabled me to calculate that the company has had a 19% incremental free cash flow return on invested capital over the last 15 years. This is important because management’s core strategy is growth through acquisitions of brands that are #1 or #2 in their respective category. This has led to consistent sales growth as the following slide clearly demonstrates:

Church & Dwight Investor Presentation

As CHD expands distribution of its new “Power” brands, ZICAM (cold & flu), TheraBreath (alcohol free mouthwash), and Hero (acne patches), earnings could surprise to the upside in the next few years. The 19% incremental free cash flow returns on invested capital provide the historical precedent for management to make this happen going forward as they continue to allocate capital. President and CEO, Matthew Farrell, and Executive VP of Strategy, M&A, and Business Partnerships, Brian Buchert, either held their current roles or other leading management positions when these deals were done. They are experienced and proven. Moreover, my analysis reveals that CHD’s free cash flow returns on invested capital have gradually increased over the last 15 years. The current management team has gradually improved the fundamental profitability of the business through its strategy. CHD also has the highest revenue per employee amongst its peers, which include notables like Clorox (CLX), Procter & Gamble (PG), and Colgate-Palmolive (CL).

CHD falls into the Consumer Staples sector which tends to be associated with value stocks, however, this is truly a growth stock. Management is guiding for 3% long-term organic revenue growth through a combination of 2% domestic U.S. growth, 6% international growth (mainly Asia), and 5% from its Specialty Products segment which is focused on dietary supplements for livestock. Add to this inflationary price increases, and I expect to see at least 6% average long-term revenue growth.

CHD’s growth potential is also revealed by its lower dividend compared to its peers. Unlike PG and CL, which are paying out roughly 2/3s of income as dividends, CHD is only paying out about 1/3, while investing more in growth acquisitions. This is the right thing to do for shareholders and the strategy is clearly working. CHD’s revenue growth has been roughly twice that of PG and CL over the last several years.

Longer term, there is a significant growth opportunity for CHD in emerging markets, especially in Asia. A business like CHD provides a safe vehicle to invest in this demographic opportunity. CHD’s moves in this realm will be something that I watch closely in the years ahead.

Finally, if a long-term bond yield spike drags down the broader Consumer Staples sector, it may also be a good time to pick up another stock in this category. I am going to do some more research, preferably for another more “growthy” stock like CHD. Such a yield spike may very well lead to a financial crisis and deep recession which would ultimately benefit stocks in the Consumer Staples sector.

Joshua

Be the first to comment