Wirestock/iStock via Getty Images

The Investment Plan

Chord Energy Corporation (NASDAQ:CHRD) is based in the United States, with most of its operations taking place in North Dakota and Montana. Here, the company engages in the exploration of hydrocarbon and hydraulic fracturing. Besides exploring for the mentioned products, Chord Energy is also invested in looking for natural gas and oil sources. Once the company acquires the sites, it exploits and develops them to then sell the product to its rather large customer base in the United States.

Chord is a fast growing company where it has managed to maintain a high net margin. But the valuation right now is a little bit too rich. Despite that, holding any shares in the company might be best as the future remains very bright for them. Adding on share price drops could be a good strategy to help reduce the average price paid.

Latest Earnings Report Highlights

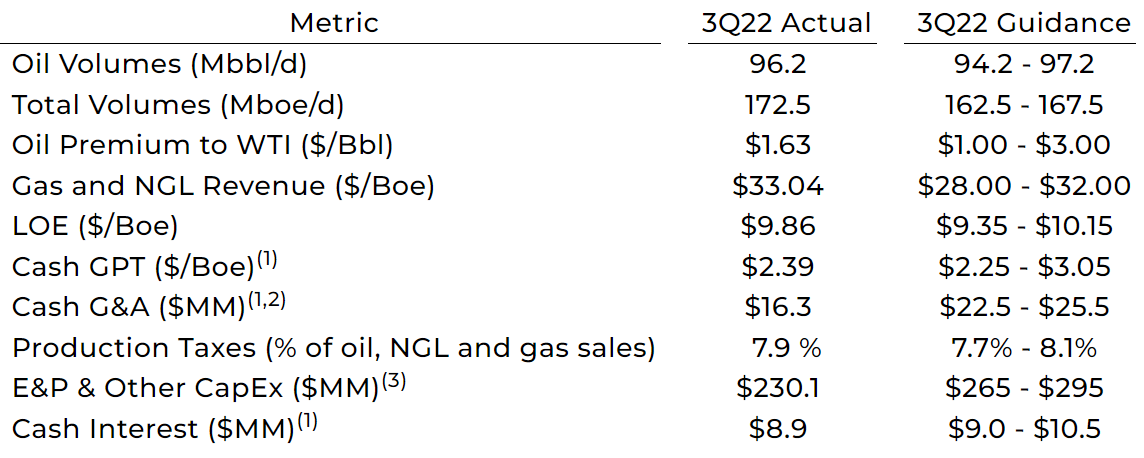

On November 2, 2022, Chord Energy provided investors with their Q3 earnings report. The company managed to beat their production guidance and topped out at 172.5 MBoe/d. In terms of revenues they came in at just above $1.1 billion. Compared to last year’s quarter this was an increase of 222%. I think a big reason for this impressive increase is the much higher commodity prices we saw in 2022. For companies like Chord this has been a double edged sword. On one side it brings in more money to the company, but it also gets increasingly difficult to make assumptions about the future.

Chord operating Volumes (Chord Q3 Report)

Looking at the bottom line, EPS climbed to $22.79. At the current valuation, the company’s share price seems very favorable. But like I said, assuming the future becomes difficult and boom and bust cycles are a real thing, the same goes for gas and oil prices.

Given this larger revenues for the company, they made use of it and purchased back $125 million worth in shares in the Q3 quarter.

Revenue Statement (Chord Q3 Report)

In terms of what the management sees them going in the future, they remain optimistic. The CEO Danny Brown can be noted saying “Chord’s deep economic inventory, strong margins, low leverage and capital discipline make for a compelling outlook”. I think that if I were an investor in the company, this would be amazing news to hear. Hearing that they will remain capital disciplined is refreshing to hear in my opinion.

Sector Outlook

Chord Energy has managed to diversify their business quite well. This means that in the long term they have set themselves up well to have stable growth. But looking at the sectors they are in, there are some notable headwinds to deal with. With such a larger push towards renewable energy sources, I think that the share price and valuation of companies in the space will stay suppressed. Instead, the value will be found through dividends and share buybacks.

Crude Oil Price Outlook (Deloitte)

In the short term, I would expect Chord to see a variable performance, much driven by the latest commodity prices of both oil and natural gas. As they are focused on hydrocarbons, I want to highlight the future of that market. I think that given the volatile markets of oil and gas, hydrocarbons might start tightening down, as a greater focus is placed on the commodities I just mentioned. The lessened supply from Russia with oil and gas can most likely be blamed as a culprit for this too.

Competition

The energy sector is large and there are a lot of companies here fighting to get more market share and drive their competitors to bankruptcy. In the niche that is natural gas and oil, some notable competitors for Chord Energy would be PDC Energy (PDCE), Kosmos Energy (KOS) and HighPeak Energy (HPK).

Even though Chord has seen impressive growth so far, that might start to slow down as it faces bigger competitors. All the companies we have mentioned are also growing at steady numbers, around 15% CAGR EPS for the next 5 years at least. There are some years where the competitors will outperform Chord. HPK seems to have a much brighter future than Chord as their revenues continue to double for the next 2 years as they are expanding rapidly. But what has investors interested in Chord is the yield and shareholder returns the management is focusing on. Looking at the competitors they have the highest dividend yield and a healthy balance sheet to back it up.

The Balance Sheet

Chord Energy is an interesting company to look at when it comes to the balance sheet. They have managed to put in some impressive work and I am excited to see where this is going.

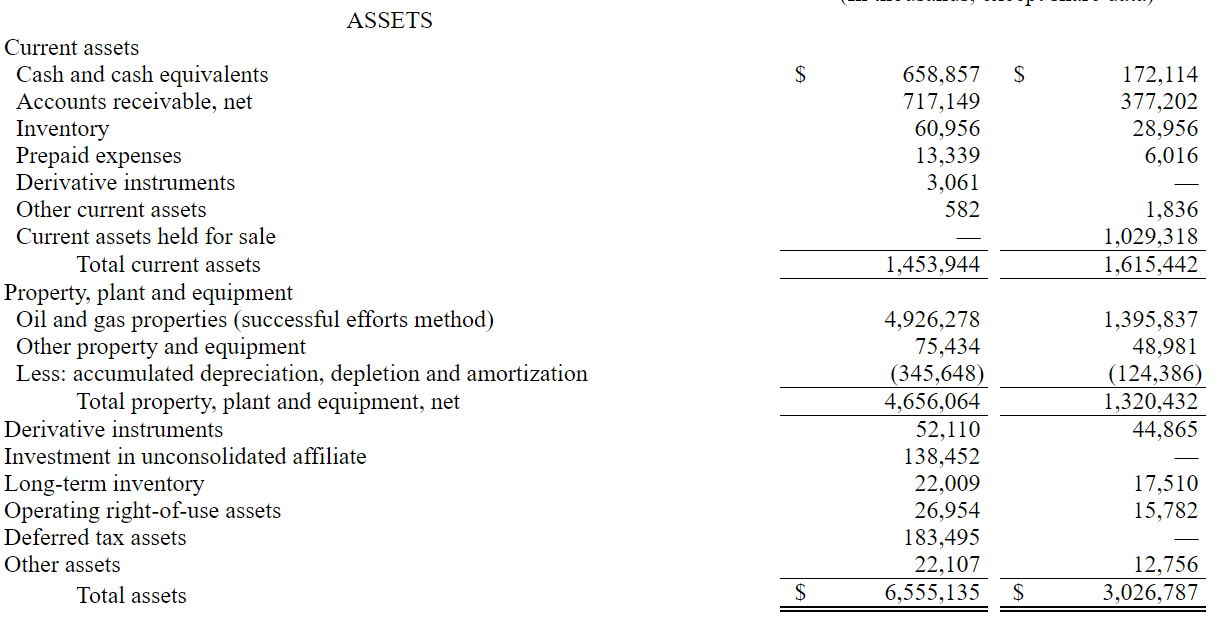

Chord Balance Sheet (Chord Q3 Report)

The management has placed a big focus on increasing the cash position. In the latest report they held $658 million in cash, compare this to 2021 numbers and I see a 282% increase. This is good to see as money is becoming more expensive for companies to get a hold of, but with a tougher economic climate this is good news. It means they have managed to capitalize on the high commodity prices 2022 had.

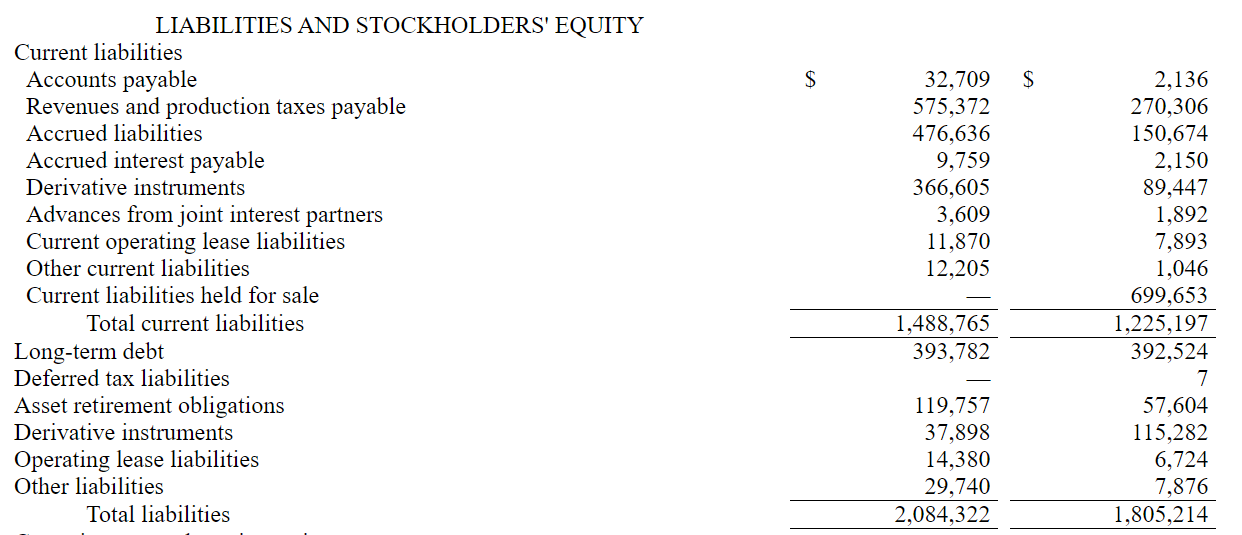

Chord Liabilities (Chord Q3 Report)

Looking at the debt Chord has I don’t think they will have any problems paying it off. With the long-term debt at $393 million the company will have plenty of cash leftover to spend on expansion.

What has caught my eye the most perhaps on the balance sheet is the impressive growth of assets compared to the growth of liabilities. Chord has spent plenty on properties, plants and equipment. They have $4.6 billion worth of it compared to $1.3 billion in 2021.This has led them to having a return on assets of around 6%, but going forward they should be able to leverage their assets further and increase the top line.

Outstanding Shares (Seeking Alpha)

Looking at the outstanding shares for the company I think we have an investor’s dream. The management has spent the last 2 years heavily buying back shares, making use of the increased capital they had at hand and the undervalued share price too.

Cash Flow History (Seeking Alpha)

The cash flow for the company has just like the balance sheet seen good growth. The last few years they have maintained a positive cash flow, which impresses me as I have seen plenty of established companies not able to achieve that. For the future I think they can maintain and grow this whilst also spending a little on buying back more shares.

Valuing The Company

Chord is an interesting case to put a price target on. From the continued growth the company has seen it should trade at a much higher price. But with future being unsure about whether they can keep this growth up, the current valuation is low.

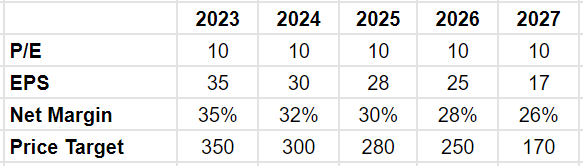

Valuation Estimates (Author’s Own Calculations)

The p/e I have set for the company is a terminal 10. This is slightly above the average of 8 in the sector. But I think they deserve this as they have been growing rapidly in the last few quarters and they seem to have a strong net margin too.

I do think that this growth will slow down and eventually go down even. As the company starts to experience higher operating expenses, this will start affecting the bottom line. The prices of the commodities they are operating with will in my opinion stay very valuable for many years ahead. Instead I think that the costs for exploring and setting up production will become more expensive as perhaps new legislation is introduced, further pushing companies to favor renewable energy sources instead.

Price Chart (Seeking Alpha)

But at the current price the company seems to offer an annual return of 6.2% if my calculations are correct. This is below the target I have of at least 12-13%. But if the management manages to keep costs down and maintain a high net margin, then I can see the EPS being higher and in turn the price targets too. Right now though I think just holding on to shares is the best course of action. Perhaps we see lower share prices where a better entry point could be made.

Conclusion

Chord Energy has managed to handle the last few volatile years very well and has come out on top. With revenues increasing fast and not at the cost of a lower net margin. I think the company is set up well for the future.

Looking at the sector, the need for oil and natural gas will be with us for a very long time. Eventually, we will adopt completely to renewable energy, but until then there is a lot of money to be made in the industry still.

The management has placed a big focus on increasing the available cash as they generate impressive cash flows. This sits very well with me as hedging against hard financial times is vital for me.

All in all, I think investing into Chord right now might not be the best. Holding onto shares is perfectly fine, but a potential drop in share price is not unrealistic. I think there will be better opportunities in the short term to add to the company.

Be the first to comment