Brad Barket/Getty Images Entertainment

Scholastic Corporation (NASDAQ:SCHL) is a publishing company with a very strong backlist primarily focused on the US. Among its titles are Harry Potter, which remains a major seller. They have been hurt by COVID-19, but with a normalised environment this year, operations have had the opportunity to improve ahead of even pre-COVID levels. While this might reflect pent-up demand, as historically revenues have been consistently a step below TTM levels, the improvements are happening in the biggest needle-movers, and were bolstered by especially wise inventory management practices by management. Operations look good overall despite some challenges in selling software, but the valuation is just not compelling in the current environment where deals can really be found. Pass.

How were SCHL Q2 Earnings?

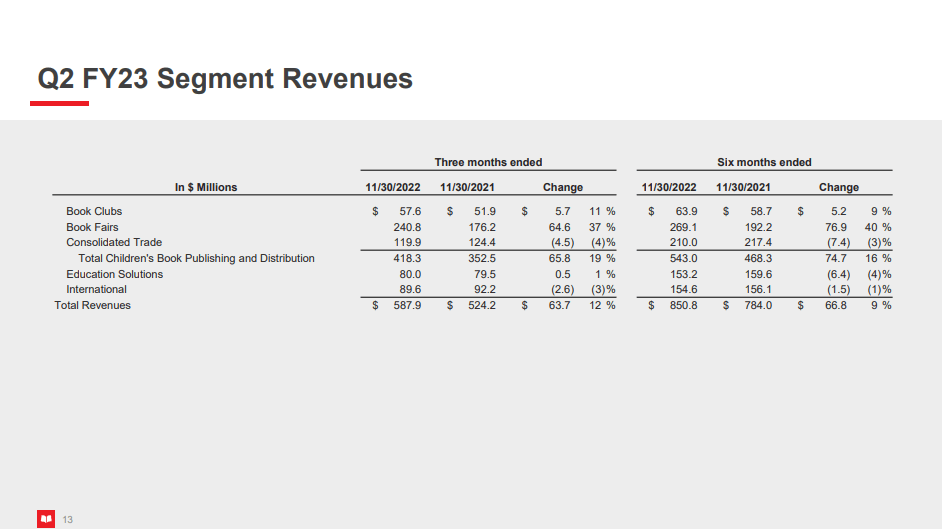

Revenues comprehensively were up 12%, with the driving force being the book fairs. I remember fondly Scholastic’s Book Fairs, where the company would set up a massive stand in our atrium filled with perfect titles for primary and middle school students. The operating leverage is big on these events, and the ease of marketing is extraordinary. This is a higher margin component of the mix for sure, with EBITDA having growth around 20% comprehensively for SCHL thanks to higher book fair revenues in the mix.

Segment Data (Q2 2023 Pres)

Clubs did reasonably well too despite teachers being really busy causing troubles finding schools with the bandwidth to run the clubs, and overall the children’s book segment was the clear winner ahead of educational services which was plagued by several issues. Firstly, as in most industries, we’ve been seeing higher lead times on closing transactions for services, and the other thing is that implementation has been difficult due to labour issues. This quarter actually includes A2i revenues which has now been integrated, which means that adjusting for the acquisition growth in services would have been negative in all likelihood.

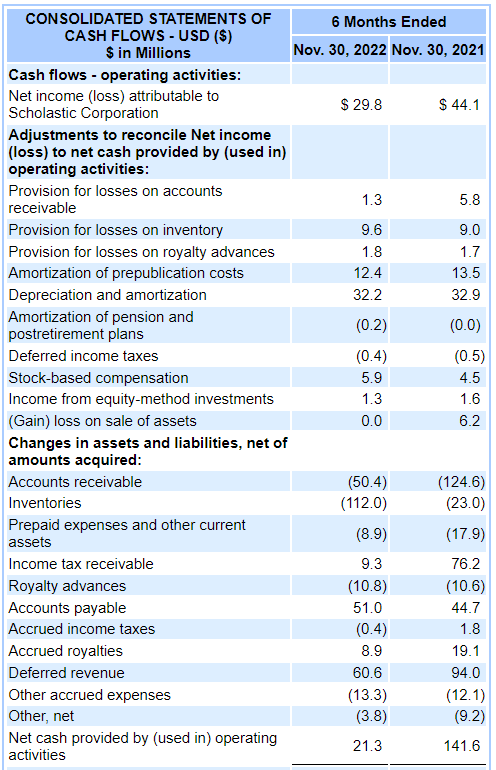

The cash flow statements are worth looking at this year as they are peculiar.

Cash Flows (SEC.gov)

Operating cash flow plummeted, and it’s coming from inventory build because of supply chain issue precautions. Since Scholastic depends heavily on the back-to-school season, they needed to ensure they had the inventory. It let them run a huge book fair push this year that likely saw some pent-up demand effects. As that inventory liquidates onwards, we should see those cash flow figures come up.

Bottom Line

Pent-up demand effects were noticeable.

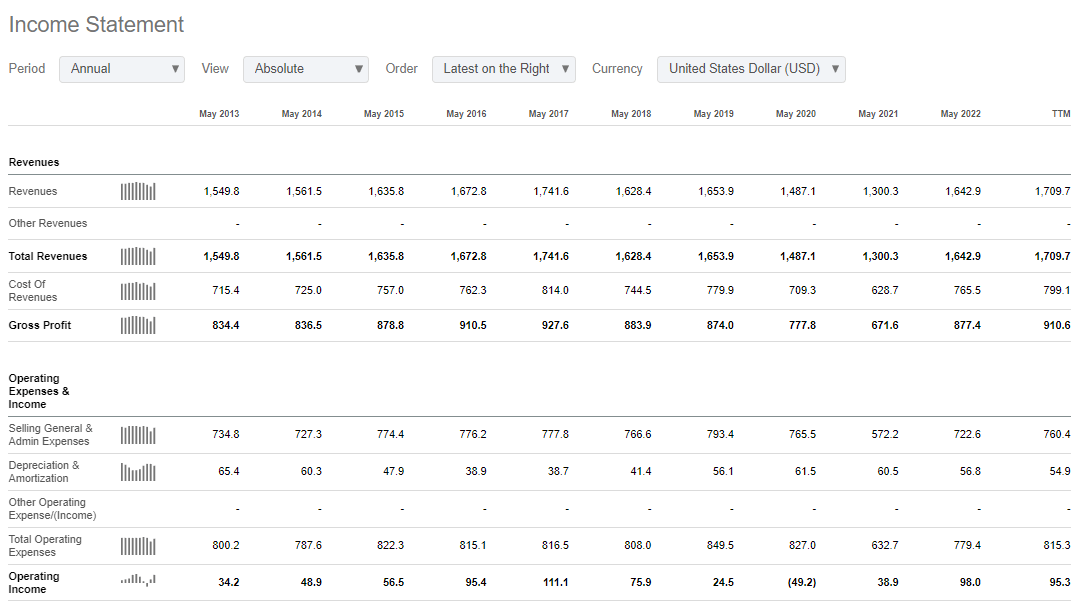

Financials (Seeking Alpha Financials)

TTM revenues are now ahead of even the pre-COVID period, after two years of a more complex COVID-19 situation which saw sharp income declines on the loss of book fairs in the mix. Things are more than back to normal. Since growth is coming from traditional categories that ultimately depend on demographics, rather than any other secularly growing forces, we think the demand push this year is going to be a one-off. Educational services are supposed to be what’s responsible for the longer-term growth.

The P/E is running at a 21x. While we don’t have a concern about growth, even if this year is going to be a peak, 21x is just not a good deal in the current markets given what we think will be a rationalising SCHL picture after the first clean year back at school. Many deals trade at less than half that multiple with better growth prospects, and we would continue to evaluate those over SCHL. A pass.

If you thought our angle on this company was interesting, you may want to check out our idea room, The Value Lab. We focus on long-only value ideas of interest to us, where we try to find international mispriced equities and target a portfolio yield of about 4%. We’ve done really well for ourselves over the last 5 years, but it took getting our hands dirty in international markets. If you are a value-investor, serious about protecting your wealth, our gang could help broaden your horizons and give some inspiration. Give our no-strings-attached free trial a try to see if it’s for you.

Be the first to comment