GDMatt66/iStock via Getty Images

It’s hard to think of now, but there was once a period when EV uptake was anaemic. The cars were broadly associated with a certain subset of the population and certainly remained out of reach for most people. This kept the EV economy as a fringe part of global automotive sales, but we are all now living through the most significant generational shift in passenger transport as EV adoption experiences its time in the sun. Campbell, California-based ChargePoint (NYSE:CHPT) is the largest publicly listed EV charging infrastructure pureplay but operates in a crowded space with several other pureplay charging companies like EVgo (EVGO), Tritium (DCFC), and Volta (VLTA) also competing for market share in ChargePoint’s core geographical markets in North America and Europe.

The shift towards lower-emission transportation through EVs is now entrenched in the post-pandemic economic zeitgeist of most developed nations racing to combat anthropogenic climate change. Whilst this shift is still in a very early stage, the pace of growth is material and dramatic. Indeed, in 2012 just 120,000 EVs were sold globally. Last year saw this figure being sold on a weekly basis with 10% of cars sold in 2021 being electric, 4x the market share in 2019. For EV sceptics, internal combustion engine vehicle sales have already flatlined in numerous developed nations where ChargePoint has a presence. Indeed, Bloomberg New Energy Finance released a report in the summer which stated that sales of gas and diesel-powered vehicles already look to be realizing a permanent decline as more and more consumers opt to go for EVs or plug-in hybrids. EVs are forecasted to grow to at least 26.8 million by 2030, up from 6.6 million in 2021.

What does this mean for ChargePoint? That its total addressable market is fast expanding which places the expansion of its charging points on the type of upward adoption ramp that would make enterprise software companies somewhat jealous. Indeed, the company reported revenue growth for its last earnings quarter of 93%. Critically, it also means operations can be put on a type of certain type of autopilot where the company just focuses on building out its footprint in great locations with the demand already set.

Revenue Goes Vroom But Cash Burn Still Elevated

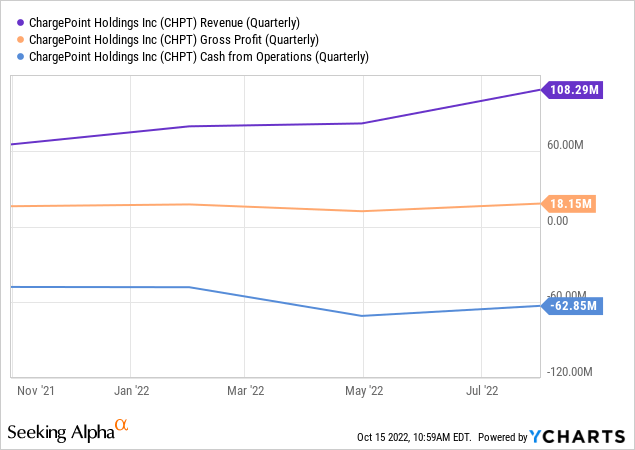

The company last reported earnings for its fiscal 2023 second quarter, which saw revenue come in at $108.29 million, a 93% increase from the year-ago quarter and a beat of $5.26 million on consensus estimates. This was driven by a 106% growth in revenue from Networked Charging Systems to $84.1 million with Subscription revenue notching lower growth at 68% to reach $20.2 million from $12.1 million in the comparable year-ago period.

The company’s gross profit margin at 17% was a 200-basis point decline from the year-ago quarter. Management during their earnings call stated that this was due to supply chain disruptions affecting inventory availability and increasing new product introduction costs. This still saw a gross profit of $18.2 million, its highest number on record. However, cash burn continues to run hot with cash loss from operations at $62.9 million during the quarter. When aggregated with capital expenditures of $5.7 million, free cash outflow was just under $70 million. Hence, whilst cash and equivalents of $471.9 million as of the end of the quarter will provide leeway for the company to keep on funding growth, there are 7 quarters left of such growth assuming the current pace is maintained.

Management has set a goal to be free cash flow positive by the end of calendar 2024 with operating expenses as a percentage of revenue being a key metric to watch. This dropped sequentially from over 100% to 74%. With the company’s market cap at $4.28 billion, it trades on an 8.9x price to forward sales multiple. This is materially higher than its sector median of 1.16x forming the main legs of the short base on ChargePoint. The company is expensive, reflecting its growth and the opportunities posed by its vast and expanding market but exposing longs to rerating risks.

ChargePoint Is Moving To Own The Infrastructure For The Future Of Transportation

The future of automotive transport is EVs. As transport moves from gas and diesel-powered vehicles, ancillary companies serving the EV space stand to ride an upward demand ramp. These pick-and-shovel plays are EV brand agnostic and save the stress of trying to pick the winners. And whilst cash burn is high now, it’s critical that the company expands its footprint heavily in these early stages with an asset that will produce cash flows for years.

Further growth is set to come on the back of the recently signed Inflation Reduction Act. The Act is extremely consequential with $370 billion allocated over 10 years to decarbonization initiatives. There will be a $7,500 electric vehicle tax credit running from January 2023 until December 2032, providing a boost for the fledging yet fast-growing US EV sector. Fundamentally, we are still in the very early innings of the global shift towards EVs. US plug-in electric vehicles still account for around 1% of all cars on the road. This paints a vivid picture of a strong high-growth future for ChargePoint, albeit at an expensive price.

Be the first to comment