Hanis/iStock via Getty Images

A few months ago, I wrote a positive article on Centrus Energy Corp. (NYSE:LEU) as a differentiated way to play the uranium investment theme. Recently, Centrus Energy reported their Q3 earnings and the stock plunged over 30%. What is going on and should investors bail on the story?

The headline earnings miss was unfortunate, and caused many uninformed investors to sell their shares of Centrus Energy. However, those who understand the story should not have been surprised, as the large revenue delta in the Technical Solutions segment was well telegraphed. I remain constructive on Centrus Energy given the large spread between the market price of SWU under long-term contracts and Centrus Energy’s contracted supply costs. I would view this pullback as a great opportunity to buy shares.

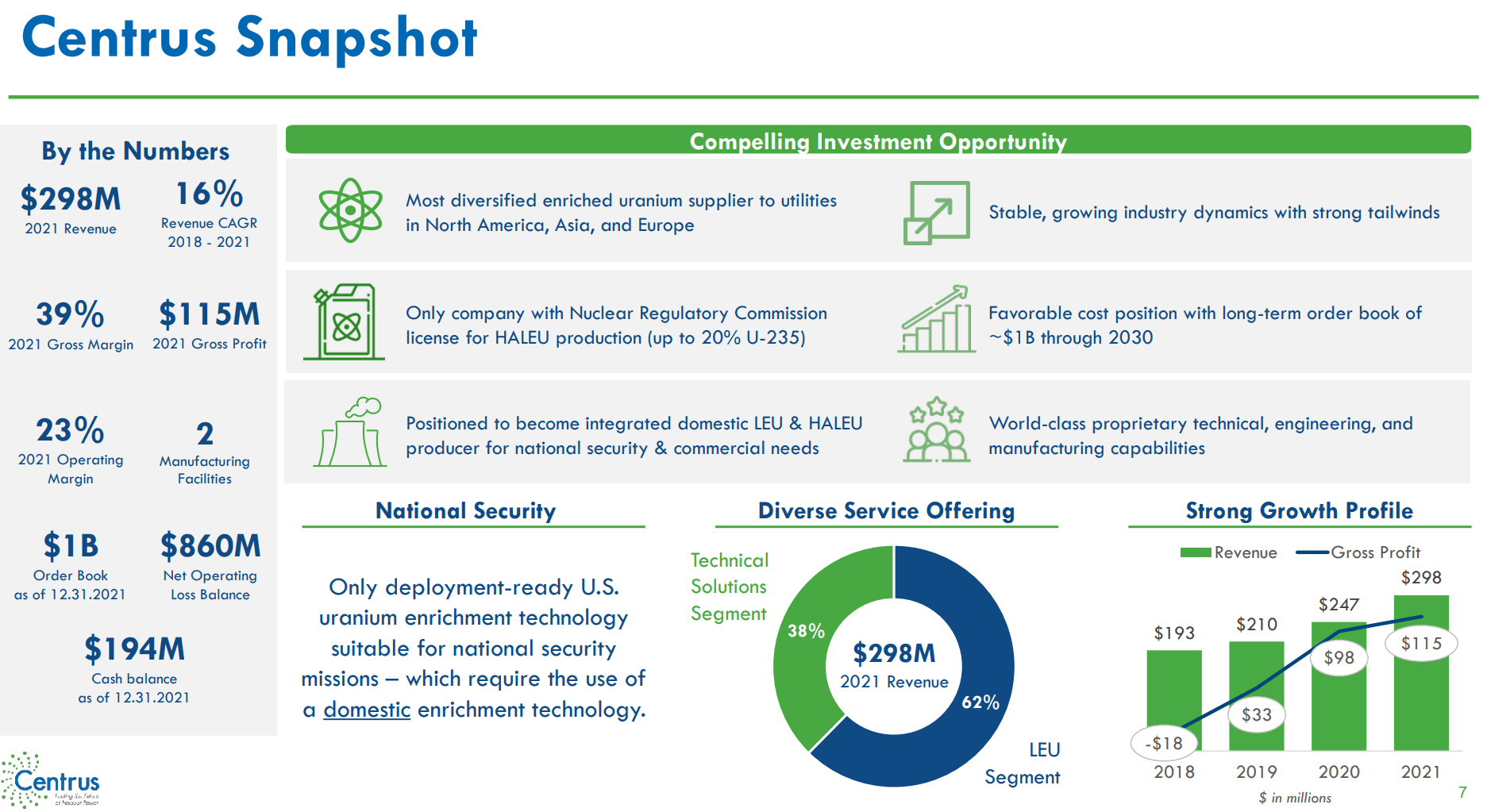

Brief Company Overview

For those not familiar with the story, Centrus Energy Corp. is a leading nuclear fuels supplier to North American, European, and Asian utilities. Centrus Energy supplies Low Enriched Uranium (“LEU”) fuels to utilities as well as provide technical consulting services to governments and private sector customers (Figure 1).

Figure 1 – Centrus Energy overview (LEU Investor Presentation)

Disaster Quarterly Earnings – What Happened?

Admittedly, I was surprised by the stock reaction to Centrus Energy’s latest quarterly earnings report, which saw LEU stock fall more than 30% from $45 to $31. What happened?

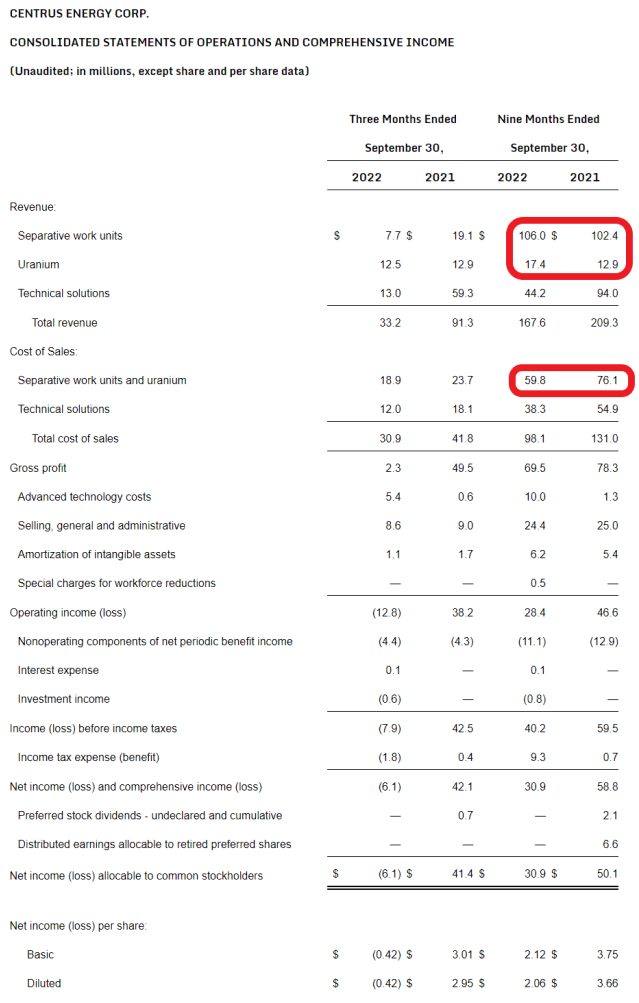

For the third quarter, Centrus reported revenues of $33.2 million, a 64% YoY decline, and net loss of $6.1 million in the quarter compared to $42.1 million net income in the prior year’s quarter. The large YoY decline in revenues and earnings was probably the reason Centrus’ stock took a dive.

One-Time Reimbursement In 2021 Should Not Have Been A Surprise

However, reading into the details of the quarterly report, the actual quarterly performance was not that bad. First, the large YoY revenue decline in the Technical Solutions segment ($13 million vs. $59.3 million YoY) is mostly explained by $43.5 million in reimbursement of prior work that I highlighted in my prior article:

Note that 2021 and LTM results include a $44 million settlement of claims related to the reimbursement of pension and postretirement benefits from prior work. This settlement is recorded as revenues in the Technical Solutions segment and is worth ~$3/sh in pre-tax income.

The underlying Technical Solutions business only saw revenues decline $2.8 million. More importantly, while the prior year’s quarter had $18.1 million in costs, this quarter only saw $12 million in costs. So contribution margin in the Technical Solutions segment was actually positive $1 million ($13 million less $12 million in costs) in Q3/2022 vs. -2.3 million ($59.3 million less $43.5 million from one-time reimbursement less $18.1 million in costs) in Q3/2021. In any event, the Technical Solutions segment is not the main driver of corporate earnings.

Lumpy Uranium Business Still Looks Good YTD

Secondly, the LEU segment is notoriously lumpy, as it involves long-term contracts with utilities at various price levels. Third quarter revenues came in at $20.2 million vs. $32.0 million YoY, with COGS of $18.9 vs. $23.7 million YoY. Gross margin for the LEU segment was only $1.3 million vs. $8.3 million in Q3/2021.

However, viewed on a YTD basis, the LEU segment has generated $123.4 million in revenue, a 7% increase from $115.3 million in 2021. Moreover, the gross margin is also much higher in 2022, at $63.6 million vs. $39.2 million YoY (Figure 2).

Figure 2 – LEU Q3/2022 Financial Statement (LEU Q3/2022 Press Release)

Adjusting for the one-time reimbursement in 2021 ($43.5 million), operating income actually grew from $3.1 million YTD 2021 to $28.4 million YTD 2022.

Elevated Fuel Margins Signal Improved Earnings Going Forward

When asked on the earnings call about the revenue lumpiness in the third quarter, management provided this commentary: (note, I have highlighted passages that I think are important)

Rob Brown

Okay, great. Thank you for that color. And then, just kind of thinking through the lumpiness of the business, I know your annual numbers are pretty solid and they move around for the quarter. But just want to confirm any sort of changes in the market, or this is truly just a timing and delivery kind of quarter and things sort of pick up or change annually, they maintain where you thought they’d be?

Dan Poneman

Yes. It’s truly lumpiness. In other words, the things that you see in the market, you can see in the price curves that we mentioned in the original laydown. The prices were $56 per SWU before all of the challenges we faced in Europe and now they’re $135 long-term market.

And as you know, most of the business is contracted long term. So those are very strong price trends. And with the continued unrest in Europe and in addition, the secular increase in climate-driven concerns and the consequent — the traction of nuclear, we think that aspect is solid.

As we noted, we have booked a lot of sales ourselves in the last three quarters. So it’s just generally and genuinely the lumpiness, because different contracts get deliveries in different quarters. And it just doesn’t even out except over a year-to-year kind of basis.

– Earnings call exchange between Rob Brown, an analyst with Lake Street Capital and Dan Poneman, the CEO.

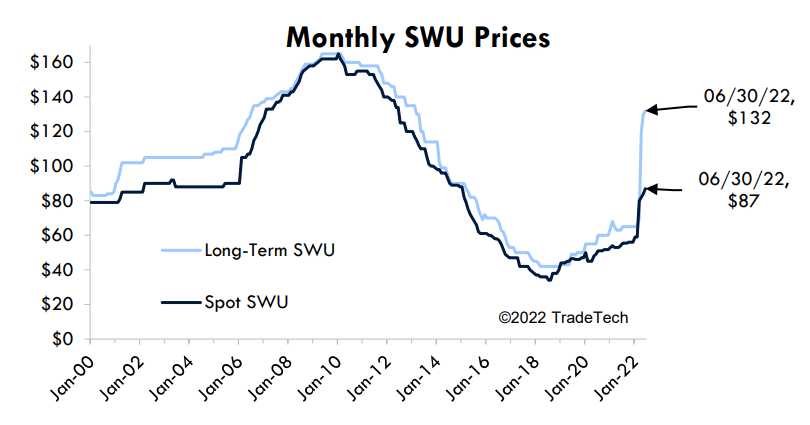

In fact, with Separate Work Units (“SWU”) pricing over $130 in the long-term market currently, the $270 million in contracts booked YTD is probably locking in high margins for years to come (Figure 3).

Figure 3 – Monthly SWU Prices In long-term market (LEU Investor Presentation)

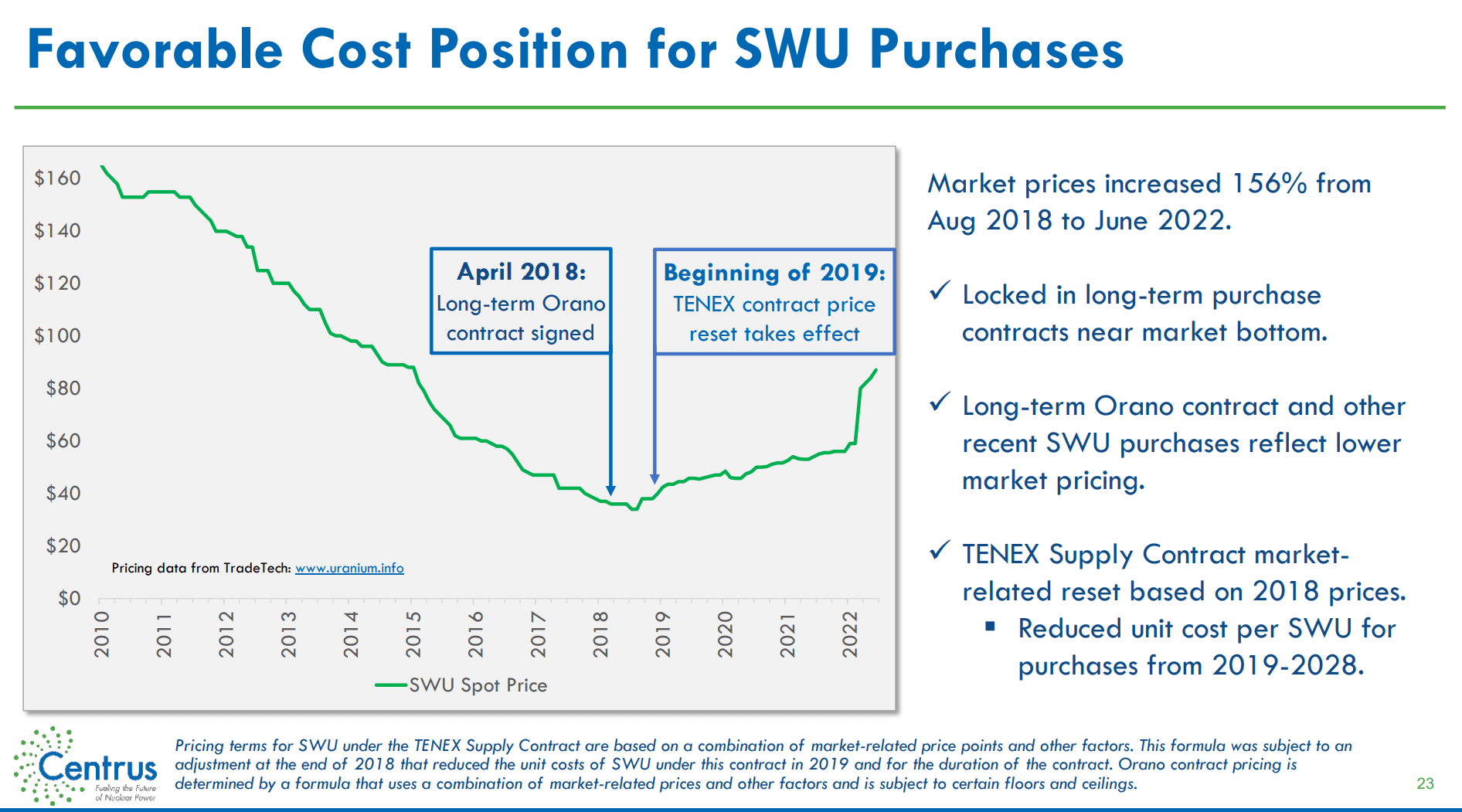

As a reminder, Centrus Energy locked in long-term supply of uranium and SWU units near the depths of the uranium bear market (Figure 4). The spread between market rates for SWU and Centrus Energy’s cost is the main driver behind my bullish thesis.

Figure 4 – LEU cost of uranium and SWU (LEU Investor Presentation)

Deferred Tax Asset Unused This Quarter

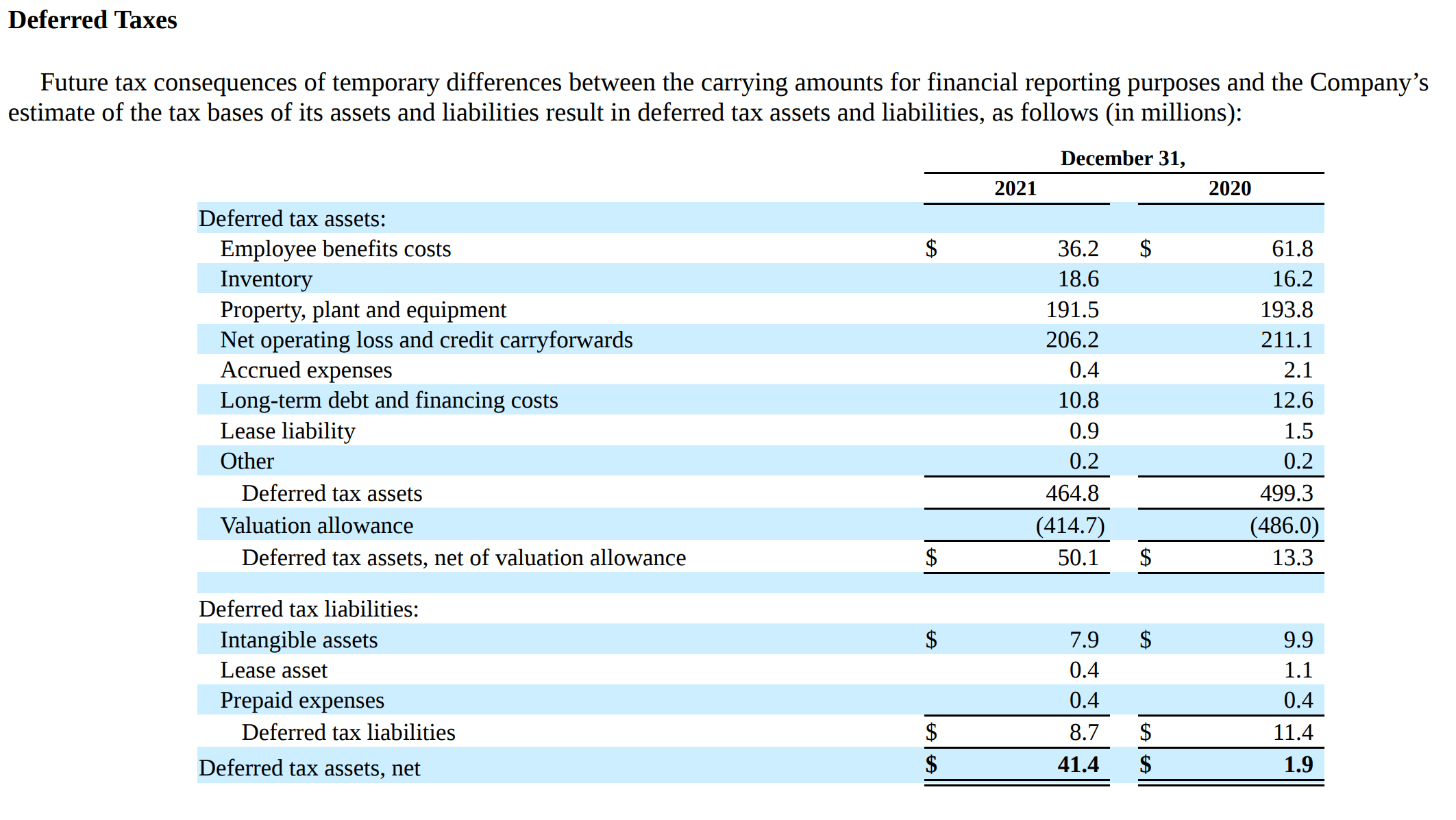

As the third quarter did not generate a profit, Centrus Energy’s large deferred tax asset was not used. As a reminder, from the company’s 10K report, we can see that LEU has deferred tax assets worth over $400 million or $28 / share that the company had booked a valuation allowance against (Figure 5). This should shield the company from paying income taxes for years to come.

Figure 5 – LEU has large deferred tax assets (LEU 2021 10K Report)

Russian Supply Remains Biggest Risk

In my opinion, Centrus Energy’s biggest risk remains its Russian supply of enriched uranium. I explained this in my prior article:

Currently, Centrus imports a significant portion of its uranium from Russia under the ‘TENEX Supply Contract’. Although Centrus has multiple sources of supply, including a long-term supply agreement with the French nuclear conglomerate Orano, the company noted in its annual report risk section that:

If measures were taken to limit the supply of Russian LEU or to prohibit or limit dealings with Russian entities, including, but not limited to, TENEX or ROSATOM, the Company would seek a license, waiver or other approval from the government imposing such measures to ensure that the Company could continue to fulfill its purchase and sales obligations. There is no assurance that such a license, waiver, or approval would be granted. If a license, waiver or approval were not granted, the Company would need to look to alternative sources of LEU to replace the LEU that it could not procure from TENEX. The Company has contracts for alternative sources that could be used to mitigate a portion of the near term impacts. However, to the extent these sources were insufficient or more expensive or additional supply cannot be obtained, it could have a material adverse impact on our business, results of operations, and competitive position.

As long as the TENEX Supply Contract continues to be honoured, Centrus Energy should continue to enjoy the benefits of elevated SWU prices.

Conclusion

The headline earnings miss was unfortunate, and caused many uninformed investors to sell their shares of Centrus Energy. However, those who understand the story shouldn’t have been surprised, as the large revenue delta in the Technical Solutions segment was well telegraphed. I remain constructive on Centrus Energy given the large spread between the market price of SWU under long-term contracts and Centrus Energy’s contracted supply costs. I would view this pullback in Centrus Energy Corp. as a great opportunity to buy shares.

Be the first to comment