peshkov/iStock via Getty Images

Investment Thesis

Cenovus Energy (NYSE:CVE) reported very strong and clear guidance on its capital allocation strategy. After Cenovus got lower than $9 billion of net debt, it got busy returning 50% of free cash flow to shareholders.

Given that Cenovus is now on its way to $4 billion of net debt, management has started turning on the spigot. By my estimates, in Q3, 100% of its free cash flow will be returned to shareholders.

I explain why paying 5x its 2023 free cash flow is an attractive multiple for Cenovus.

The Larger the Cap The Better The Performance

The reason why I love investing is that anyone can build a narrative about why they are so smart when the share price is moving up. We all inadvertently do it. We delude ourselves. But we are never that smart. A bull market hides a lot of stupidity. And the same works in a bear market. Everything is going wrong, but we are never that dumb.

When it comes to investing in oil and gas companies, I argue that the performance of the company has a lot more to do with the size of its market cap than it does with the underlying performance of the business.

For someone invested in Cenovus, this is nothing short of blasphemy. Yet, I remark that the bigger the market cap, the more liquid the stock, the easier it is to deploy capital into that stock, the strong the flow of capital, and then, the rapidly ascending share price will create its own momentum, from traders jumping on the oil wagon.

Cenovus’ Near-Term Prospects

Cenovus is the third-largest Canadian oil and natural gas producer. Cenovus is a low-cost oil sands operator.

In my previous Cenovus article I remarked that Cenovus’ opportunity was mixed given that its balance sheet carries a significant amount of leverage, that will get in the way of Cenovus significantly returning capital to shareholders.

And I have to admit, I was wrong in my estimations.

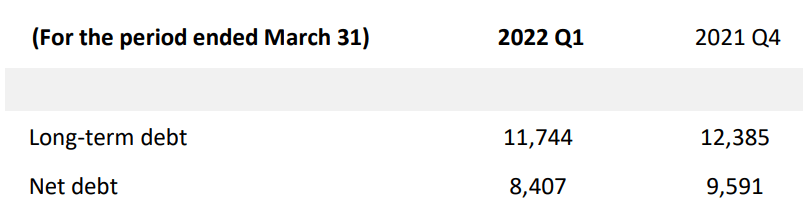

Q1 2022 earnings results

I had an issue with the fact that Cenovus carried such a significant amount of debt. And I didn’t truly believe that Cenovus would be able to be as free cash flow generative as it turned out to be.

What’s more, during the Q1 2022 earnings call management highlighted that it intends on getting its net debt profile down to $4 billion.

Given that Q2 2022 is probably going to make approximately $2.5 billion in free funds flow, this means that at some point in Q3, Cenovus will see its net debt reach that critical $4 billion of net debt marker that management believes is prudent from a risk management perspective.

Furthermore, management highlights to investors that if WTI returns to $45, the business would be around 1x leveraged at that point.

Cenovus called that $4 billion of net debt profile is its ”no regrets” marker. Going on to say,

So I think $4 billion from our perspective is the right level to [get to], but we’re going to commit giving back all the cash flow once we get there.

So, there you have it. A very clear capital allocation strategy, that I’ll discuss next.

Capital Allocation Strategy

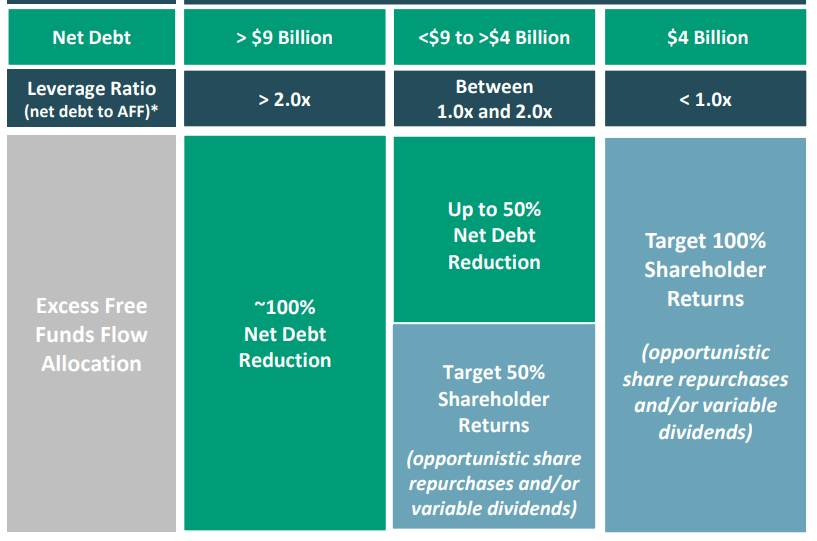

CVE Investor Presentation

Cenovus’ management team laid out a very clear capital allocation policy. When its net debt falls below $9 billion, Cenovus will return 50% of its excess free cash flows via buybacks.

While noting that if management believed that the share price was to rally to significantly higher than intrinsic value, Cenovus would instead look to increase its dividend yield.

CVE Stock Valuation – Still Attractively Priced

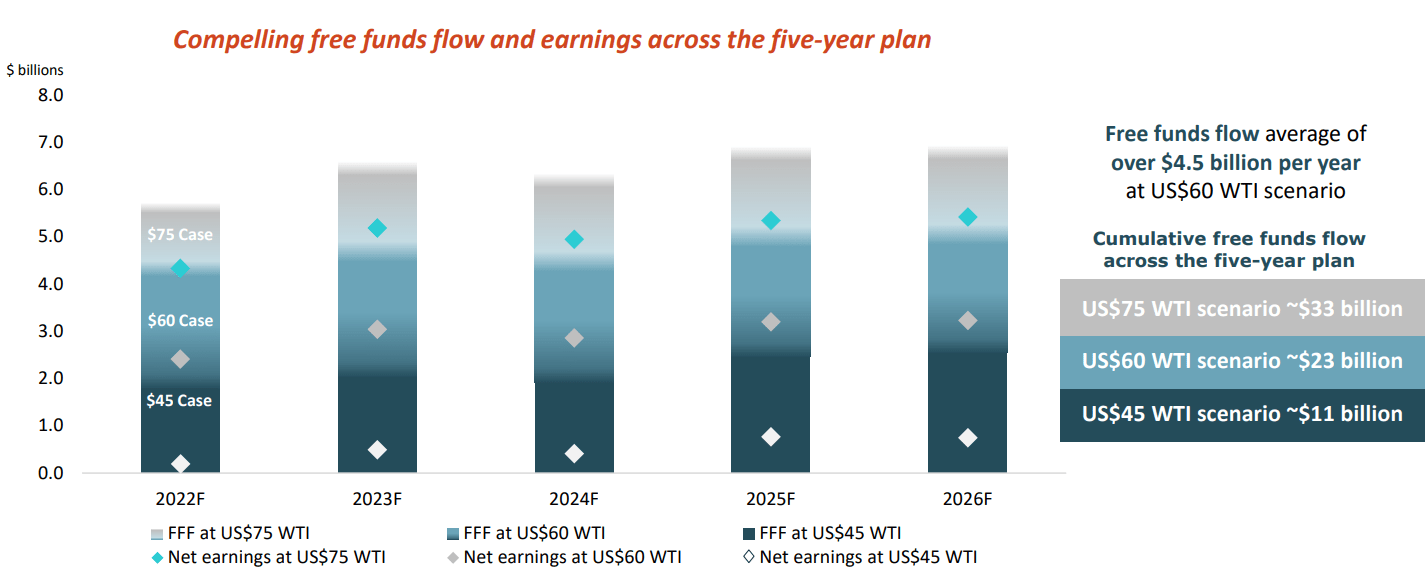

During the Q1 2022 earnings call, Cenovus’ management team, pointed investors’ attention to its December investor day.

CVE Investor Presentation

With Cenovus remarking during the recent call that even at $45 WTI Cenovus would be at breakeven.

If you follow oil and gas companies, you’ll have heard that inflation has increased many companies’ higher breakeven cost, given the increased infrastructure costs, higher labor costs, supply chain constraints, and equipment costs.

Consequently, given that management reiterated its opportunity to still break even at around $45 WTI, this insight is clearly good news and will go a long way to ensure that Cenovus can remain a viable business throughout the cycle.

Now, obviously, nobody can predict the price of oil in 2023. But we must start our math somewhere. If we assume that in 2023 WTI is $100, together with the fact that Cenovus should not have a hedged book at that point, I would be inclined to assume that Cenovus could reach around $11 billion of free cash flow.

For that, I’ve assumed $95 million in free fund of flows for every $1 WTI change (sensitivity table). Given that management points out above that at $75 WTI Cenovus would make around $7 billion, this would see about $10 billion in 2023. But at the same time, Cenovus will have fewer interest payments too, which could perhaps nudge the business closer to $11 billion in free cash flows.

I’ve seen some much higher estimates around, but I don’t believe they sufficiently factor in the higher inflation costs.

This would put Cenovus priced at around 5x next year’s free cash flow figure. A multiple that is very much in line with other oil and gas companies.

The Bottom Line

I noted at the start of the article that the bigger the market cap, generally, the higher the multiple investors are willing to pay for the company. Cenovus is priced at around 5x its 2023 free cash flows, while smaller companies are priced at around 3x their 2023 free cash flows.

That being said, ultimately, all the companies, big or small are driven by the price of WTI, which nobody controls. Both on the upside side or the downside.

Be the first to comment