deepblue4you/iStock via Getty Images

Cazoo’s (NYSE:CZOO) fiscal 2021 earnings results were strong. The London-based online car retailer went public last year on the back of growing European adoption of online car sales. This market is still fast-expanding as Europe’s used car market, a $700 billion opportunity, still has less than 2% of its transactions conducted online. Most analysts expect this shift to online sales for cars to be structural, in that it should form a permanent change in consumer buying behaviour over the long-term with market share of the online sales component likely to increase more than 5-fold over the next decade. Put another way, 1 in 50 European used car sales transactions are currently conducted online, this is set to shift to 1 in 10 by the end of the decade.

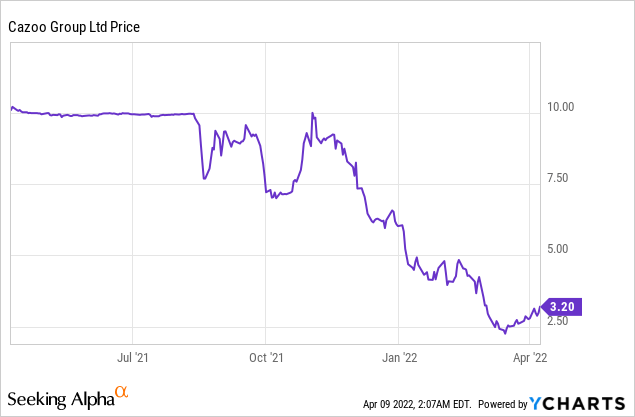

Cazoo’s stock price tells a different tale as investor sentiment for unprofitable growth stocks has waned in the face of a hawkish Fed and a forecasted US recession.

Cazoo’s common shares are now down 68% from its $10 SPAC reference price, but have recovered some ground since the company hit a post deSPAC low of $2.19 a few weeks ago. The core bull case remains the same. Cazoo is gaining first-mover advantage in a heavily fragmented space by building and operating an eCommerce platform that aims to make the car buying experience as seamless as possible. Around 180,000 used car dealerships exist across the largest ten markets in Europe, these have disparate levels of customer experience, financing options, or home delivery possibilities.

Trustpilot

Hence, with 18,500 reviews and a nearly 5-star rating on Trustpilot, Cazoo is trying to seize the day and move to extensively dominate the market. It has bolstered this position with a series of strategic bolt-on acquisitions executed over the last 6 months. The most recent was an €80 million buyout of brumbrum, an Italian online car retailer. This continues its broader strategic plan to conquer the still nascent European online used car market.

Revenue Growth Goes Hyper As GPU Booms

Cazoo is not a stock for every investor. The company is growing rapidly and investing hundreds of millions into its growth to establish and maintain a dominant position in a market set to grow nearly exponentially over the next few years. As a result of this, the company remains unprofitable. This is not entirely tenable in the current climate of mass retrenchment from growth stocks.

The company recently released its fiscal 2021 earnings results which saw revenue for the year come in at £668 million ($870 million). This was a 312% increase from the previous year and came on the back of an increase in vehicles sold during the period. At 49,853 vehicles, this was a 233% increase from the preceding year. Retail GPU also materially improved from negative £229 ($298) in 2020 to £427 ($556) in 2021.

Cazoo expects this positive trend to continue in fiscal 2022 with retail GPU forecasted to hit £900 ($1,171) on the back of revenue set to reach at least £2 billion ($2.6 billion). Cazoo also expects to sell at least 100,000 vehicles at its marketing and acquisition efforts pay off across its large European markets. Longer-term, Cazoo wants to continue its strong direct-to-consumer retail sales proposition to help it reach guidance for fiscal 2024 revenue of around £6 billion ($7.81 billion).

Hence, the company’s current market cap of $2.43 billion comes at a 0.3x multiple to expected fiscal 2024 revenue. Whilst it’s hard to ascertain what future revenue multiple a growth stock will trade on, this is far too much of a discount on growth for financial results that are just 3 fiscal years out. Further, the discount on current growth is likely to be deepened if revenue expectations are outperformed on the back of strong momentum in Europe and further bolt-on acquisitions.

Cazoo was also able to raise $630 million in February through the issue of 2.00% convertible senior notes. This will be aggregated with existing cash and equivalents of $260M as of December 31, 2021 to leave the company with a pro forma cash balance approaching $900 million. Management have stated they expect this to give them a clear runway for at least the next 24 months to execute on their strategy and reach profitability on their UK business.

Cazoo Is A Buy On Divergence Of Market Value From Growth Prospects

Cazoo is a high quality company in a space set to experience material growth in the years ahead. It has unfortunately joined a list of young growth companies that went public last year just as growth investing fell out of fashion. I think the current stock price presents an opportunity to build a long-term position in the company. The broader macro picture for the growth of online used car sales will continue to be strong and Cazoo has a strong position to hover up much of this market.

Be the first to comment