niphon

Investment Thesis

Carrier Global Corp. (NYSE:CARR) is poised to benefit from the implementation of SEER2 regulation in 2023 which is expected to raise the average selling price for the company’s HVAC products. Moreover, the enactment of the Inflation Reduction Act is expected to incentivize its customer in the form of tax credits and rebates to buy high-efficiency HVAC products. Both SEER2 and the inflation reduction act are expected to act as a short to medium-term tailwind for the company’s revenue. In the long term, four secular trends- health and wellness, sustainability, digitalization, and the growing middle-class population are expected to grow CARR’s total addressable market faster than the base GDP growth rate.

On the margin front, the company’s cost reduction efforts are expected to help improve the adjusted operating margin by 50 basis points (bps) annually till 2026. Additionally, management is focused on growing its higher-margin aftermarket segment faster than the company’s average which should shift the company’s sales mix to higher-margin products and services.

CARR Revenue Outlook

During the third quarter of 2022, the company reported revenue of $5.5 billion, up 2% Y/Y. Organic sales increased by 8% Y/Y driven by price increases while the volume was flat Y/Y. The Chubb divestiture reduced revenue by 10% Y/Y and Toshiba’s global residential and light commercial HVAC business acquisition increased revenue by 8% Y/Y. The currency translation was a 4% Y/Y headwind for revenue.

The HVAC segment reported a 22% Y/Y increase in revenue, including 12% Y/Y revenue growth from the Toshiba acquisition. HVAC organic revenue was up 13%Y/Y, driven by high-single-digits growth in residential and double-digit growth in commercial HVAC businesses. Residential HVAC growth was primarily driven by pricing as volume was down mid-single-digits. Revenue in the Refrigeration segment declined by 9% Y/Y primarily due to a significant currency translation headwind, while organic revenue declined by 1%. Within the transport refrigeration business, North American truck/trailer sales were up high-teens Y/Y while supply chain issues affected the European truck/trailer business. On the other hand, demand softness and tough comps resulted in container sales declining 20% Y/Y, dragging overall refrigeration segment revenue. The Fire and security products segment revenue grew 6% Y/Y (excluding the Chubb business) due to favorable demand, partially offset by the impact of supply chain challenges, especially in the higher-margin access solution business.

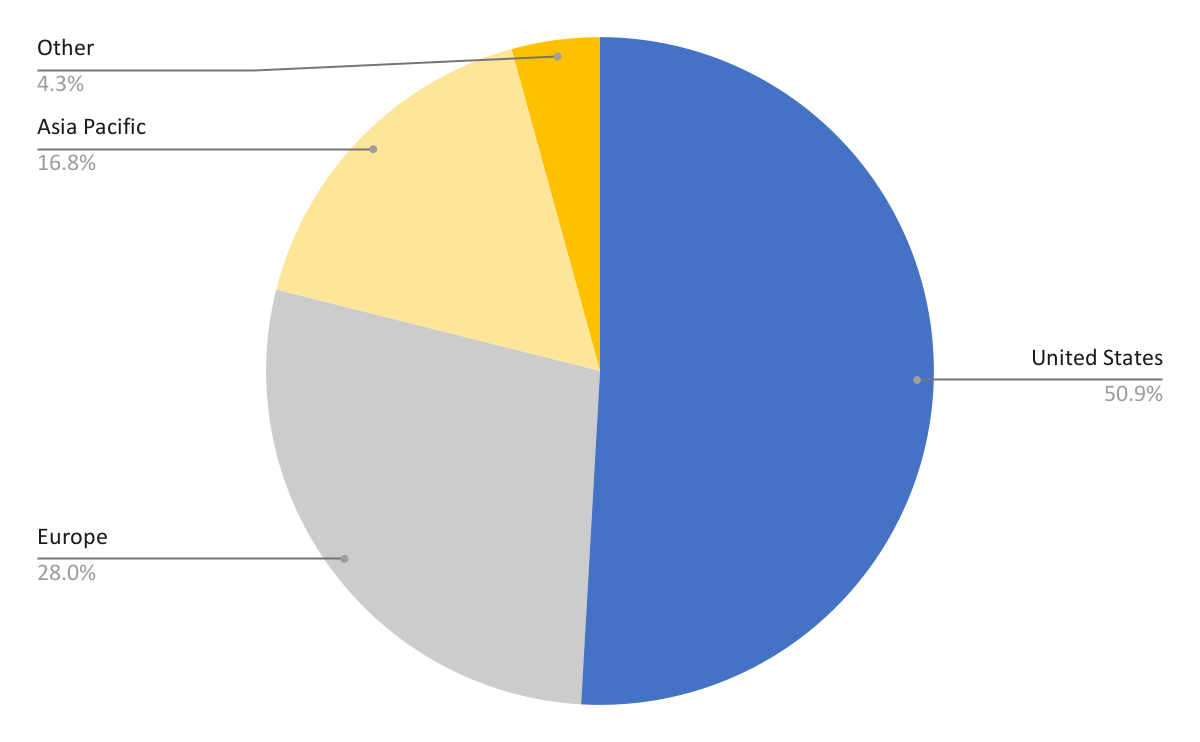

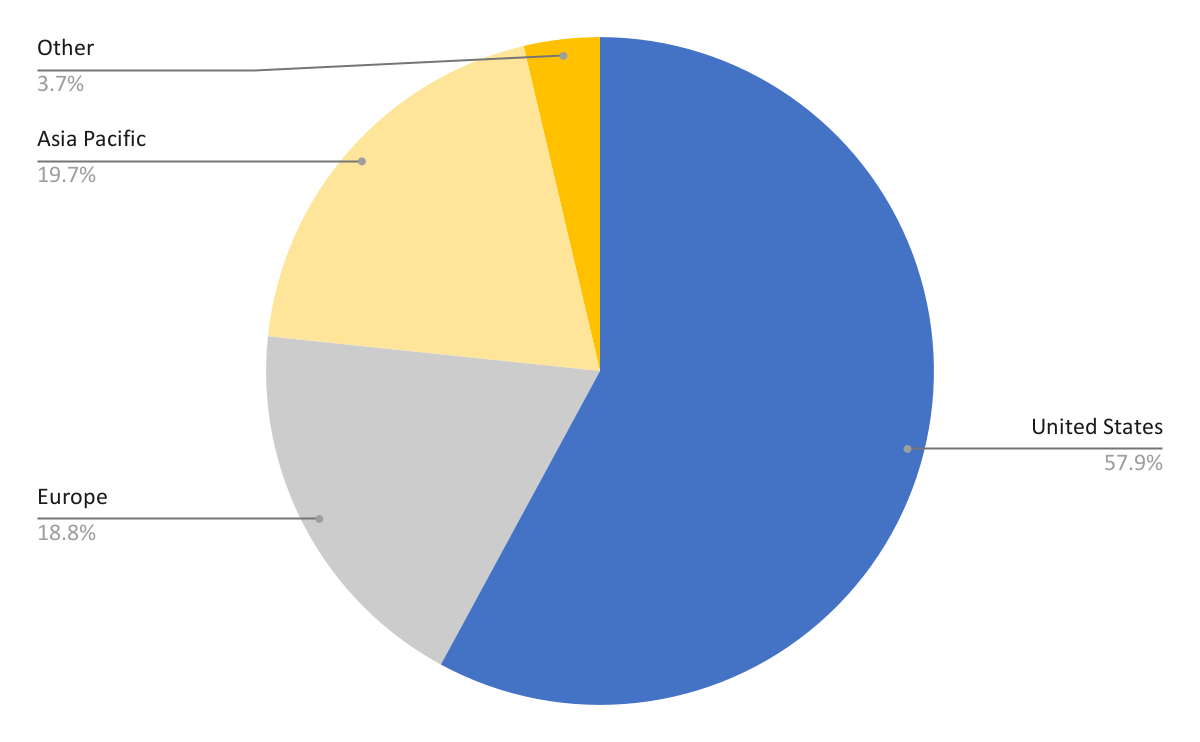

Looking forward, the new SEER2 regulation in the US should benefit the HVAC industry. This new regulation should increase the demand for more efficient products which have 10-15% higher average selling prices. Moreover, the recently passed Inflation Reduction Act is expected to accelerate the demand for energy-efficient heat pumps in the US. However macroeconomic headwinds, high energy prices, and inflation are affecting food and retail customers in Europe. This should result in weak growth for CARR in the European market. The company generated 51% of its revenue from the US market in 2021 which increased to 58% in Q3 22. Meanwhile, the exposure in Europe declined from 28% in FY21 to 19% in Q3 FY22 due to the divestiture of Chubb’s business this year. Given its geographic exposure, I believe the strength in the US market should more than offset the softness in the European market.

Geography-wise revenue in 2021 (Company Data, GS Analytics Research) Geography-wise revenue in Q3 2022 (Company data, GS Analytics research)

In the long run, four secular trends are expected to help CARR’s revenue growth

-

Health and wellness: Shift to healthier air and safer indoor environment.

-

Sustainability: More environmental regulation pushing organizations and individuals to reduce their carbon footprints.

-

Digitalization: Increased interconnectivity of humans and devices (IOT).

-

Growing middle class: ~3 billion people live in areas without access to air conditioning and a similar number of people live in places that don’t have adequate cold chain infrastructure.

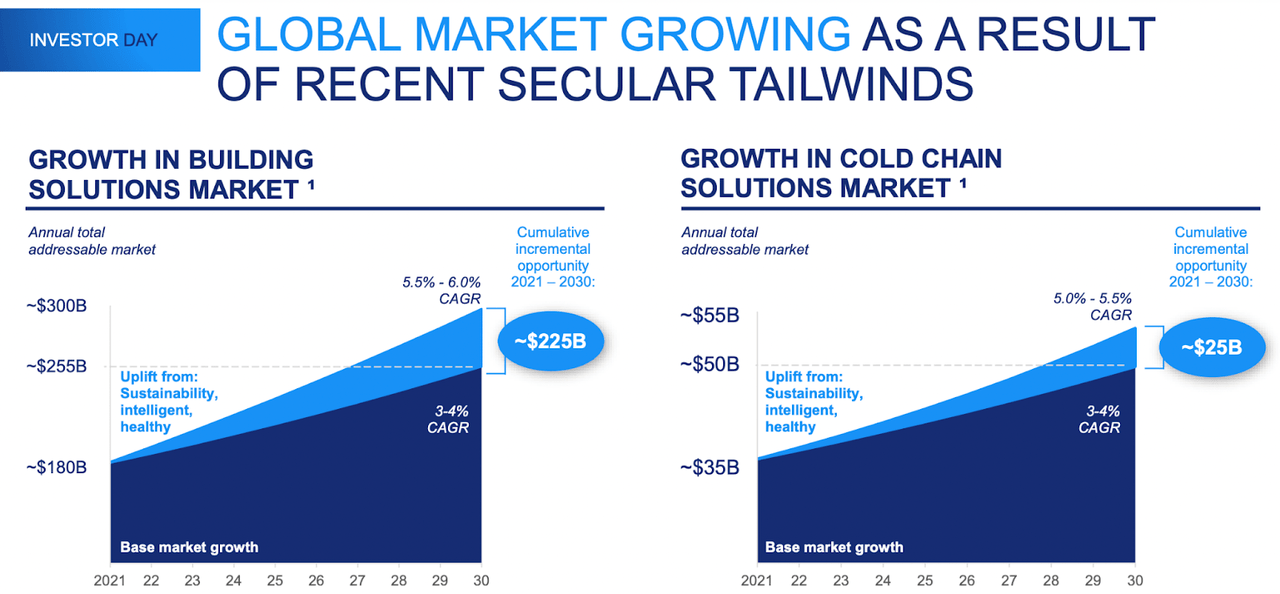

According to management, if we assume base market or GDP growth of 3-4% and then add benefits from the transition toward sustainable, healthy, and intelligent solutions, the company’s Building solution market can grow by 5.5-6% CAGR and the Cold Chain solution market can grow by 5-5.5%.

Total addressable market projection (Investor day presentation)

In addition to the secular drivers mentioned above, the company’s strategic initiatives such as strengthening and growing core, product extension & increasing geographic coverage, and focus on digitally enabled aftermarket growth should further benefit the company.

The company is executing these initiatives quite well. In strengthening and growing the core initiative the company is increasing its R&D expense as a % of revenue. In FY21 the company spent 2.44% of revenue on R&D which was an increase from 2.15% in FY19. These investments in R&D are bearing fruits as evidenced by the introduction of new competitive products such as the Infinity26 air conditioner and Infinity24 heat pump. Under product extension and geographic coverage initiative, the company recently acquired Toshiba Global’s HVAC business. This acquisition should help CARR increase its presence in the fast-growing Asia VRF heat pump market. For digitally-enabled aftermarket growth, the company launched ~100 new aftermarket offerings including BluEdge, Lynx, and Abound. The company almost doubled its new equipment attach rate in the HVAC segment to 40% and expects it to grow to 60%. CARR is expected to continue delivering on these initiatives in the future, which should complement the underlying secular trends helping the company achieve its 6-8% long-term revenue growth target.

Margin Outlook

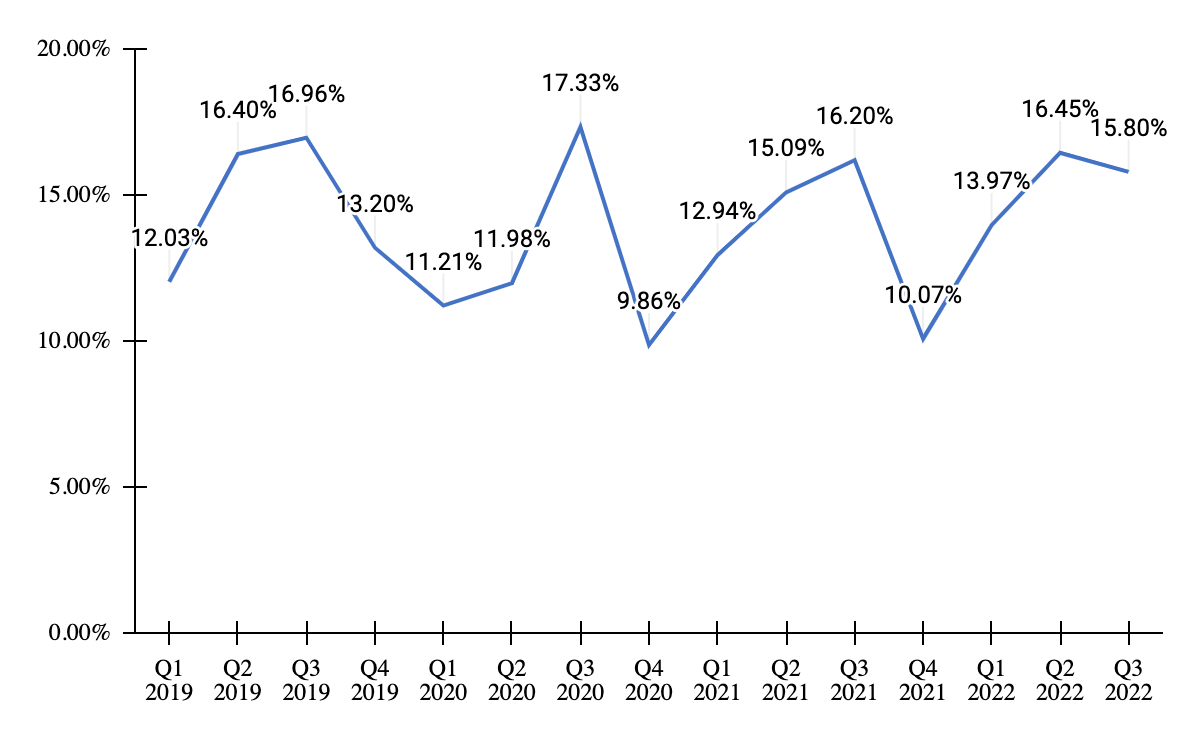

During the third quarter of 2022, the adjusted operating margin was down 40 bps Y/Y to 15.8%. The margin impact of the Chubb divestiture and Toshiba acquisition was about 70 bps Y/Y each offsetting the other. Price/cost resulted in a margin headwind of about 30 bps Y/Y. Adjusted operating margin for the HVAC segment was down 260 bps Y/Y to 16.7% with about 150 basis points impact from Toshiba consolidation and 90 bps headwind from price/cost. The Refrigeration segment margin was up 80 bps Y/Y to 12.8% due to improved productivity and positive price cost. Adjusted operating margin for the fire and safety segment grew 220 bps Y/Y to 16.6% mainly because of the Chubb divestiture and productivity, which more than offset the impact of negative volume.

Adjusted Operating margin (Company data, GS Analytics Research)

On the recent investor day, the management proposed their framework to grow profitability in coming years via cost reduction, delivering a 2-3% gross cost reduction every year.

CARR’s cost-reduction approach revolves around four major cost-cutting areas.

-

Supply chain optimization – A couple of years ago the company launched carrier alliance and dual sourcing to drive down costs. So far the company achieved dual sourcing in 35% of critical components that the company uses. Now the company wants to expand dual sourcing to 75% of their critical components by 2026.

-

Automation – The company is expected to double its automated manufacturing capability by 2026.

-

Footprint optimization- The company plans to continue shifting its operations to low-cost countries. Currently, ~75% of the company’s operations are done in low-cost centers which are expected to increase to ~85% by 2026.

-

Decrease G&A as a % of revenue through the application of carrier business services and co-located centers of excellence. The company expects its G&A as a % of revenue to decrease by 200 basis points by 2026 due to this.

All of these factors combined are expected to yield a margin benefit of almost 50 basis points annually till 2026.

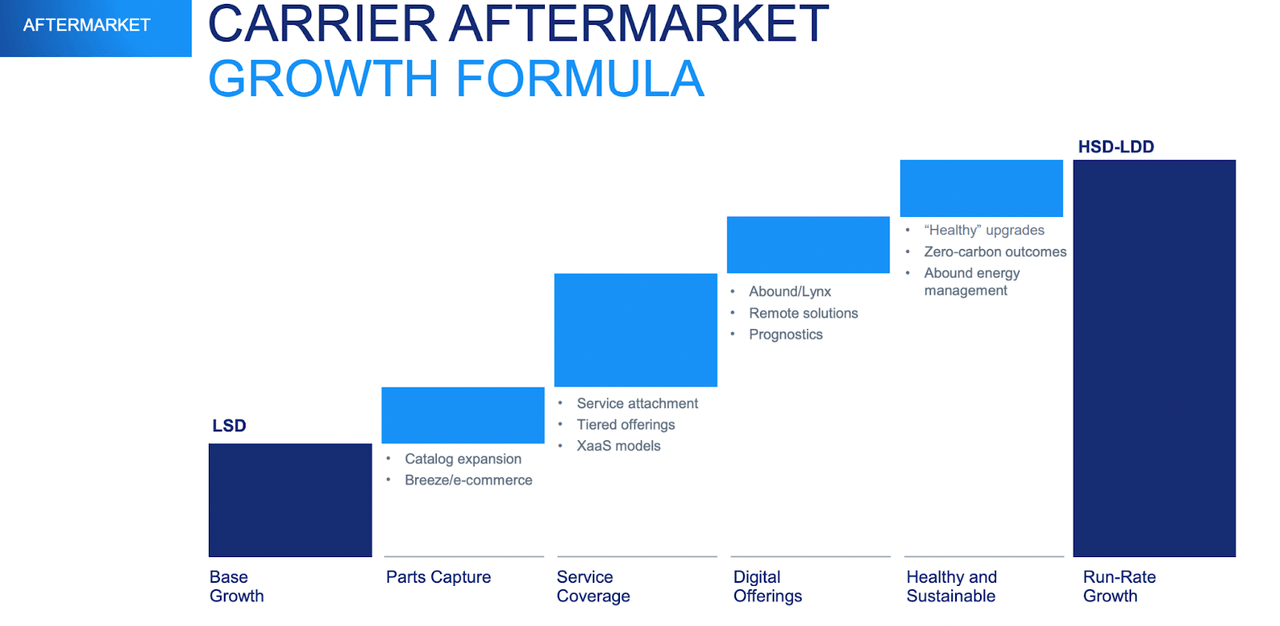

Apart from cost reduction, the management is committed to growing its higher-margin aftermarket segment faster than the overall company. Currently, the company derives 1/4th of its revenue or $4.5 billion from the aftermarket segment which is expected to increase to $7 billion by 2026. Management plans to achieve this $2.5 billion incremental aftermarket revenue by better parts capture, increased service coverage, providing better digital offerings, and capitalizing on the underlying trend towards healthy upgrades and energy efficiency.

For increasing the part capture rate the company is expanding its part catalog and designing differentiated products. For increasing service coverage the company launched a digital service platform known as Bluedge in 2021. Since its launch, the company sold more than 30k service contracts and drove new equipment attach rates above 40% in the HVAC segment. For providing better digital offerings the company launched Abound and Lynx which are digital platforms that send and receive data and interact with key systems of a building (Abound) or cold-chain (Lynx). In the third quarter of 2022, Abound won a deal with a nationwide drugstore chain which will add it to ~2500 stores. Moreover, Lynx is expected to reach 100k subscriptions in FY22. Apart from these initiatives the company’s healthy and sustainable products and solutions should help capture demand for healthy and sustainable upgrades.

Carrier Aftermarket Growth Initiatives (Investor day presentation.)

These initiatives should aid the company in growing its aftermarket segment in the high-single digits to the low-double-digit range in the coming year. Note that the aftermarket segment yields 10 percentage points higher gross margin than the company average. The increasing mix of the aftermarket segment should lead to higher margins for the company in the coming years. Looking forward, both cost-cutting measures and aftermarket segment growth are expected to positively impact CARR’s margins.

Valuation and Conclusions

The stock is currently trading at a P/E of 16.42x FY23 consensus EPS estimate of $2.54, which is lower than its five-year average forward P/E of 20.08x. The company’s near term revenue outlook is favorable with SEER2 implementation in the U.S. expected to drive sales. In the long term, the company’s growth initiative coupled with a shift towards healthy, sustainable, and intelligent solutions should drive sales. Moreover, the company’s cost-cutting measure and mix-shift towards the aftermarket segment should help in improving margins. Hence, I have a buy rating on the stock.

Be the first to comment