Taiyou Nomachi

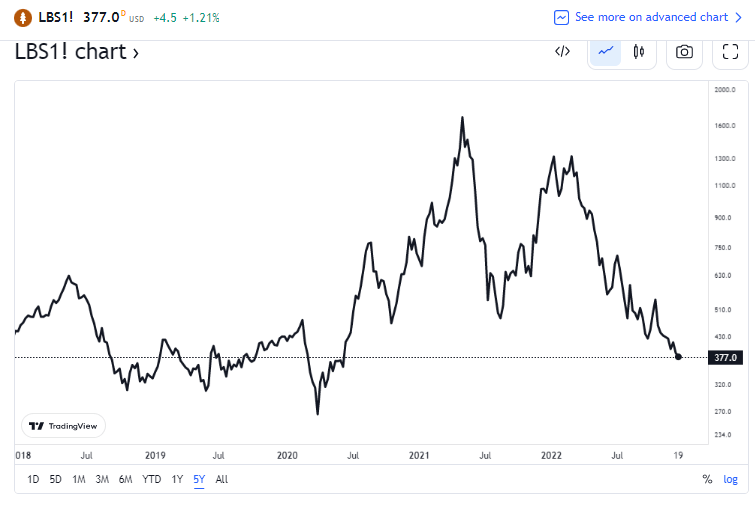

Commodity prices continue to generally retreat as inflation fears transition to recession risks. That is no more apparent than in the lumber market. Prompt-month lumber futures are down more than 75% from their all-time high seen during the worst of the pandemic. As supply chains cleared up and, more recently, demand for real estate has softened, lumber prices have cratered. That impacts many companies owning timberlands.

One of the largest global forestry companies has seen share price volatility in this uncertain environment. Is there more downside ahead for Weyerhaeuser? Let’s cut through the clutter and find out.

Lumber Prices Going Timberrrr

Tradingview.com

According to Bank of America Global Research, Weyerhaeuser (NYSE:WY) is one of the world’s largest integrated forest products companies, with approximately $10.2bn in 2021 sales. WY has returned to its timberland roots by focusing on this segment which sustainably grows and harvests trees. Overall, WY owns or controls approximately 12mn acres, mainly in the United States. WY also has a large wood products business.

The Washington-based $22.9 billion market cap Equity Real Estate Investment Trusts (REITs) industry company within the Real Estate sector trades at a low 10.2 trailing 12-month GAAP price-to-earnings ratio. It pays a 2.3% dividend yield, according to The Wall Street Journal.

Back in October, the company announced an earnings beat as well as a better-than-expected revenue figure. Shares rallied around that report as the market was in a general recovery mode, but recent price action has been less impressive. The firm bearishly preannounced a negative upcoming quarter in late September, so investors should be on the lookout for another potential profit warning before earnings next month.

On valuation, analysts at BofA see earnings falling modestly this year after a massive 2020 and 2021. Per-share profits are then expected to plunge next year with a more modest continued move lower in 2024. The Bloomberg consensus forecast is considerably more upbeat than BofA’s take in the coming quarters, though.

Since it’s a REIT, dividends will be volatile in the years ahead as earnings dip. So do not be fooled by WY’s currently low P/E – that will expand as the “E” falls soon. The EV/EBITDA and free cash flow yield figures also drop. Overall, there are major recession risks with this stock, and the valuation appears to not fully reflect that reality.

Weyerhaeuser: Earnings, Valuation, Dividend Forecasts

BofA Global Research

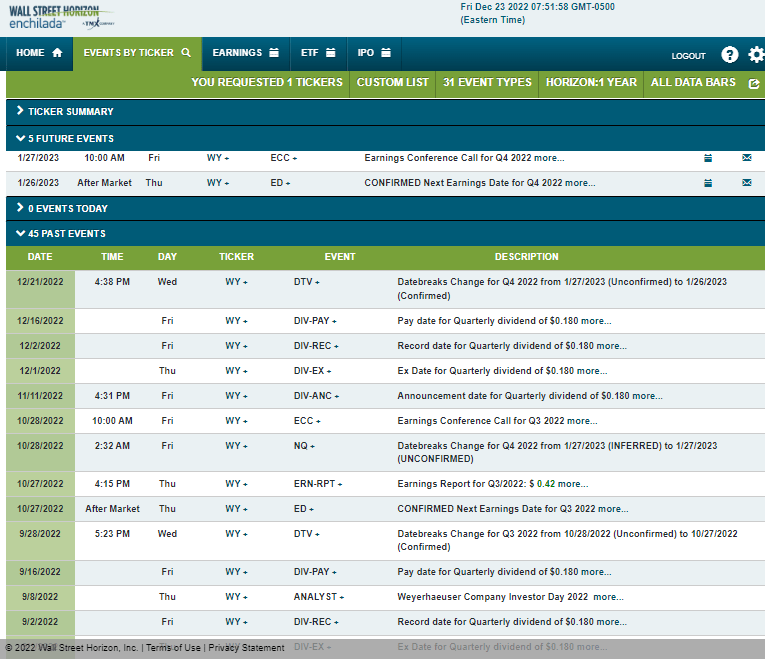

Looking ahead, corporate event data from Wall Street Horizon shows a confirmed Q4 2022 earnings date of Thursday, January 26 with a conference call the next morning. You can listen live here. There are no volatility catalysts until that earnings date though.

Corporate Event Calendar

Wall Street Horizon

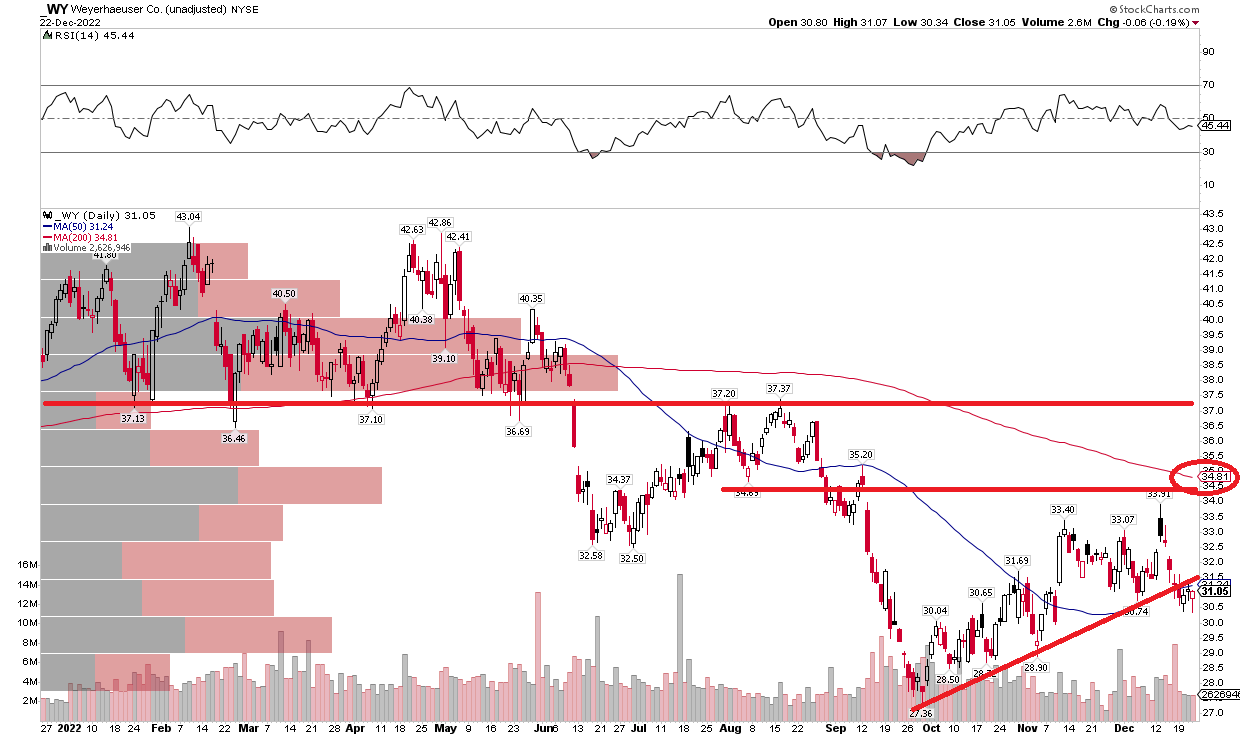

The Technical Take

WY remains stuck in a downtrend after printing a bearish double top pattern earlier this year north of $40. I see resistance in the $36 to $38 range along with a more immediate area of supply near $34. Also, notice the falling 200-day moving average which comes into play near the recent November high. Finally, the stock might be breaking its uptrend support line off the late-September low – another bearish sign.

If we go back on the charts to late 2020, we will find support near $26.50 from a bullish double-bottom pattern during the pullback following the immediate rebound post-March 2020. Shares held that level during a retest back in September. That is an important level to watch to see if the bulls can continue to defend support.

WY: Shares Taking Another Leg Lower

Stockcharts.com

The Bottom Line

I see more bearish risks than upside potential with WY here given the macro-outlook and earnings decline expected. The valuation is not attractive while the price trend appears lower.

Be the first to comment