photosvit

The cruise lines recently took a huge step to remove some of the last remaining covid restrictions holding back guests from taking cruises. Unfortunately, the updated Carnival Corp. (NYSE:CCL) plans were too late for the 2022 summer cruising season and still restrictive on unvaccinated passengers. My investment thesis remains Bullish on a full recovery in 2023, but the cruise lines have to become more aggressive fighting any and all covid restrictions.

Sailing Past Covid

Back on August 12, Carnival loosened health restrictions related to covid vaccinations and specifically testing for cruises departing September 6 or later. Vaccinated guests no longer need a negative test to board a cruise, and unvaccinated guests can now take trips with a negative test within 3 days of embarkation. Some restrictions remain in place depending on the cruise location.

The cruise line had only as recently as July 29 adjusted testing protocols. The biggest move was eliminating the pre-cruise testing for fully vaccinated guests on cruises with itineraries 5 nights or less.

Anyone following covid the last couple of years knows a negative test 3 days prior to boarding a ship doesn’t prevent a passenger from actually having covid at the time of the trip. These covid testing requirements are illogical and go far beyond any requirements to fly or stay in a hotel domestically.

The simplified protocols are clearly in demand, with Carnival doubling bookings on August 15 compared to the equivalent day in 2019. Now, a one-day surge in bookings doesn’t make a trend, or alter the picture in a meaningful way, but it does provide a powerful signal of pent-up demand for loosened restrictions. One should expect Carnival to post some solid bookings for 2023 as guests see a light at the end of the tunnel while bookings within 2022 might remain restricted due to the shifting restrictions and end of the summer cruising season.

Back on the FQ2’22 earnings call, CFO David Bernstein had already highlighted a strong advanced booking position compared to 2019:

For the full year 2023, our cumulative advanced book position continues to be at the higher end of the historical range and at higher prices, with or without FCC, normalize for bundled packages as compared to 2019 sailings. This is a great achievement given pricing on bookings for 2019 sailings is a tough comparison as that was a high watermark for historical yield.

Full Recovery In 2023

The cruise line sold 102.1 million shares of common stock at $9.95 per share back on July 20 raising ~$1 billion in cash. Carnival intends to use the proceeds for general corporate purposes or to address 2023 debt maturities.

The company needing to sell more equity was highly disappointing with the hopes cruise lines would return back to profitable operations in 2022. Not to mention, the offering was priced slightly below $10 while the stock traded above $20 for most of 2021 and on into 2022.

Carnival was cash flow positive during the last quarter due to payments for advanced bookings for 2023. The cruise line generated $1.4 billion in increased advance bookings, but Carnival reported a $900 million EBITDA loss. The company had $375 million in interest expenses cutting off most of the positive cash flows.

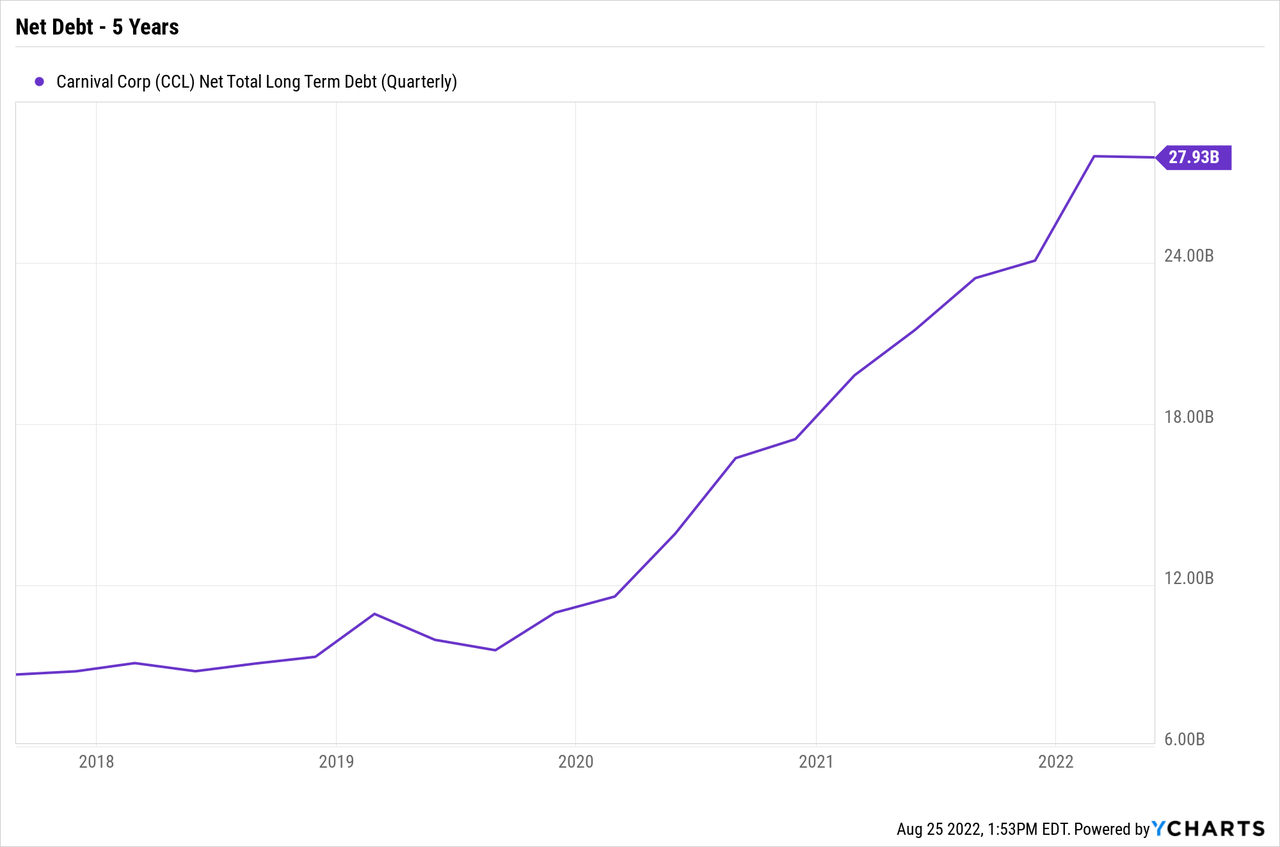

The cruise line saw debt levels soar to $27.9 billion during covid shutdowns, and the hope was the company wouldn’t need to sell more equity with resuming operations. The market cap was only $12 billion with the stock trading below $10 while Carnival ended last quarter with a $7.2 billion cash balance.

The big question is what a full recovery in 2023 looks like with much higher share counts and debt levels combined with higher forecasted capacity. Analysts have Carnival on a path to an EPS of $1.50 to $2.00 in FY24/25 providing a general indication of where the dilution takes a more normalized operation.

Of course, any earnings power isn’t fully realized until Carnival cuts the debt level meaningfully from current levels, with a goal of ultimately reaching pre-covid debt levels with annual interest expenses of $200 million compared to the current level of ~$1.5 billion. Even under a scenario of higher shares outstanding, the cruise line can still generate $1 in additional EPS from cutting interest expenses by $1.3 billion back to pre-covid levels.

The last equity raise boosted the diluted share count to at least 1.24 billion shares, up from just 0.7 billion when entering 2020 before covid hit.

Takeaway

The key investor takeaway is that Carnival has finally removed most of the remaining covid restrictions holding back bookings. Guests should now be able to book summer 2023 trips expecting most, if not all, covid restrictions to be eliminated by next year.

The cruise line was a huge profit machine in 2019 and one should expect the same scenario in FY23 offset by higher interest expenses. As soon as Carnival returns to more normal debt levels, the company will return to the full earnings potential of the cruise line. One can buy the $10 stock with an earnings potential heading back to $3.00, or $1.00 above the $1.50 to $2.00 estimates for the next couple of years.

Be the first to comment