Aliaksandr Litviniuk

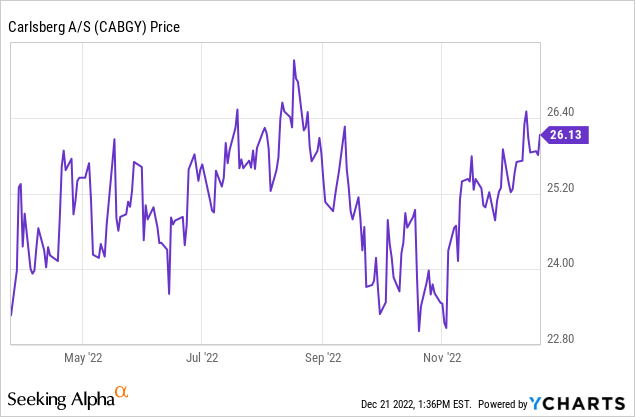

I saw Carlsberg (OTCPK:CABGY) (OTCPK:CABJF) as an opportunistic buy when I last covered it in March. At the time, shares of the Danish brewer had fallen over 30% year-to-date following Russia’s invasion of Ukraine – an unsurprising reaction given its significant operations in the region. What’s more, its all-round Europe-heavy footprint arguably put it in a more vulnerable position in terms of indirect effects of the conflict too.

Up around 17% since then in DKK terms, these shares have staged a solid recovery, albeit they are down around 7-8% from their summer highs.

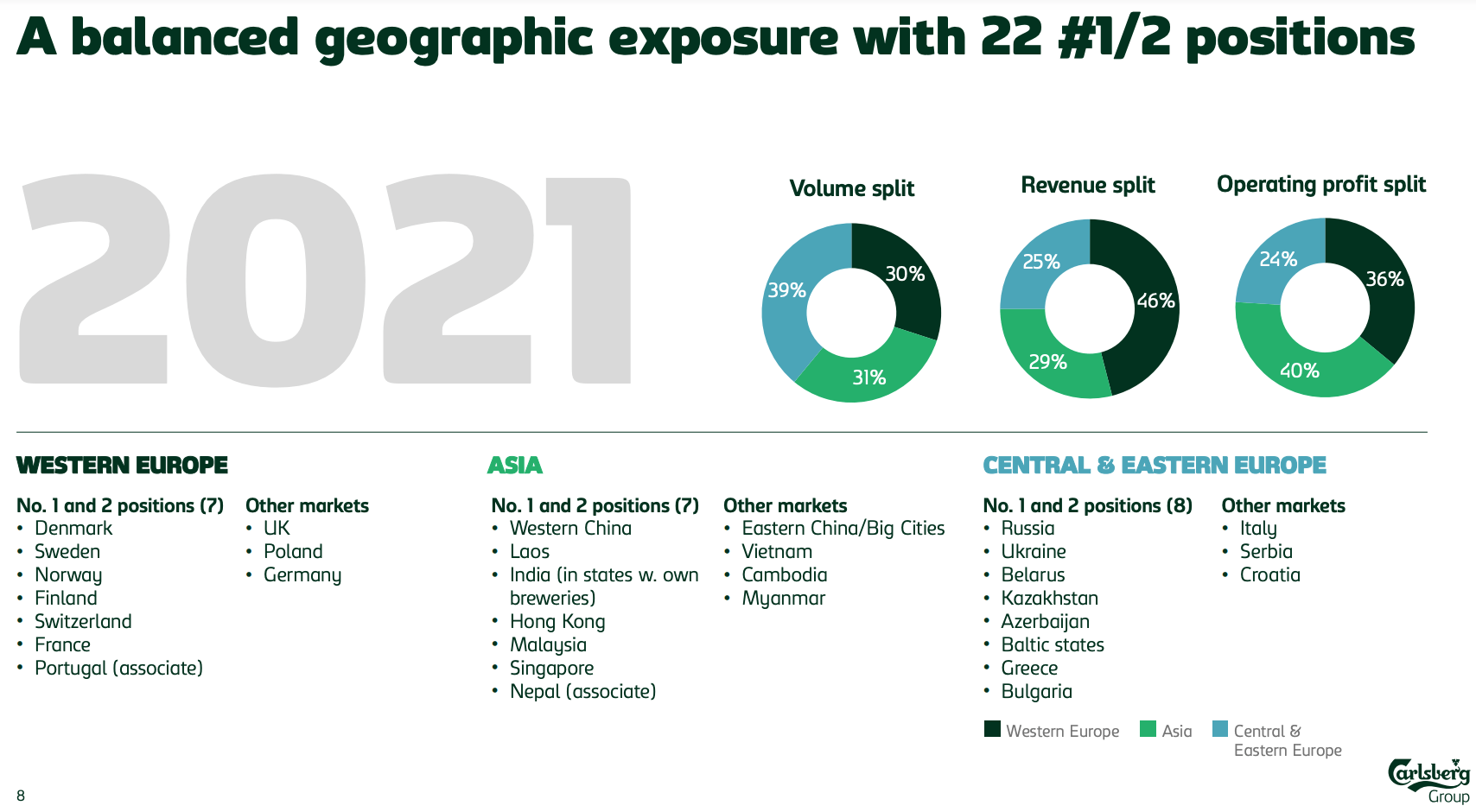

Where that currently leaves the stock is slightly less clear-cut. In the past, I haven’t been thrilled with Carlsberg’s position among the listed global brewers, with the firm under-indexed in growing categories like premium and lacking an attractive emerging market footprint. That puts it at a disadvantage to larger peers Heineken (OTCQX:HEINY) and Anheuser-Busch InBev (NYSE:BUD).

On the flip side, the company has been reporting better numbers this year than I expected, and I also appreciate the clear financial targets accompanying its current five-year growth plan, SAIL’27.

With that, my fair value estimate still points to high single-digit possible upside here, but with the outlook in Europe getting worse that kind of discount looks thinner than it might otherwise. Furthermore, peer AB InBev is trading at a relative discount despite a more attractive growth and profitability profile, and I view the Belgian brewer as the standout industry pick right now. Hold.

Executing Well In Tough Conditions

2022 should have been a relatively straightforward year for Carlsberg, with plenty of low-hanging fruit on offer from lapping COVID-related restrictions in 2021. Russia’s invasion of Ukraine has muddied the waters considerably. In terms of the former, Carlsberg is following many international firms in stepping away from the country entirely. Russia was a relatively big part of the company’s business, accounting for a double-digit share of revenue and high single-digit share of operating profit, and the impairment charge booked in H1 has swung the firm into a paper loss. In terms of the latter, operations in Ukraine have been disrupted for obvious reasons, with the Ukrainian beer market still down ~25% year-on-year in Q3.

Indirect effects are significant, too: COGS inflation for one, with deteriorating European consumer health, in part due to higher energy prices, is another issue. Europe accounts for most of the revenue and operating profit, and consumers there look vulnerable.

Source: Carlsberg Corporate Presentation

Notwithstanding the above, Carlsberg has reported very respectable numbers so far this year. Company-wide organic beverage volume is up 6.4% YTD, with strong pricing leading to a circa 20% increase in revenue. Total volumes are around 8% ahead on pre-COVID 2019. Revenue is 20% ahead on the same basis. In Asia, the firm’s brightest growth avenue, volumes are now almost 20% ahead of their pre-COVID levels. Guidance on full-year organic operating profit growth has been upped to the 10-12% area (previously high single-digits), with better than expected trading helping to offset higher H2 COGS inflation and the roll-off of COVID-hit comps.

The Outlook

Deteriorating consumer health in Europe is my biggest concern in the near-term. Peer Heineken had already flagged softening consumer demand in its Q3 results, and Carlsberg will be in the same boat. So far, reported numbers for the region have been solid, with Western Europe Q3 revenue up 5.7% year-on-year thanks to broadly similar contributions from volume and pricing.

Source: Carlsberg Q3 2022 Trading Statement Presentation

The firm does have price hikes still feeding through from late in the quarter (as well as in Q4), but volume could become more sensitive to pricing in the near term. It is worth noting that the firm flagged a poor September in the U.K., with the country’s on-trade performance a significant drag. This will be a recurring issue in the coming quarters.

With regards to the UK and you’re right, we see there are some difficulties in the markets so to say. The on-trade frequency, the visit frequency has declined significantly over the last couple of months. Kantar has shown in a report that they see the lowest consumer confidence that they’ve ever measured. So that is not good.

Heine Dalsgaard, CFO, Q3 Conference Call

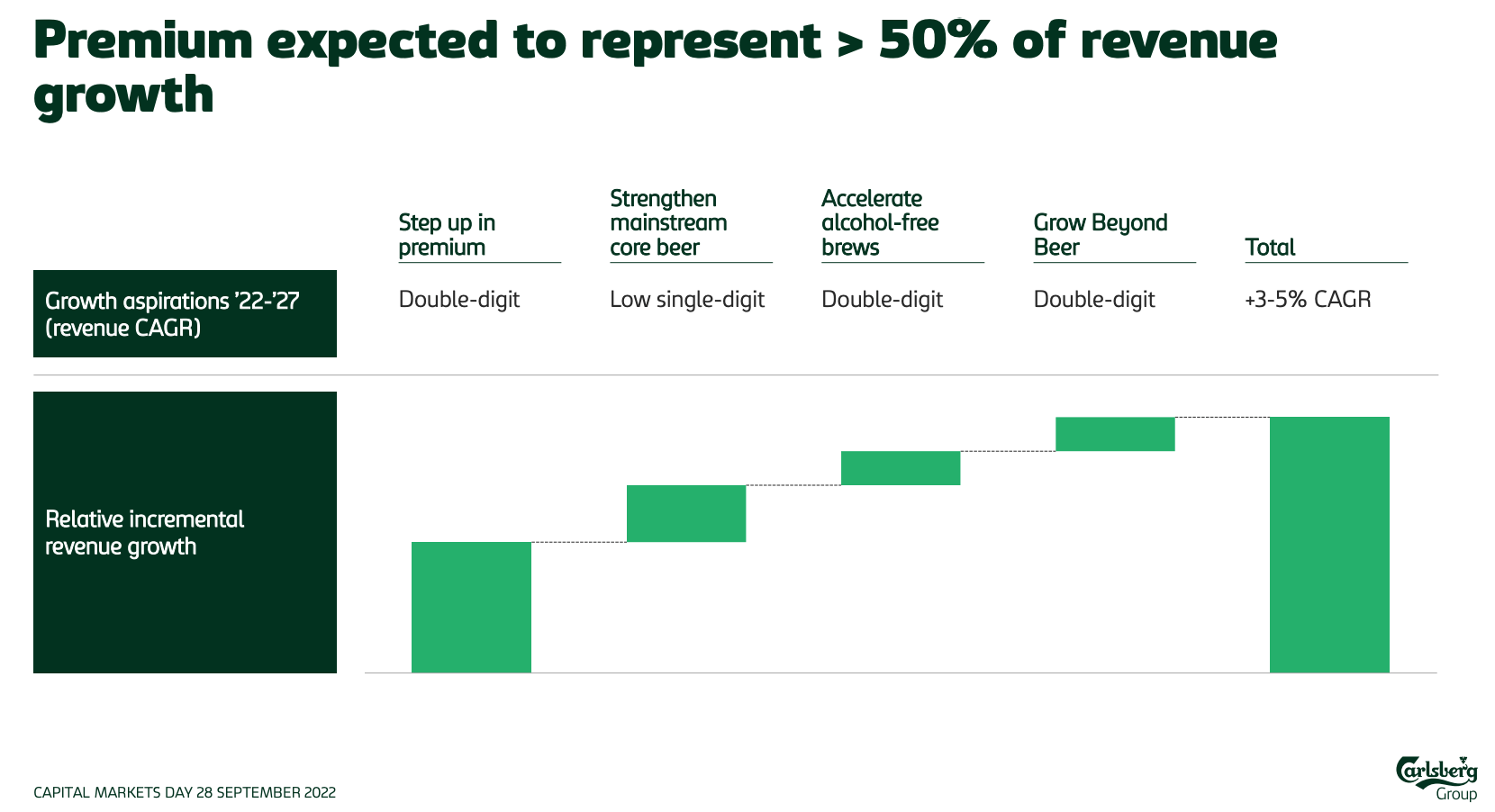

On a longer-term basis, I’ve had my concerns with Carlsberg’s beverage portfolio and geographic footprint. In terms of the former, beverages in the premium-and-above category now account for around 25% of group revenue, though that remains below industry leader AB InBev (~33% revenue share). Given historical and future growth prospects, it’s no surprise that expanding this category forms one pillar of Carlsberg’s SAIL’27 growth strategy.

Source: Carlsberg 2022 Capital Markets Day Presentation

Nevertheless, clear growth targets set out in SAIL’27 are welcome, with those including 3-5% annualized organic sales growth and slightly higher organic operating profit growth.

Source: Carlsberg 2022 Capital Markets Day Presentation

Some Upside Left, But Better Value Elsewhere

Carlsberg shares change hands for around DKK918 in Copenhagen trading at the time of writing, up from circa DKK780 when I covered them with a ‘buy’ rating in March. That still leaves a bit of upside to my DCF-derived fair value estimate of DKK965 per share, with that figure based on a 5-6% mid-term CAGR (i.e. broadly in line with SAIL’27 targets) moderating thereafter to a low single-digit per annum terminal rate.

While that may leave the shares a little undervalued for long-term investors, given the elevated uncertainty facing European consumers it’s probably not enough to warrant much excitement. What’s more, industry leader AB InBev appears to trade at a material discount. Headline valuations for the two appear similar (both trade on a prospective FY22 EV/EBITDA of ~9x), but with AB InBev sporting a clear lead on profitability and long-term growth prospects, I don’t see a compelling enough reason to look beyond the industry leader right now. Hold.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment