dikushin

This article was co-produced with Mark Roussin.

While writing this article, I looked up “the most unexpected pairings” online.

Incidentally, you have to love the modern era for its instant gratification when it comes to the most random searches. How else would I have come up with 1.26 million possible answers to my question in a nanosecond?

The very first entry was titled “10 Unexpected Pairings That Make Life More Exciting.” It’s an awesome title that works perfectly for my purposes.

However, I have to say I just can’t get enthusiastic about pairing florals and stripes together. So I’m going to reference the second hit instead: “Unexpected Duos: From Food to Fashion, the Crazy Pairings America Loves.”

Published by Fort Worth Business Press, it reads:

“Sometimes unexpected pairings just make sense. Whether it’s an unusual food duo that ends up incredibly delicious, a quirky blend of fashion that works surprisingly well, or an opposites-attract couple that actually balance each other out perfectly, these unexpected pairings can make a lasting impression.

Consider:

- Breakfast for dinner

- Sour cream and onion (“The potato chip champion”)

- Cartoon characters Tom and Jerry

- Muppet characters Miss Peggy and Kermit

- Fairytale characters Beauty and the Beast.

As a man who enjoys his oatmeal… who consumes a potato chip every now and again… has been a kid himself and has five children of his own…

I consider that a pretty decent list. Though it does seem to be missing a pretty big entry, especially considering being published in a business-specific publication.

Dividend Growth Is Still Growth

Growth and real estate investment trusts (REITs).

They might sound like peanut butter and tomatoes. Certainly, they’re not often associated with one another when there are “real” growth stocks like big tech has been the last 10 years or so.

But should they be?

I don’t think you’re ever going to find a REIT that can compete with, say, Tesla, Inc.’s (TSLA) best years. (Then again, REITs don’t typically tank as much either during not-great years.) But there are, in fact, REIT growth stocks out there.

Depending on considerations such as sector, time, location, and management, their shares can appreciate rapidly. Or at least much more rapidly than the typical slow-and-steady pace we tend to see.

But beyond those admitted outliers, is dividend growth.

Don’t groan just yet. I’m not trying to be cute. This is an aspect and angle worth exploring.

For starters, REITs tend to pay higher dividends than non-REITs. That makes sense since they’re required to distribute at least 90% of their taxable income to shareholders via dividends.

That’s a very nice perk in and of itself. But then there’s the fact that their investors have expectations based on their tax status.

By that, I mean they want to see those dividends grow, preferably year in and year out. And being the competitive entities that (most of them) at least want to be…

The results can be impressive.

Now, don’t get me wrong. Some of them are slow and steady even in that regard – which isn’t always a bad thing, mind you. A few are stagnant, and sometimes we see dividend cuts.

That’s why we’re always mindful of each potential pick’s stats: What their funds from operation (“FFO”) and/or adjusted FFO (“AFFO”) look like. The health and safety of their payout ratios. Their past records, current deals, and future prospects.

Dividend growth in and of itself should never be the end-all and be-all of your investment decisions. But when everything aligns? We want to be part of that real estate picture.

As such, let’s discuss three dividend growth REITs that iREIT on Alpha is excited about in 2023.

Dividend Growth REIT #1 – American Tower Corporation (AMT)

American Tower is the premiere Cell Tower REIT in the industry, with a market cap of $98 billion, nearly double that of its closest competitor, which is Crown Castle (CCI).

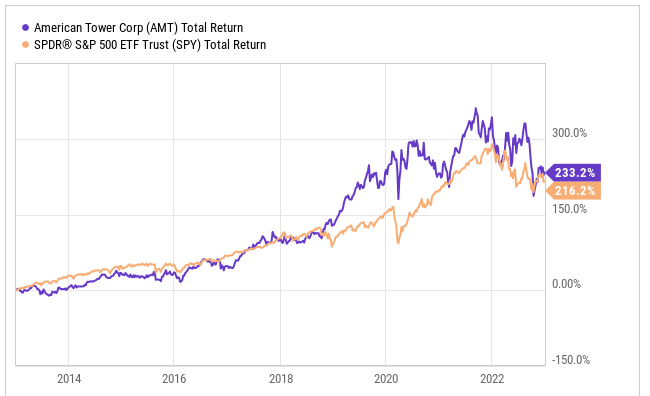

Over the past decade, AMT shares have outperformed that of the S&P 500 (SP500) from a total return perspective. During that period, AMT had a total return of 233.2% compared to the S&P 500 having a total return of 216%.

YCharts

Over the past year, however, shares of AMT have underperformed the greater stock market by falling 25% compared to the S&P 500 falling 20%.

This has created what appears to be a great opportunity in this blue-chip REIT.

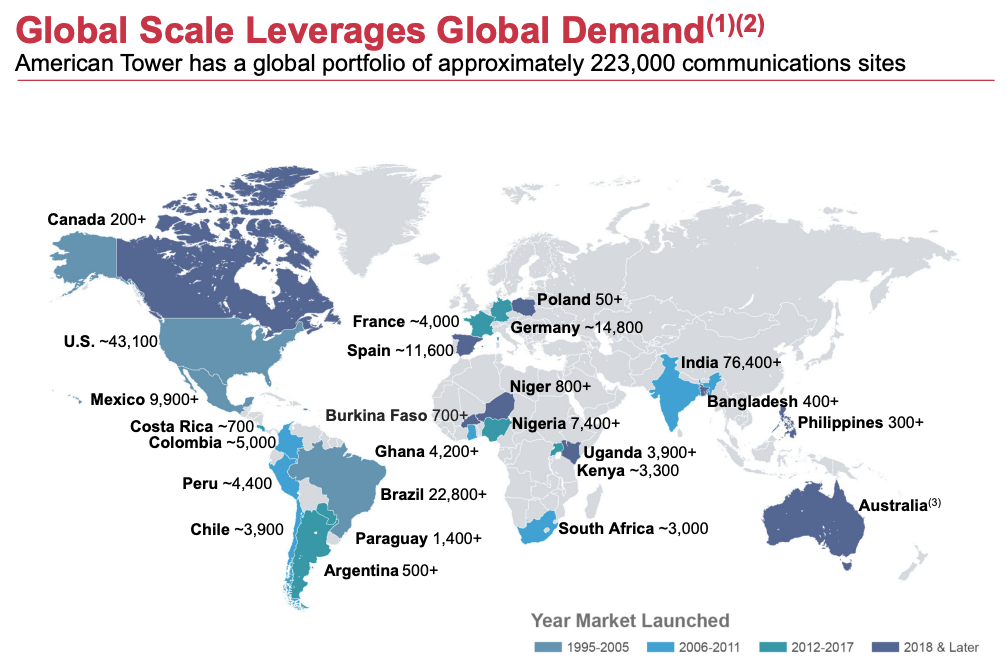

The company has a portfolio that consists of ~223,000 communication sites across the globe.

AMT Investor Relations

The growth in 5G, both here and internationally, has been and continues to be a growth driver for the company. 5G speeds are far superior to that of 4G, but the problem with 5G is the lack of distance the data can travel. This, however, is a great thing for American Tower because it creates a need for more cell towers.

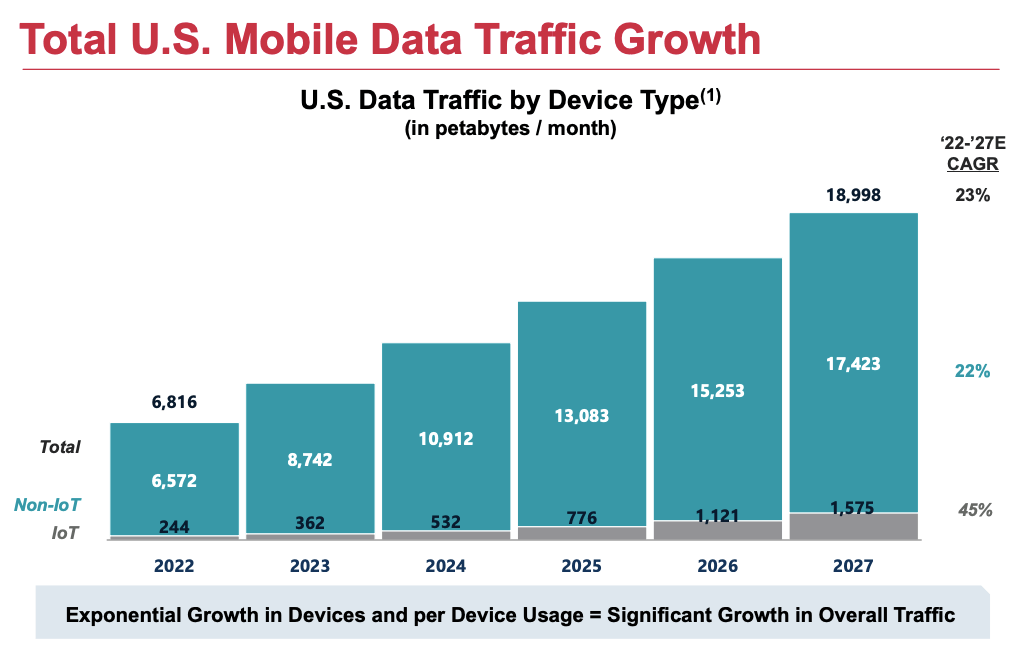

The growth in mobile devices may have slowed slightly, but the usage and dependency for data has only continued to grow. Over the next handful of years, including 2022, U.S. mobile data traffic is expected to grow at a combined annual growth rate of 23%.

AMT Investor Relations

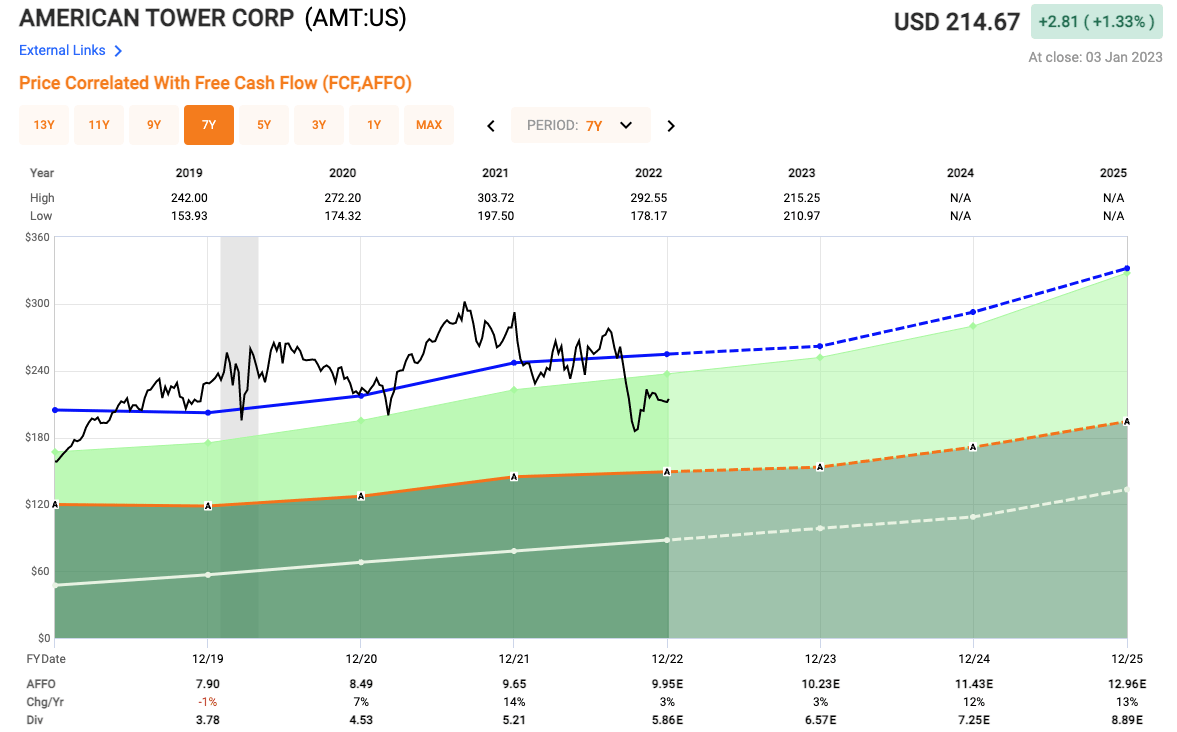

Free cash flow has been growing at an annual clip of 16% over the past five years, and I do not foresee any reason for that to slowdown in the near-term. Higher sustainable cash flows feed into the company’s growing dividend.

AMT currently pays an annual dividend of $6.24, which equates to a dividend yield of 2.9%. The dividend is well-covered with a low payout ratio of 54%, providing plenty of room for continued dividend growth. Over the past five years, the company has increased their dividend at an average annual rate of 18%, making them a dividend growth REIT.

In the YCharts chart above, we saw how American Tower shares have fallen over the course of the past year, which has created a buying opportunity in a blue-chip REIT that was trading at a premium valuation 12 months ago.

At the start of 2022, shares of AMT were trading at an AFFO multiple over 30x. Today, you can pick up shares of AMT for 21x, which is well below the company’s historical average of 25.6x.

FAST Graphs

Dividend Growth Stock #2 – Prologis, Inc. (PLD)

The next dividend growth REIT on our list is another leader in their respective space, which is Prologis. Prologis is a leading REIT within the logistics industry.

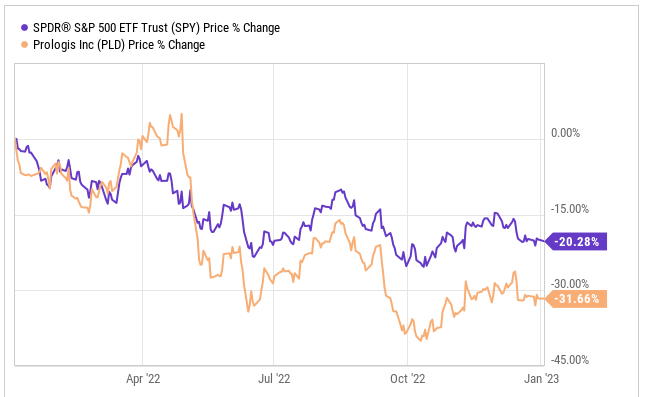

Over the past year, shares of PLD have fallen over 30%, also underperforming the S&P 500 in 2022. The company currently has a market cap of $105 billion.

YCharts

PLD had a rough year for a few reasons in 2022:

- Amazon made some comments in their quarterly earnings release that brought into question the amount of warehouse space the company had leased out

- Prologis acquired Duke Realty at a valuation that shareholders did not agree with

- Valuation was running really hot coming into 2022.

Let’s briefly go through each of these issues. First, the Amazon comment sent shockwaves through the logistics space in general, so it was not just PLD related. After all, AMZN is the company’s largest client, so there was obvious concern from a shareholder perspective. However, Amazon is not looking to reduce its warehouse space necessarily, and instead, they want to upgrade. Upgrade in terms of location as well as technological advancements within the buildings.

To date, Amazon has not terminated or adjusted any of their leases with Prologis. Instead, the company actually added new leases in the most recent quarter.

Next, let’s talk about the company’s acquisition of Duke Realty, which was another warehouse REIT. Prologis acquired Duke Realty for a value of $23 billion. The acquisition included 19 new buildings within major U.S. markets, including Southern California, New Jersey, South Florida, Chicago, Dallas and Atlanta.

The acquisition was announced at the same time investors were dealing with the Amazon news, so it was a double whammy. The markets in general were already beginning their downward spiral, and then investors got word of PLD making an acquisition. Investors were frustrated more at the timing than anything.

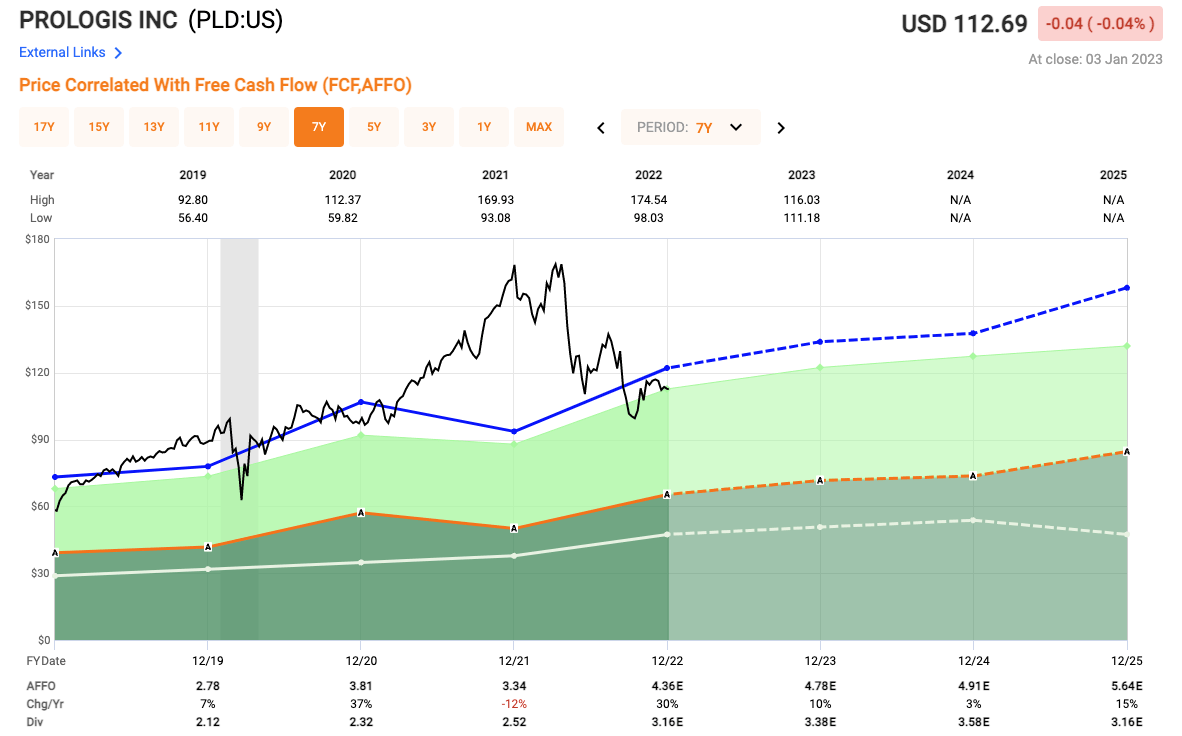

Finally, PLD shares came into 2022 on fire. Shares were trading at an absurd valuation, over 45x P/AFFO. For comparative purposes, PLD shares have historically traded at an average of 28x.

FAST Graphs

Today, investors can pick up shares of PLD for 25x AFFO and 23.5x next year’s AFFO estimates. This is very reasonable for a company of PLD’s stature.

The logistics REIT pays an annual dividend of $3.16/share which is well-covered by a low payout ratio of 61%. PLD has increased their dividend for 9 consecutive years now and they have a 5-year dividend growth rate of 12.4%, making them a dividend growth REIT.

Dividend Growth REIT #3 – VICI Properties Inc. (VICI)

The first two REITs we covered today were not only dividend growth REITs, but they were both leaders within their respective sector. Well, we certainly cannot buck the trend now.

As such, we will continue with the premier REIT within the hospitality and gaming industry, which is VICI Properties. VICI has a market cap of $32 billion.

On the year, shares of VICI outpaced much of the REIT sector and the S&P 500, by gaining 6% over the past 12 months.

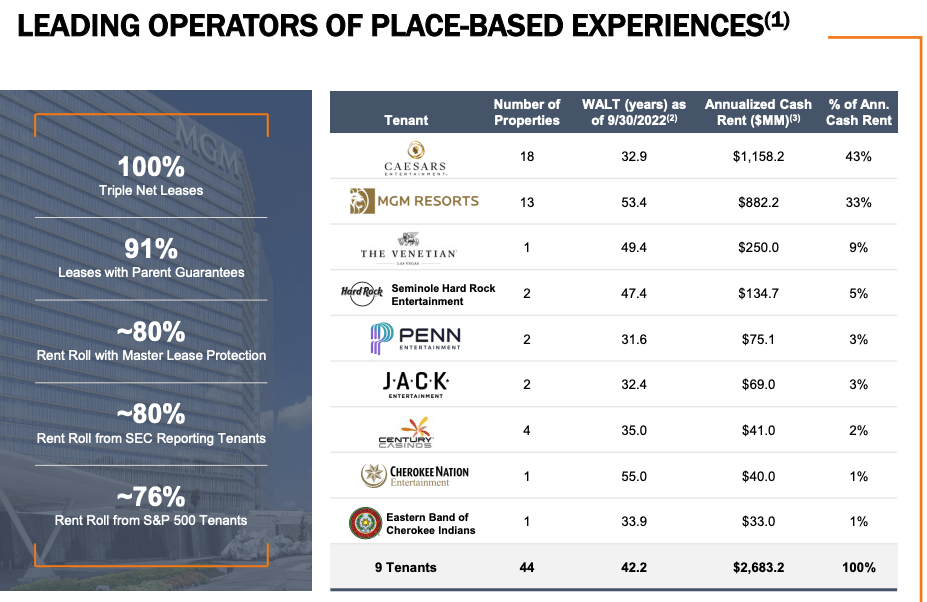

VICI owns 44 properties within the United States, but a large chunk of their annual base rent comes from Las Vegas. VICI is now the largest landlord on the Las Vegas strip and the company earns ~45% of their annual rent from this region alone.

The prized portfolio of properties VICI owns along the strip include:

- Caesars Palace

- MGM Grand

- The Venetian

- New York New York

- Mandalay Bay

- Luxor

- Excalibur.

Being a REIT, the company is really just a landlord, yet they work with some of the top hospitality and casino operators around. This is evidenced by the company’s ability to maintain a 100% occupancy rate and collection rate, even during the depths of the global pandemic.

The gaming and hospitality sector, especially along the prime real estate of the Las Vegas strip, has a very high barrier of entry. One reason being the lack of land on or even around the Las Vegas strip.

Along with operating in a sector in which they are not only a leader but also have a high barrier of entry, VICI also enters into very long master lease agreements with its operators. These long dated leases currently have a weighted average lease term of 42.2 years.

VICI Properties

The gaming space is becoming more popular, and other REITs are trying to find their way into the sector. Recently, even Realty Income Corporation (O) acquired their way into the gaming sector with their $1.7 billion transaction with Wynn Resorts.

The strong performance from VICI combined with a strong balance sheet bodes well for both the company and shareholders moving forward. We just went through a global pandemic which saw much of the country shut down for a period of time, and VICI did not blink. Now we are headed for a recession here in the U.S., yet the REIT is still expecting to grow.

Analysts over at Jeffries believe this as well, as they made VICI their “top pick” for 2023.

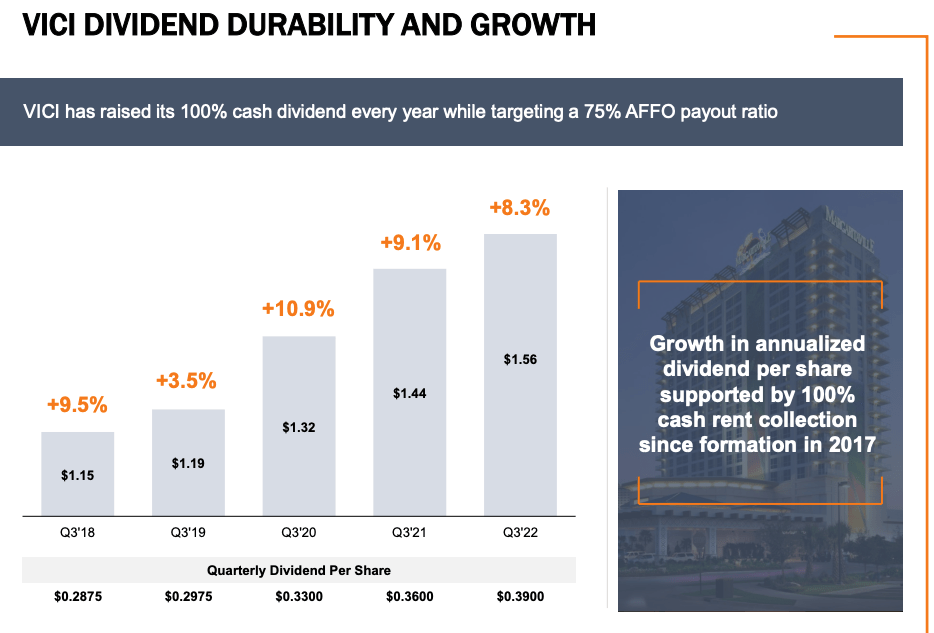

The continued solid performance of the company, in their short stint as a public REIT, has not only fueled further growth and expansion, but it has also fueled a growing dividend.

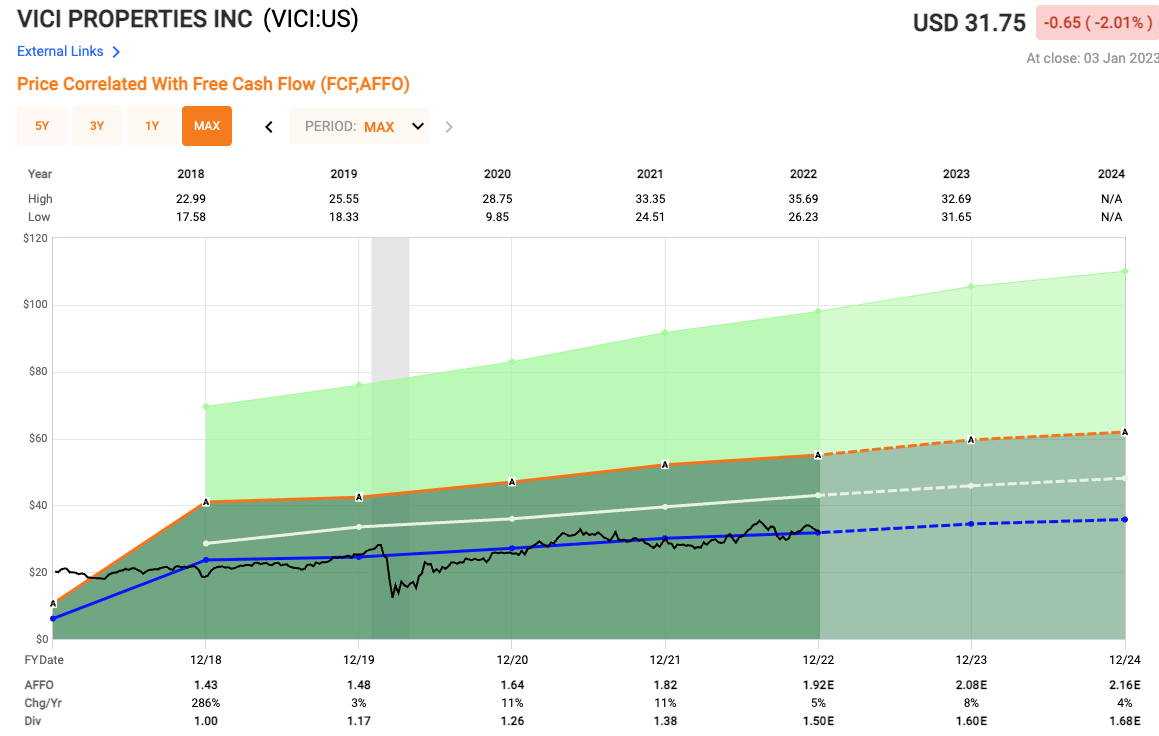

As you can see below, VICI has more than doubled their initial quarterly dividend back in 2018, as they have been increasing the dividend every year since going public. Over the past three years, VICI has had an average dividend growth rate of 11.5%, making them a dividend growth REIT.

VICI Properties

In terms of valuation, as I mentioned VICI is new(er) to the public markets, so investors are still calculating what type of multiple to place on a company like VICI, but that is where the opportunity lies.

Analysts are looking for AFFO of $2.08 in 2023, which indicates AFFO growth of 8%. This implies a forward AFFO multiple of 15.2x. Since going public, shares have averaged an AFFO multiple of 16.5x.

FAST Graphs

In Conclusion…

So what do you think? Was I being cheesy or cutesy with the comparison?

In all honesty, I do recognize that the answer might very well be yes, no matter how I meant it. And even if I didn’t come across that way, I know some of you are going to take objection regardless.

It comes with the territory. Plus, your feedback does help me stay sharp. I often think about potential responses as I’m writing these articles.

All the same, I maintain that one of the best kinds of growth you can hope to find in the stock market is dividend growth. And if it’s on the higher side AND sustainable, packaged up in a share price that’s at or under value?

I’m going to write about it. I might even invest in it depending on my portfolio needs at the time.

As always, take your own personal situation into consideration as well when deciding whether to get involved or not. But looking at the REITs above objectively in the grand scheme of things…

There’s a whole lot to love that I’m more than happy to pass along to you.

Be the first to comment