z1b

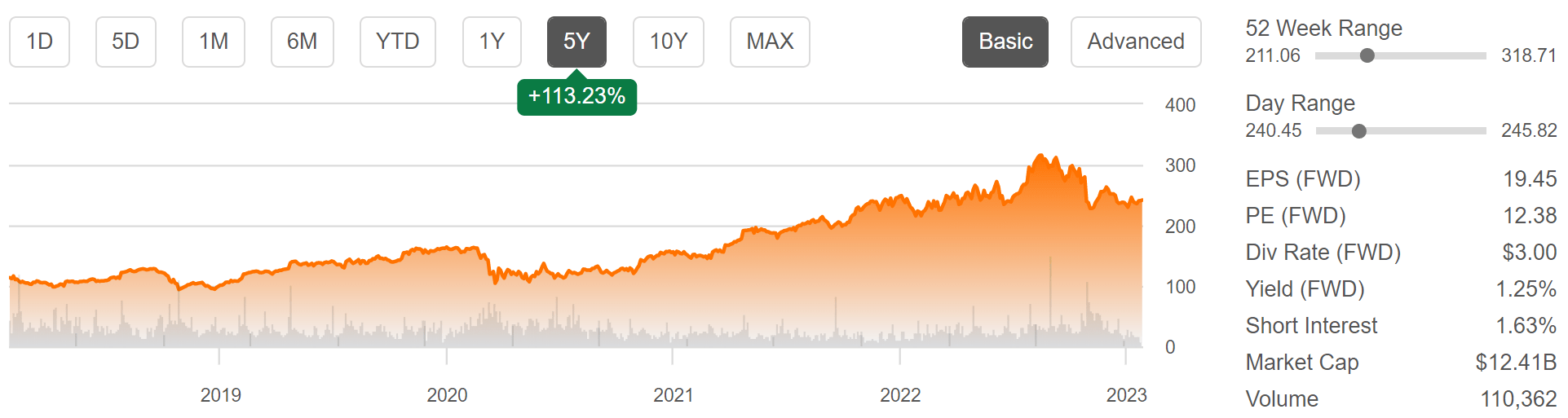

Sometimes one chart can say it all. In the case of Carlisle Companies (NYSE:CSL), the stock has seen strong upward momentum over the past 5 years, more than doubling its value over this timeframe. It’s also one of my best picks over the past couple of years, as the stock has given investors a 61% total return since early 2021, far exceeding the 6% return of the S&P 500 (SPY) over the same timeframe.

CSL Stock (Seeking Alpha)

That’s not bad for a supposed “old economy” stock that’s not as popular as the once high flying tech names. In recent months, CSL has traded materially down from its 52-week high of $319, and in this article, I highlight what makes now a good opportunity to layer into the stock while it’s undervalued.

Why CSL?

Carlisle Companies is a diversified global company that manufactures highly engineered products and solutions for its customers. Its key markets include commercial roofing, architectural metal, specialty polyurethane, aerospace, medical technologies, defense, transportation, and industrial, to name a few.

CSL’s industry diversification which allows it to spread its risk across different end-markets and mitigate the impact of fluctuations in any particular market. Additionally, the diversification of the company’s operations allows it to capitalize on growth opportunities across multiple segments.

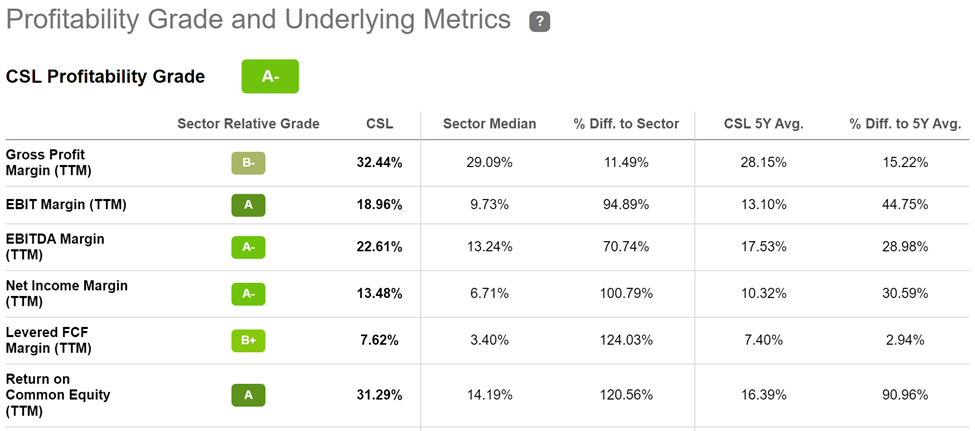

Carlisle also has a strong track record of innovation through investments in R&D, which has helped it to develop a wide range of new products and solutions to meet the changing needs of its customers. This enables CSL to charge above market pricing for its premium quality products, resulting in higher than average profitability. As shown below, CSL scores an A- Profitability grade, EBITDA and Net Income margins of 23% and 13.5%, which are well in excess of the sector median.

CSL Profitability (Seeking Alpha)

Meanwhile, CSL has demonstrated strong operating fundamentals despite plenty of macroeconomic uncertainty brought upon by high interest rates and war in Ukraine. This is reflected by revenue growing by 36% YoY (28% on organic basis) to $1.8 billion. This was driven by positive pricing action across the board, robust U.S. non-residential construction demand and continued recovery in CSL’s aerospace markets.

Notably, CSL now has a record backlog in aerospace due to the aircraft shortage, which has forced many airlines to cut back on flights as they struggled to meet the rebound in passenger demand. These strengths more than offset weakness in the U.S. residential market, and helps to justify CSL’s diversified business model.

The market, however, appears to be spooked, as it anticipates potential for volatility in CSL’s fourth quarter results continued uncertainty in this new year, and management recognizes that consumers and businesses are being more cautious in the current climate.

Nonetheless, I see the long-term growth thesis as being intact, as CSL continues to execute towards is Vision 2025 strategy of driving growth and efficiencies. This was highlighted by management during the last conference call:

The pillars of Vision 2025 remain core to our strategy going forward. These include: first, drive mid single-digit organic growth. Second, utilize the Carlisle Operating System or COS to drive leverage. We use COS to consistently drive efficiencies and enhance operating leverage by targeting cost savings of 1% to 2% of sales annually. In the third quarter, adjusted EBITDA grew 75% nicely leveraging our sales growth.

Third, build scale with synergistic accretive acquisitions. Under Vision 2025, we have streamlined and optimized our portfolio through acquisitions and divestitures to build scale in our highest returning building products businesses. CWT leadership continues to execute extremely well on delivering a smooth and efficient integration of Henry and is on pace to exceed our initial synergy targets of $30 million.

Plus, CSL maintains a strong BBB rated balance sheet. It also has 46 years of consecutive dividend increases under its belt, and that includes the 39% dividend increase during the fourth quarter. While the 1.2% dividend yield isn’t anything to write home about, it is very well covered by a 12% payout ratio, and future raises should make up for the low starting yield, especially for those who don’t need immediate income.

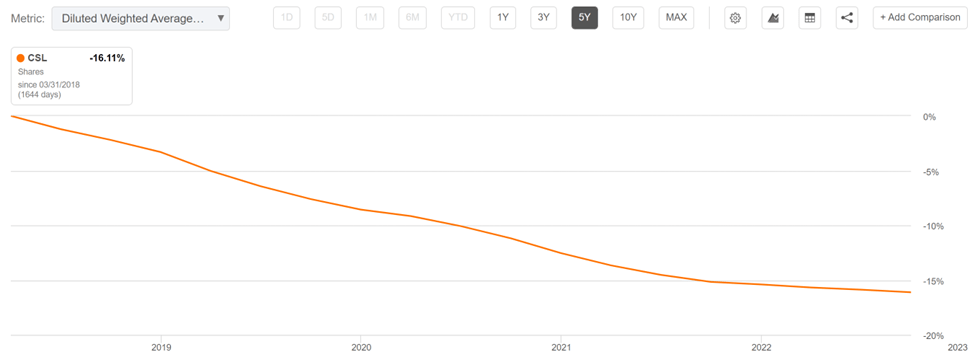

Importantly, CSL is a company that prioritizes total returns with share buybacks as an alternative form of capital return to shareholders. This includes $26 million spent on share buybacks during the last reported quarter and as shown below, CSL has reduced its share count by an impressive 16% over the past 5 years.

CSL Shares Outstanding (Seeking Alpha)

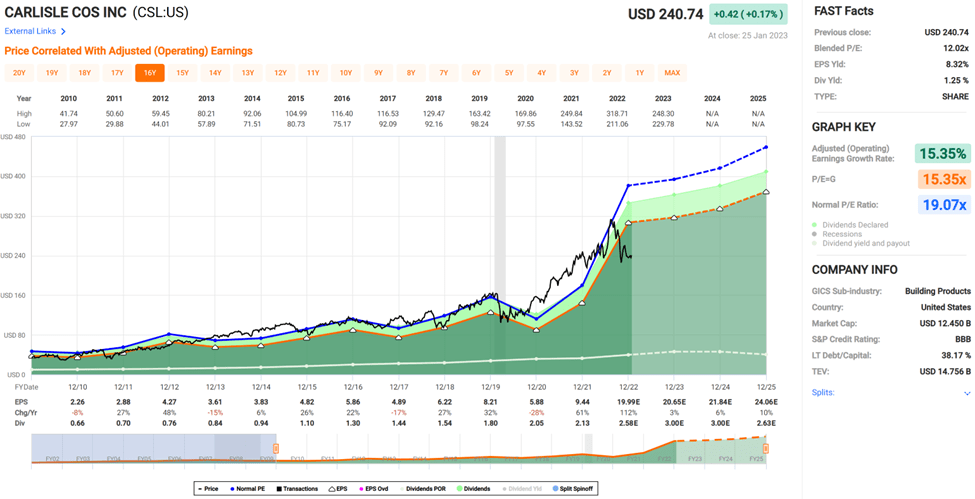

Turning to valuation, CSL appears to be bargain priced at $242 with a forward PE of 12.4, sitting far below its long-term normal PE of 19.1, as shown below.

CSL Valuation (FAST Graphs)

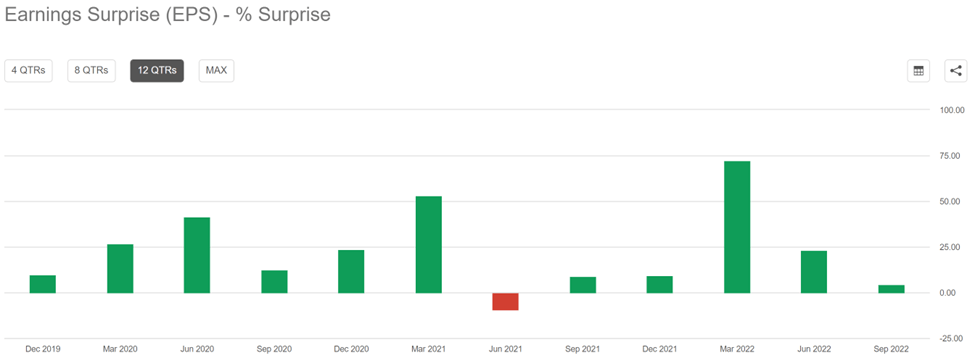

This valuation apparently reflects the mid-single digit EPS growth that analysts expect this year. However, CSL has a strong history of beating analyst estimates, as shown below. Plus, even with lower expectations for growth this year, analysts also see value in the long-term thesis, and have a consensus Buy rating with an average price target of $343, translating into potentially very strong total returns.

CSL Earnings Surprises (Seeking Alpha)

Investor Takeaway

Overall, CSL appears to be a great value buy at current levels. It has a broad portfolio of innovative products that command premium pricing and it’s executing towards its Vision 2025 initiative. Plus, CSL recently bumped up its dividend by a material amount and has a robust track record of share buybacks. The market appears to have more than priced in near-term headwinds, presenting value investors with an excellent opportunity to layer into the stock.

Be the first to comment