Solskin

Investment Summary

Our buy call on CareMax, Inc. (NASDAQ:CMAX) has not been profitable and therefore are here today to revise the position down to neutral. Unfortunately, despite the growth percentages exhibited in its latest quarter, the market has reacted poorly and was likely seeking more from the name. Even though management updated guidance, recent developments in the company’s growth engine haven’t materialized to upside in the share price. This presents as a risk to holding CMAX looking down the line, especially with so many other selective opportunities available.

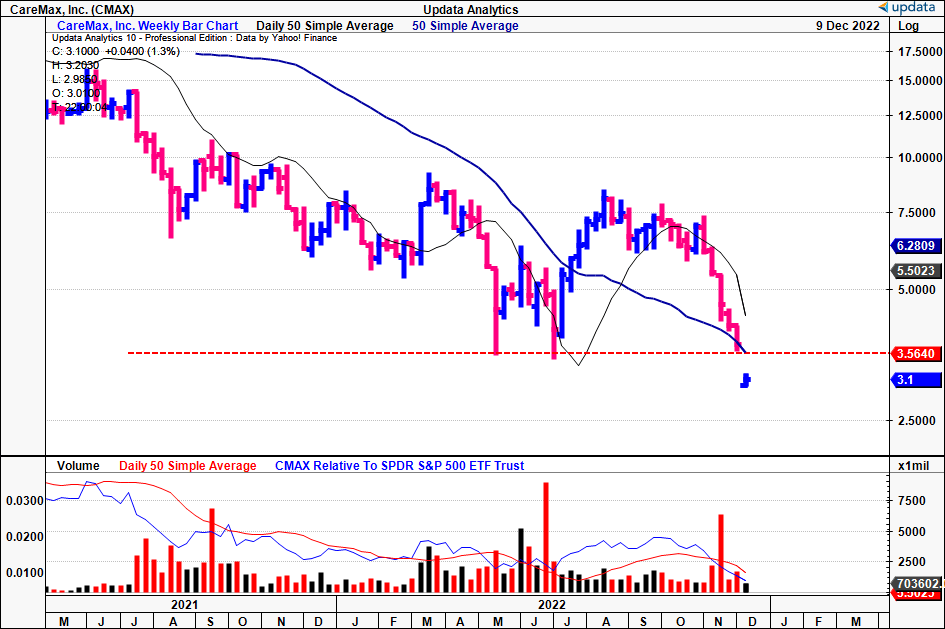

You can see below that the stock has lost support and has broken long-term resistance levels in the chart below.

Exhibit 1. CMAX 2-year weekly price action

Data: Updata

As a reminder, our buy thesis on CMAX was built on the below factors [you can read it by clicking here]:

- In July 2021, MAX announced that it had signed a definitive agreement to acquire the Medicare value-based care business (“MVBC”) of Steward Health Care System. MAX is now the sole value-based MSO for the division. The transaction was made on a part-cash / part-scrip consideration of $25mm in cash, and another 23.5mm Class A MAX shares. The implied valuation on these metrics was approximately $135mm, or approximately 8x EV/FY23 EBITDA.

- The efficiency in which PCM had been able to convert the costs associated with new centre openings into contribution margin was a standout. We noted the growth of primary care centres had proven to be a positive impact on PCM’s overall financial performance. The company had demonstrated an ability to efficiently open new centres [see: previous analysis, Exhibit 2], which has in turn resulted in double-digit increases in PCM’s revenue. This trend contributed to the predictability of the company’s future cash flows at the time helped to enhance its overall value in our estimation.

After reading the above and comparing to the latest investment developments, it will be clear why we changed our position to hold.

Latest investment highlights

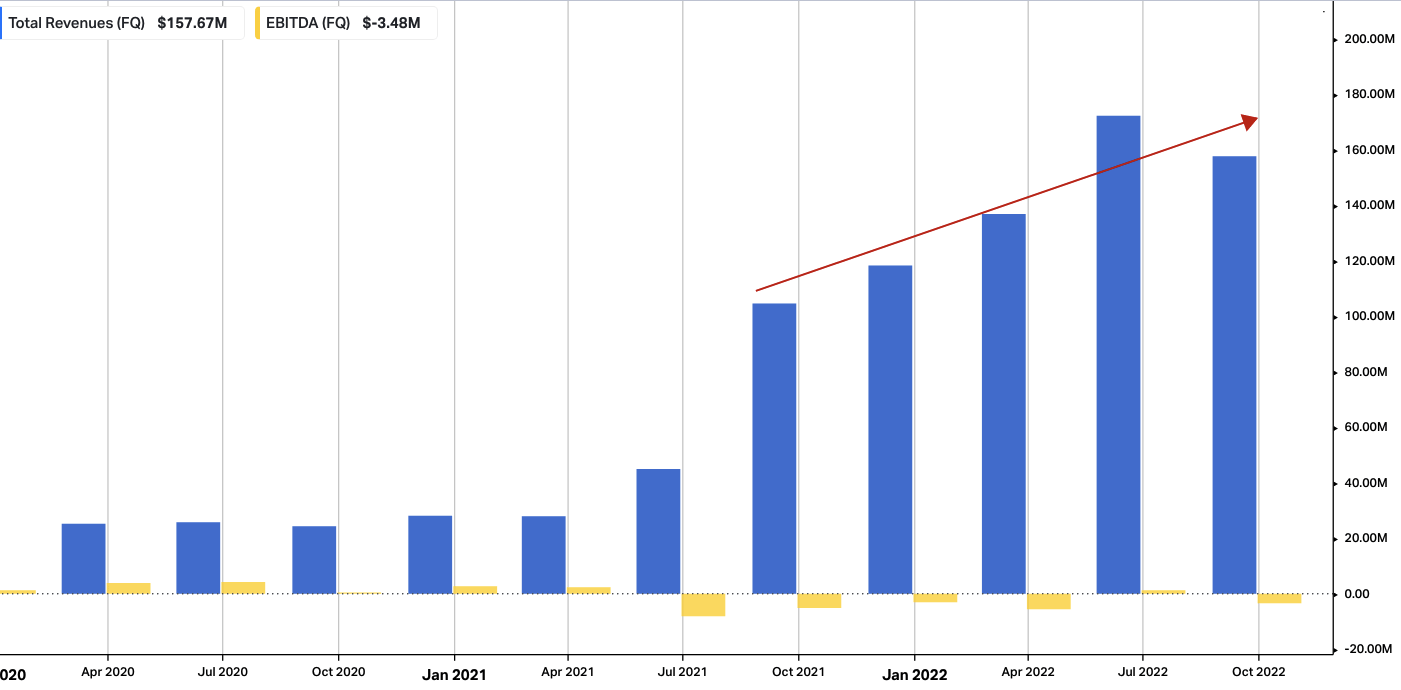

Turning to the latest developments, CMAX had a strong third quarter, with total revenue of $158mm, a 51% YoY growth on adjusted EBITDA of $9.2mm [it reported in early November, like most peers]. This growth was driven by a 60% increase in Medicare risk revenues, and CMAX ended the quarter with 39,500 Medicare Advantage members, a 49% increase compared to the previous year.

Exhibit 2. Sequential revenue growth a standout.

Data: HBI, Refinitiv Eikon, Koyfin

CMAX is targeting a range of $2mm to $3mm for CapEx per clinic for their de novo strategy. The company has been able to secure tenant financing and landlord type financing for the build-outs, resulting in a majority of the costs being included in their rent expense once the clinics are open Hence, there’s more headroom for upsides there. To that effect, CMAX opened three more de novo centers in the fourth quarter, bringing its total center count to 54, and they expect to have 60 centers by the end of the year.

The acquisition of Steward’s Medicare value-based care business was going to be the main highlight in our opinion. We note CMAX drew down $45mm from the delayed draw term facility to fund the acquisition. It also expects to take on additional external financing for Steward’s 2022 Medicare shared savings receivable. Management says it has hosted “numerous town halls with Steward physicians“, educating them and supplying resources to support the deployment of value-based care.

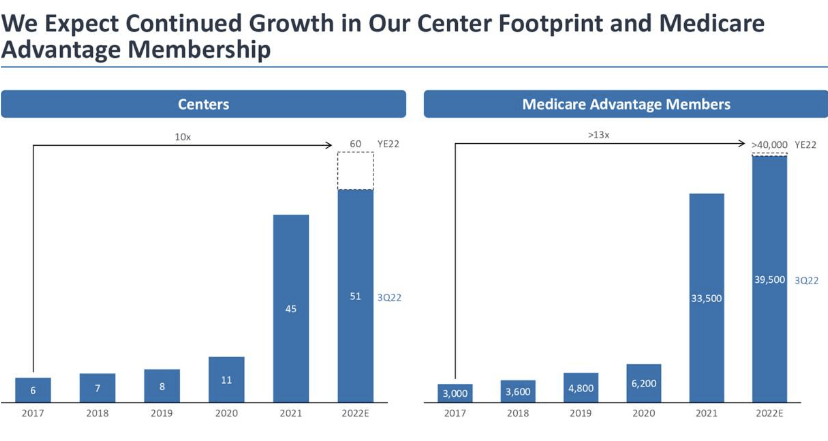

We believe the Steward acquisition will enable it to drive a more selective return on investment capital. We’d also note that CMAX’s core centres still have capacity to grow their membership by more than 50%, not to mention that it reported overall Medicare Advantage penetration in Central Florida is still below 60% compared to over 70% in South Florida. You can see its growth in these segments below.

Exhibit 3. Medicare Advantage penetration

Image: CMAX Investor Presentation

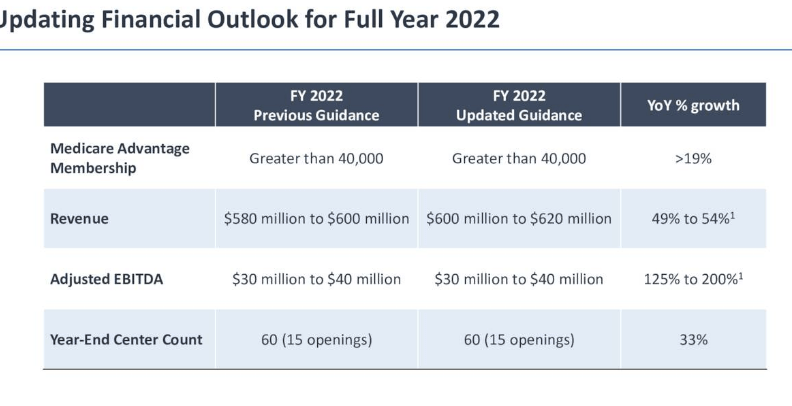

Based on its growth route to date, CMAX is increasing its full-year revenue guidance from $580mm to $600mm to a new range of $600mm to $620mm. It based these assumptions from growth in core organic sales, de novo expansion, and MSO growth.

Exhibit 4. Revenue outlook for CMAX.

- Keep in mind that the updated guidance could be a tailwind for the company leading into the end of H2 FY22.

- However, if it misses this guidance, it could prove to be a downside risk.

Image: CMAX Investor Presentation

Valuation and conclusion

Looking ahead, consensus has the stock valued at $0.8x forward EV/sales. We believe the stock is on a good growth rate, and could hit the upper end of its guidance range. Applying a 1x forward EV/sales multiple [still the sector median] to CMAX’s FY22 revenue estimates derives a price target of $5.60. At the lower end, it’s $5.40. The discrepancy to the current market price, each price target questions if CMAX is undervalued or not.

We aren’t so confident. A rally to these targets would account for a small mean reversion, however, doesn’t necessarily imply there’s overlooked value in the stock. In fact, it could suggest it is just lowly valued in our opinion. Yet, it’s still a talking point to not completely ignore the stock. Hence, the balance of downside factors and the valuation discussed in this analysis supports our hold thesis over rating the stock an outright sell.

Be the first to comment