Harvepino/iStock via Getty Images

Introduction

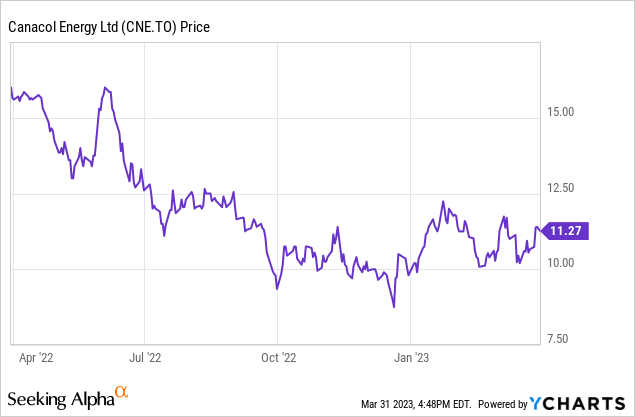

I have been a shareholder of Canacol Energy (TSX:CNE:CA) for quite a while but unfortunately I have yet to realize a positive absolute return. The market is clearly discounting the company’s Colombian operations despite the proven profitability and the subsequent generous dividend policy which is fully funded by the sustaining free cash flow. An additional benefit is the very flat natural gas price in Colombia. While this means Canacol’s average realized price did not increase when the natural gas market was on fire in 2022, it also means the company shouldn’t be hit by the current low natural gas prices in North America as its effectively realized natural gas price will remain stable around $5.

This article is meant to be an update. For all my older articles on Canacol Energy, please follow this link.

The fourth quarter of 2022 didn’t contain any massive surprises

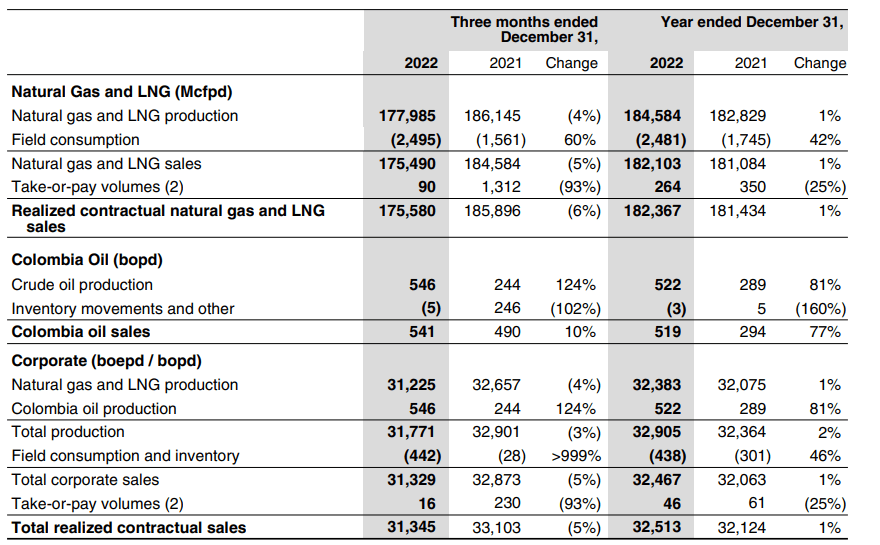

In the final quarter of last year, Canacol produced and sold just over 175,000 Mcf of natural gas per day, and when converted into an oil-equivalent production rate, the natural gas accounted for an attributable production rate of 31,225 barrels of oil-equivalent in natural gas which resulted in a total production of 31,771 barrels of oil-equivalent per day after also adding the actual oil production. The total amount of sales was 31,345 barrels of oil-equivalent per day.

Canacol Investor Relations

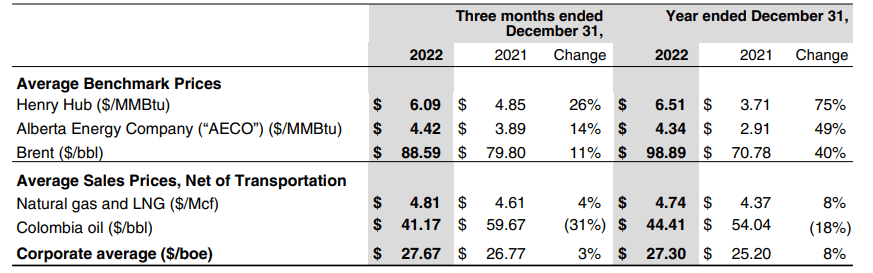

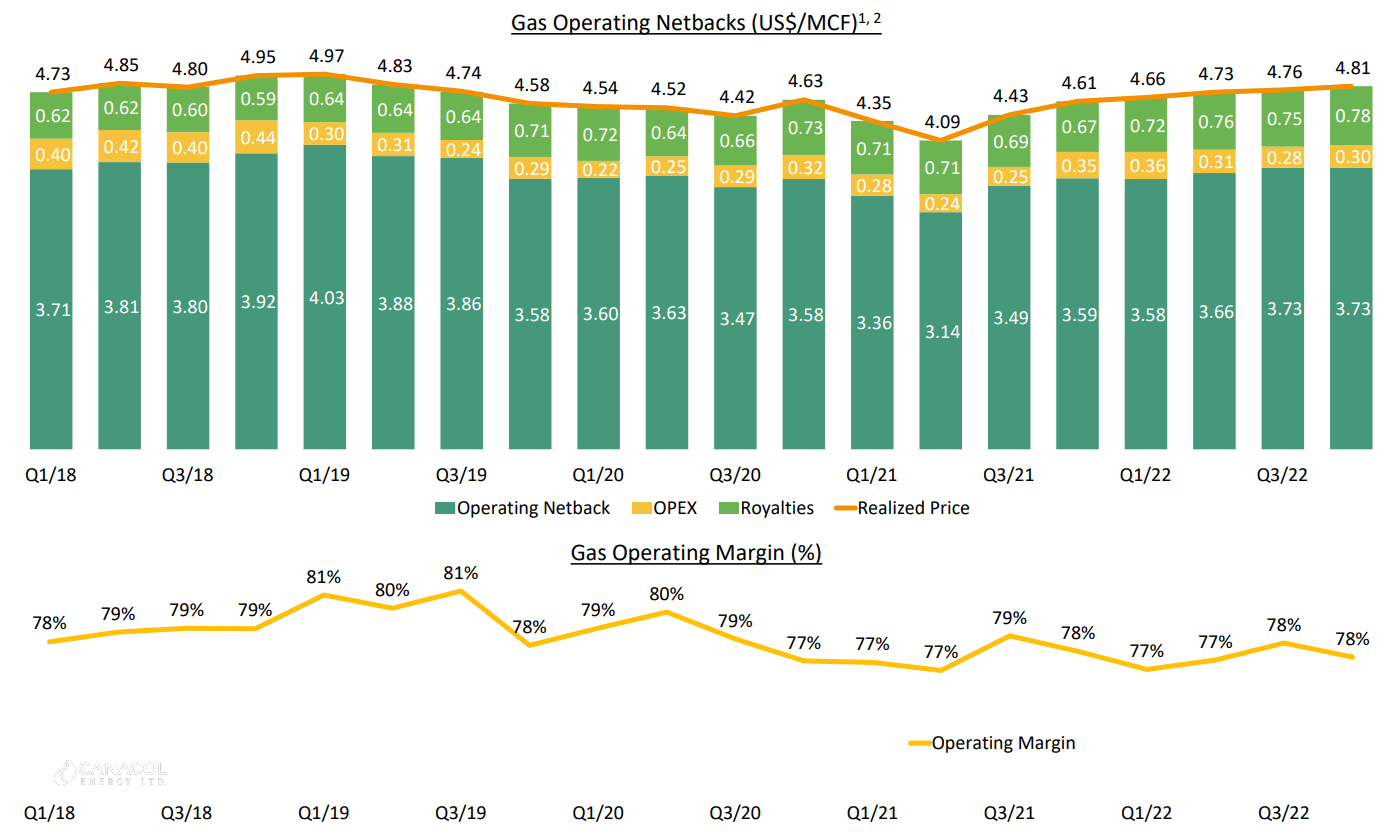

The average received price was approximately $4.81 per Mcf, and the realized natural gas price remains pretty stable given the strong domestic demand and Colombia’s reliance on the import of LNG which is obviously not cheap enough to be a real competitor to domestic natural gas.

Canacol Investor Relations

The image below shows how stable the natural gas price has been in the past five years. It does fluctuate somewhat but it’s for sure not as volatile as the natural gas prices in North America. And thanks to Canacol’s low-cost production base, the operating margins tend to come in around 77%-80% on a very consistent basis. This makes it easier to calculate and predict the cash flows.

Canacol Investor Relations

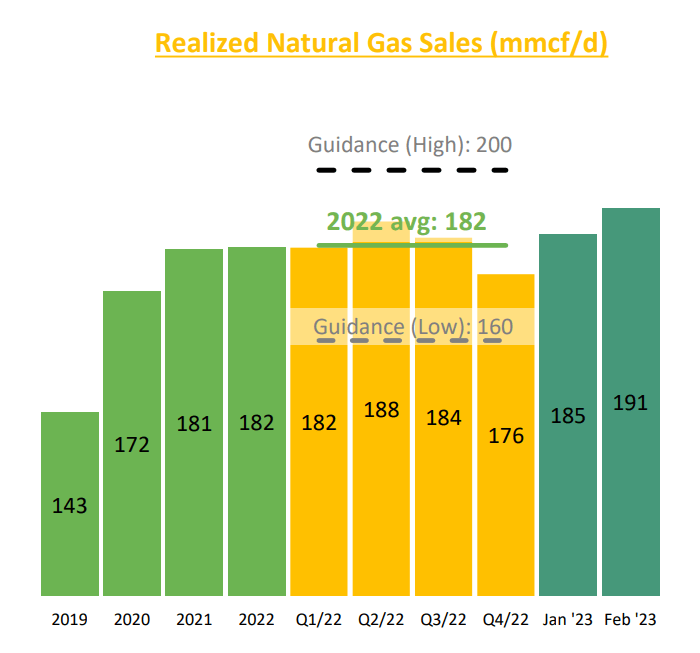

The fourth quarter was OK but weaker than expected as there was a decrease in the natural gas demand due to the high water levels in the reservoirs. The vast majority of the electricity production in Colombia comes from hydro. This was just a temporary effect as the image below shows the volumes picked up again in January and February this year.

Canacol Investor Relations

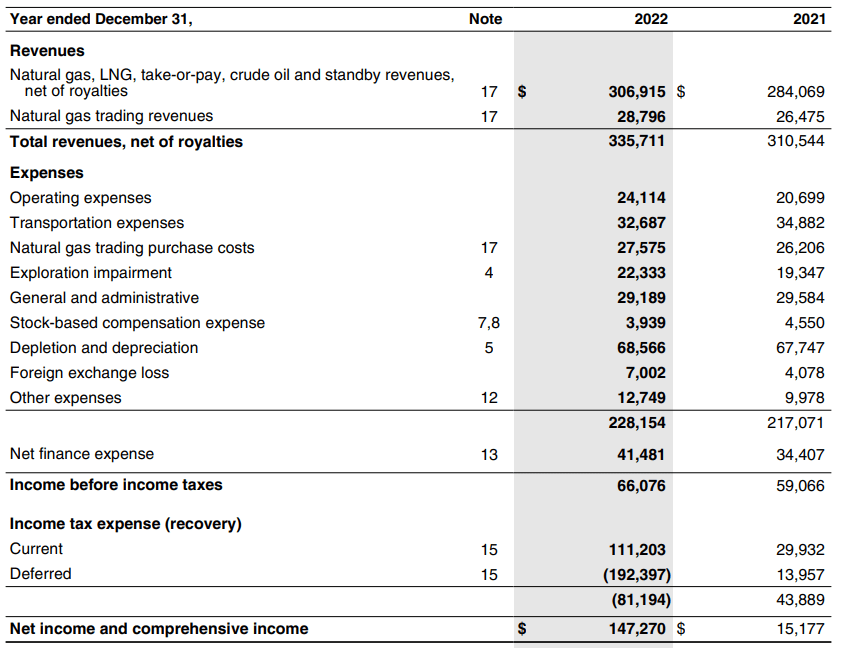

The full-year average production rate was approximately 182,000 Mcf/day and this resulted in a total revenue of $307M while the company also generated an additional $28.8M in revenue from trading activities in natural gas. That’s an activity with a very narrow margin as the company generated just $1.2M in operating profit on these trading activities.

Canacol Investor Relations

As you can see above, the total net income was $147M but that’s entirely caused by a tax benefit. The pre-tax income was just $66M and the normalized net income would have been approximately $23M (as Canacol mentioned a $43M tax bill excluding the restructuring on its conference call). That’s just over C$68M/share and considering there are 34.1M shares outstanding (subsequent to the 5:1 share consolidation), the underlying EPS was approximately C$2/share. Not bad for a stock trading at just over C$11.

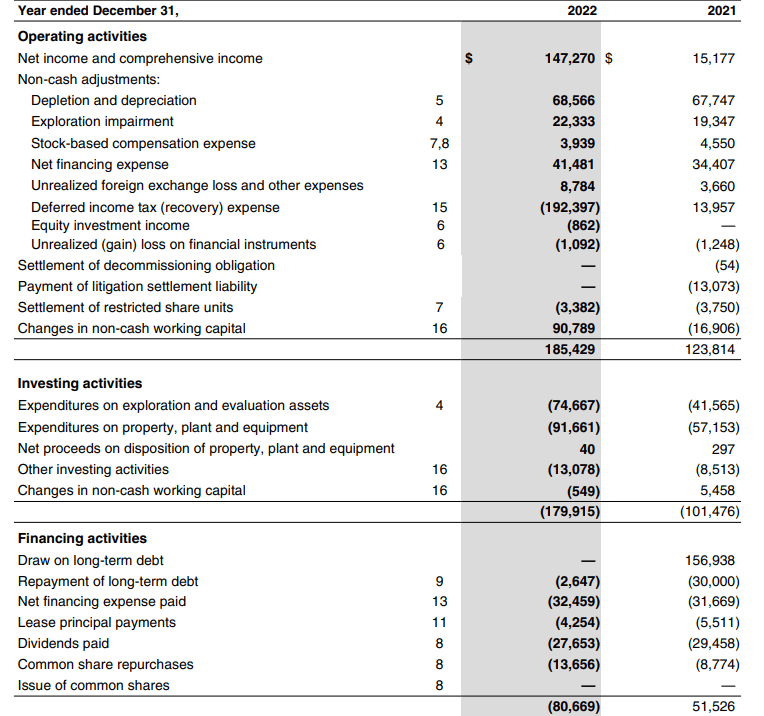

As explained in my previous articles, I’m mainly interested in Canacol’s ability to generate a positive cash flow. And 2022 was another very decent year. Although we see the operating cash flow of $185M on a reported basis was boosted by a $91M cash inflow from working capital changes, it’s important to realize the cash flow statement deducts the $192M in deferred tax gains, but still included the $111M in current taxes. On an adjusted basis (i.e. applying a total normalized tax of US$43M based on the conference call) and after deducting the $37M in lease payments and interest payments, the underlying operating cash flow was $126M. There will be an additional tax bill this year related to the corporate restructuring initiatives but that was not part of the 2022 cash outflow yet.

Canacol Investor Relations

While that wasn’t enough to cover the $166M in capex, I already explained in a previous article the vast majority of the 2022 capex was related to advancing the exploration programs as the sustaining capex was just $54M.

The new reserves update is very intriguing

I’m fine with a company spending quite a bit of cash on exploration as long as it also generates value. Unfortunately the company only had a replacement ratio of 169% in the 2P reserve category but it is encouraging to see Canacol is eyeing 200% for 2023.

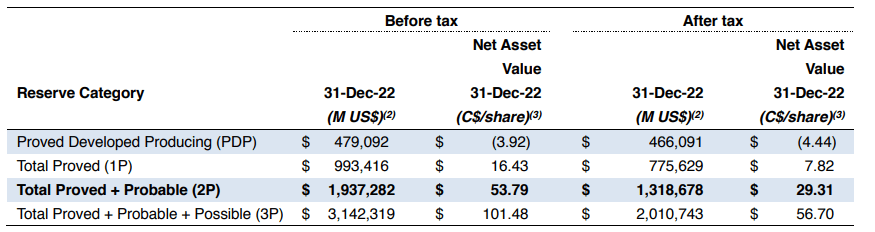

The total NPV10% of the existing reserves is estimated at $1.3B and Canacol also provided the NAV/share on an after-tax basis and after taking the net debt of $578M into consideration. As you can see below, the NAV/share came in at just over C$29, which is almost three times higher than the current share price.

Canacol Investor Relations

Of course this does not take G&A expenses and interest expenses into account so the C$29.31/share overstates what’s realistically achievable, but it does confirm the company is quite cheap right now. That being said, the independent consultants used an average natural gas price of US$5 for this year, increasing to almost $6 in 2027 which is perhaps a tad optimistic.

Canacol Investor Relations

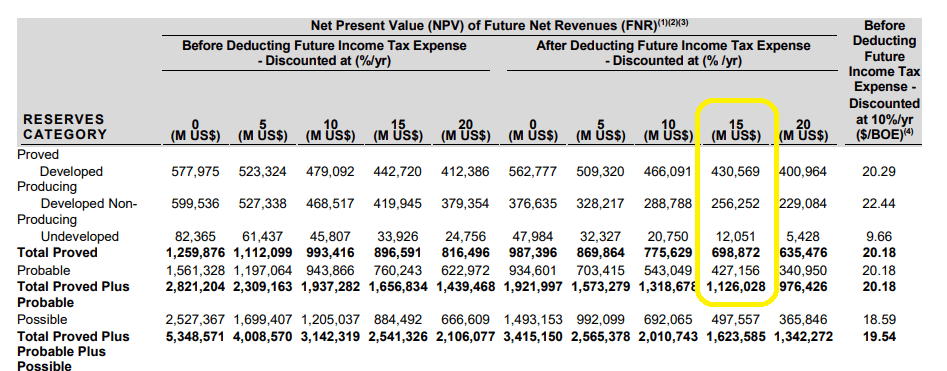

Fortunately the Annual Information Form contains a sensitivity analysis which also provides the PV15 and PV20 values. And if we would use a discount rate of 15% instead of 10%, the after-tax NPV15% is still very respectable at US$1.13B. After deducting the $578M in net debt, the implied equity value (before G&A and interest expenses) is US$548M.

Canacol Investor Relations

Divided over the just over 34M shares outstanding, that’s US$16/share or C$22/share. So there definitely is a margin of safety present.

Investment thesis

While the total production and sales volumes will fluctuate (the official guidance calls for a range of 160-206MMcf/day), it’s important to know the take-or-pay contracts in 2023 cover about 160MMcf/day. The stock is currently trading at just half its after-tax NPV15% and the reserves and PV calculation will further increase this year as Canacol is targeting a 200% replacement ratio for its natural gas reserves.

I have a long position and may add to my position perhaps by recycling a portion of my investment in Canadian gas producer Spartan Delta after its recently announced strategic sale and spin-off. Canacol Energy pays a quarterly dividend of C$0.26 and the C$1.04/share on an annual basis represents a very attractive dividend yield of in excess of 9%.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment