Olga Tsareva/iStock via Getty Images

Overview

Cannabis has come a long way in the USA. Legally speaking, the substance has never been more in favor. With 37 states having legalized medical usage and 21 states having legalized recreational usage, we are in a brave new world. I personally find that the streets of New York are a case study par none when it comes to this; every other time that I step outside, I catch a whiff. In my anecdotal experience, the gold rush here began before the first legal licenses were issued – and it doesn’t seem to be slowing down whatsoever. I won’t be so quick to extrapolate this across to the entire nation, but it’s one data point amongst many.

Nationwide usage definitely appears to be getting higher over the long-term. The most recent Gallup poll in 2022 found that 16% of adults interviewed use marijuana – up from just 7% in 2013. I personally believe this is an understatement. Additionally, common sense dictates that when you make something legal, more people will use it than when it was illegal. Simply put, there’s less stigma.

The effects of widespread state-level legalization are thus acting towards this as well as beginning to come up in the statistics. A noteworthy element of these statistics is the level of usage amongst younger adults (18 to 34). Amongst this demographic, a whopping 30% smoke marijuana with some regularity. Edible usage is at 22% amongst this demographic bracket. Given the younger generations well-known dislike of cigarettes and alcohol, I am inclined to think that cannabis is their vice of choice.

The caveat to all of this is that marijuana sales (on a price basis) decreased across several mature markets in 2022. While it is difficult to pin down the exact amount of cannabis sold by weight, the simple fact remains that less cannabis was sold in 2022 than 2021 on a price basis across large parts of the USA. Notably, the article mentioned here did note that certain high-throughput states such as Colorado saw a decrease in ‘basket size’ (how much weed an average customer purchased). This effect was not distributed across all states, however. The overall impact of this may be lower cannabis sales YoY, although this was not tallied.

This sales volatility is likely due to the US exiting the pandemic era and people going back to more regular patterns of behavior. I would certainly think it’s easier to smoke way more pot when you’re stuck at home; personally, I am not surprised by this fluctuation in sales figures. Additionally, the glut of supply appears to have put downward pressures on prices and reduced unit profits for cannabis.

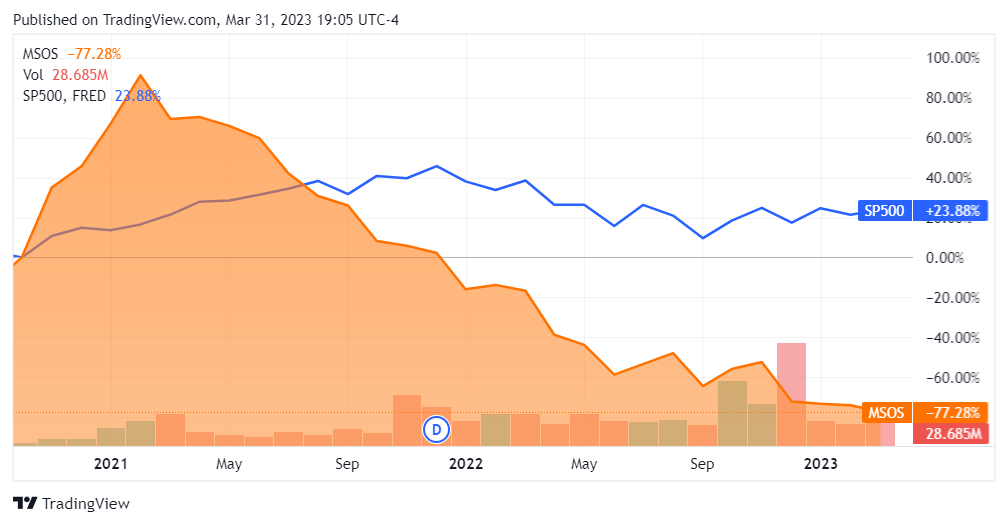

Along with these sales trends, the most well-known US-only cannabis ETF – the AdvisorShares Pure US Cannabis ETF (NYSEARCA:MSOS) – has been sold off significantly since 2021. Entering 2022 already below the S&P500 in terms of price performance, it has continued a downward trajectory and is now significantly underperforming the Index, with a trading beta inception-to-date of roughly -3.24.

Seeking Alpha

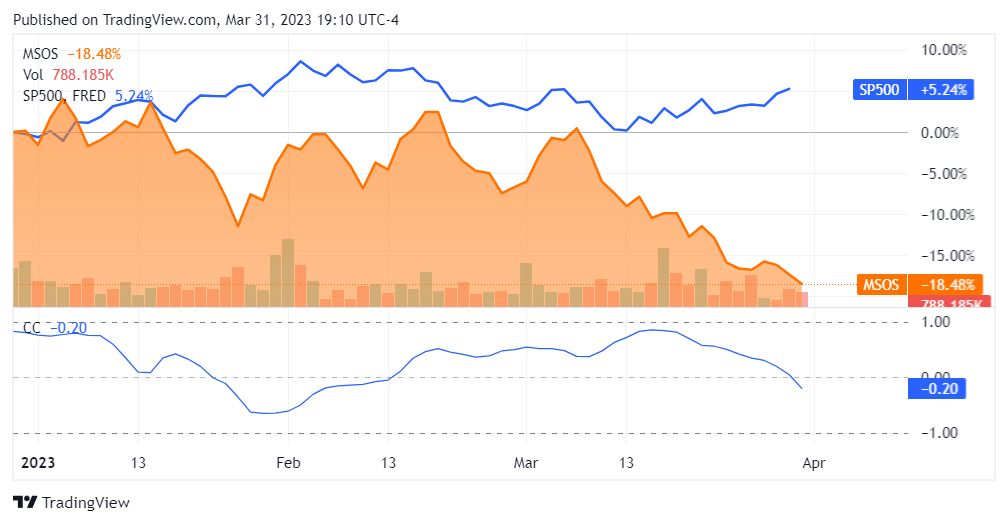

Furthermore, this year has seen this trend continue and seemingly increase in quantitative significance, with the correlation between MSOS and the S&P going negative at times that the S&P was appreciating, including the last two weeks. Clearly the market things cannabis is no longer a good investment at present. This article will explore this theme in more depth to see if it really is the case.

Seeking Alpha

Financials

First and foremost, we need to evaluate if the decline in overall cannabis sales was reflected in the holdings of this ETF. In order, the top 3 holdings for MSOS are:

- Green Thumb Industries (OTCQX:GTBIF)

- Curaleaf Holdings (OTCPK:CURLF)

- Trulieve Cannabis Corp. (OTCQX:TCNNF)

Together these 3 account for 75.7% of the overall (adj. for weightings) holdings of the MSOS ETF.

The respective revenue figures are as follows:

Green Thumb Industries

Seeking Alpha

Curaleaf Holdings ** (Earnings release delayed from initial announce date of March 28th 2023 due to accounting conversion. Data replaced with Trailing Twelve Months figure for 2022)

Seeking Alpha

Trulieve Cannabis Corp.

Seeking Alpha

The numbers here at clear: sales are still up overall. For each of these, 2022 was still a year of growth. Even though we don’t even have the data yet for Curaleaf Holdings’ Q4, the trailing twelve months figure is still higher than any previous yearly performance – indicating that its 3 quarters in 2022 were healthy indeed.

Given the sales performance of these 3 companies – the largest legal cannabis retailers in the US by revenue – I am skeptical that overall marijuana sales ended up lower YoY. While there may have been some volatility, it seems that things picked back up and ended up positive for the year. It is also possible that larger players such as these took over a larger portion of the market from smaller players, although I am not able to confirm this.

There are significant disparities as to profitability and cash flow generation between these 3, but I won’t focus on that within this article. The point here is that marijuana sales remained strong throughout 2022. Since cannabis is a relatively new sector, this is really the core variable that we need to pay attention to. For a growth company or sector, revenue growth is foremost – and we can rest easy that we have maintained that throughout 2022.

Given the large sell-off in these companies reflected in the price of the ETF, we can note that they are now trading quite cheaply on a sales basis. Since these companies are the majority of the ETF we can make use of these valuation multiples to price the ETF as well.

Green Thumb Industries

Seeking Alpha

Curaleaf Holdings

Seeking Alpha

Trulieve Cannabis Corp.

Seeking Alpha

As you can see, each of these companies is now trading at a significant discount to sales on a trailing twelve-month basis – anywhere between 53% to 79% discount to the overall pharmaceuticals space within which they are classified. Again, since these represent the majority of ETF’s value, it stands to reason that the ETF is trading quite cheaply as well.

Conclusion

It seems that the cannabis sector sold off along with the rest of the growth factor. While we continue to see disruptions across early-stage software companies and other future-growth stocks, the situation here is evident: cannabis is still selling well. On a fundamental basis, 2022 was not a down year for these companies or this ETF, and I don’t think 2023 will be either.

The other element to consider here is the overall economic picture and the nature of cannabis as a consumer discretionary good. It is well-known that consumer spending declined in Q4 and that consumer credit is overall quite high. Many voices in professional circles are stating that the consumer is ‘tapped out’ or at their marginal limit in terms of consumption.

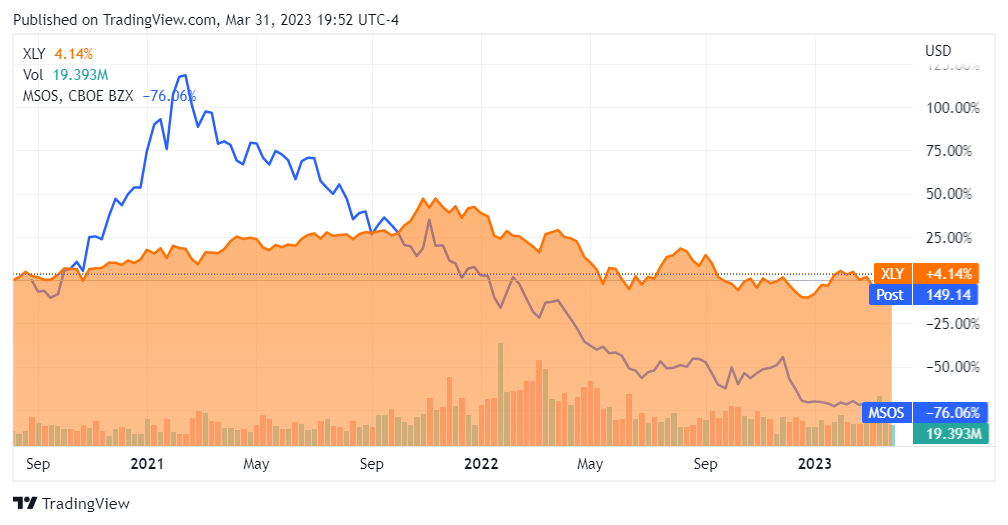

As can be seen below, MSOS is now trading well below the consumer discretionary sector. Interpreting this relative sell off, we can reason that the market believes that cannabis is a lower priority good for consumers than other elements of the consumer discretionary basket. A lower price implies weaker sales growth prospects for cannabis vis-a-vis the consumer discretionary sector. I am a bit skeptical of this.

I don’t think cannabis is a simple consumer discretionary good. I think it is also a substance that creates habits in consumers. While widely understood to be less ‘physically addictive’ than nicotine, I do think cannabis is habit forming and not something a consumer will readily remove from their purchasing basket, if they are indeed a habitual consumer. At a minimum, I would not assume it is a lower priority consumer good than the entire basket of consumer discretionary goods. I believe that there are plenty of consumers out there that would rather use their marginal dollars to purchase cannabis rather than fast food or clothing. As such I expect sales to continue growing throughout this new consumer environment, although perhaps at a somewhat slower pace.

Seeking Alpha

Taking all of this into consideration, I think the cannabis sector has fundamentals that are better than its price implies. Sales have continued growing and should continue growing, and I don’t think the cannabis space should be trading at a worse sales multiple than the rest of pharmaceuticals or at a worse price return than all consumer discretionary goods. On the basis of these facts I am going to call the AdvisorShares Pure US Cannabis ETF a buy.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment