ablokhin

Elevator Pitch

I have a Hold investment rating assigned to Costco Wholesale Corporation’s (NASDAQ:COST) shares.

COST probably can’t rebound back to $600 anytime soon, since its current valuations aren’t really appealing, and the outlook for Costco is mixed assuming a recession happens. As such, Costco isn’t deserving of a Buy rating. But COST shouldn’t be a Sell either, as the company has an unique and successful business model, and there is a long growth runway for its online business. In conclusion, a Hold is a fair rating for Costco.

COST Stock Basics

Prior to discussing the potential for a recovery in COST’s share price, it is necessary to touch on the stock’s basics. I define COST stock basics as the company’s key financial numbers and its business model.

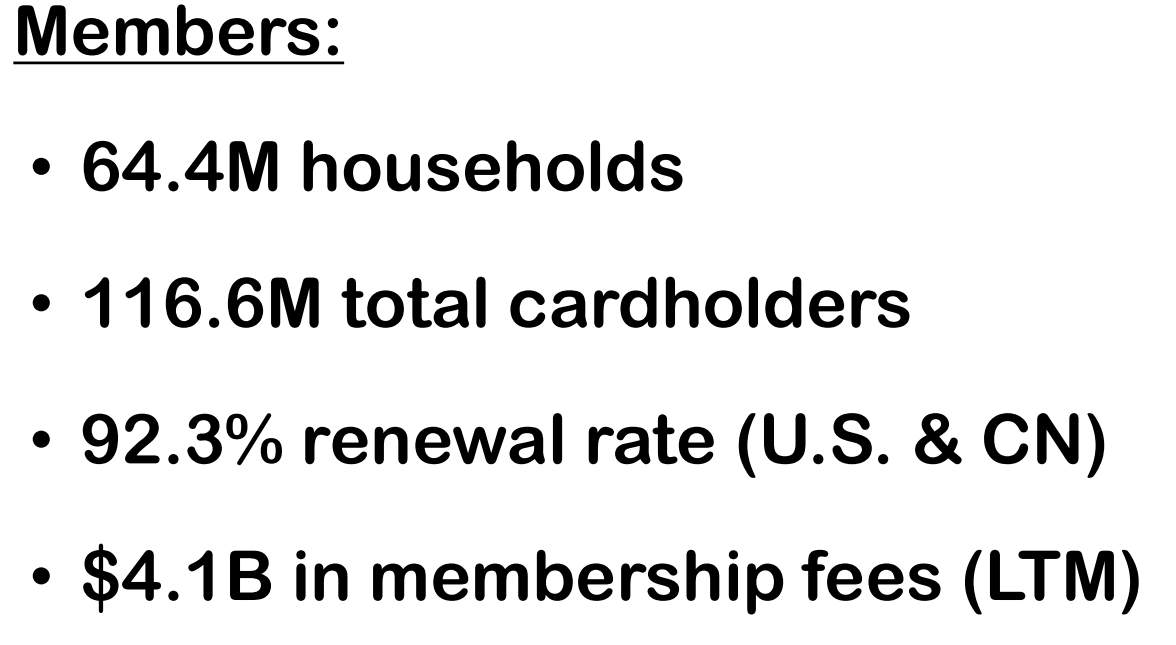

In the company’s fiscal 2021 (YE August 31) 10-K filing, Costco describes itself as an operator of “membership warehouses and e-commerce websites based on the concept that offering our members low prices on a limited selection” will drive “high sales volumes and rapid inventory turnover.” The key figures relating to COST’s warehouses and members can be found in the charts below.

COST’s Retail Footprint As Of End-Q3 FY 2022

COST’s Q3 FY 2022 Investor Presentation

Costco’s Membership Statistics As Of May 8, 2022

COST’s Q3 FY 2022 Investor Presentation

There are three key aspects of COST’s business model that are worth noting.

Firstly, Costco has historically derived more than 70% of the company’s operating profit from membership fees, based on estimates from Reuters and UBS. As such, COST stands out from other retailers which usually generate the bulk of their revenue from merchandise sales.

Secondly, the company’s physical warehouses carry a relatively low number of SKUs (Stock Keeping Units) of around 4,000 as disclosed in its FY 2021 10-K. In comparison, grocery retailers’ SKUs are usually in the tens of thousands. A much lower SKU count translates into greater purchasing power and bulk discounts for COST. This in turn enables Costco to generate substantial cost savings and offer its members more attractive prices for its products.

Thirdly, COST’s private label brand, Kirkland Signature, is estimated to account for a significant 31% of the company’s top line in FY 2021. The high percentage of sales generated from Costco’s private label brand is a win-win for both its members and the company. From the perspective of members, they can have access to reasonably high quality private label products at a lower price as compared to national brands. From the perspective of the company, private labels boast higher margins, and a more favorable revenue mix tilted towards a larger proportion of sales contributed by Kirkland Signature is positive for Costco’s profitability.

Is Costco Stock Undervalued?

I don’t think Costco stock is undervalued now. Instead, the company’s shares appear to be fairly valued or even slightly overvalued.

With respect to relative price performance, COST’s shares are down by -12.0% year-to-date in 2022, but the stock has outperformed the S&P 500 which has corrected by -19.0% over this same period.

In terms of peer valuations, Costco is the most expensive stock among its peers based on the forward P/E and EV/EBIT valuation metrics as per the table below.

COST’s Peer Valuation Comparison

| Stock | Consensus Forward Next Twelve Months’ Normalized P/E Multiple | Consensus Forward Next Twelve Months’ EV/EBIT Multiple | Consensus Forward One Year Revenue Growth | Consensus Forward Two Years Revenue Growth | Consensus Forward One Year Normalized EPS Growth | Consensus Forward Two Years Normalized EPS Growth |

| Costco Wholesale Corporation | 36.0 | 26.1 | +8.5% | +6.2% | +10.1% | +10.2% |

| BJ’s Wholesale Club Holdings, Inc. (BJ) | 20.6 | 19.1 | +6.7% | +4.4% | +10.6% | +13.7% |

| Walmart Inc. (WMT) | 19.0 | 15.6 | +3.2% | +3.7% | +9.5% | +9.2% |

| Target Corporation (TGT) | 15.6 | 14.4 | +4.1% | +3.5% | +42.7% | +12.6% |

Source: S&P Capital IQ

COST’s expected top line expansion for the next two years are superior to that of the company’s peers, and this supports the case of Costco enjoying a valuation premium. However, Costco’s forecasted earnings growth over the same period isn’t the fastest in the peer group.

With regards to historical valuations, Costco’s current P/E of 36.0 times is higher than its five-year and 10-year mean forward P/E multiples of 33.1 times and 29.2 times, respectively as per S&P Capital IQ valuation data.

In summary, COST isn’t undervalued based on a review of historical and peer valuations, and the stock’s price performance relative to the broader market.

Can COST Stock Reach $600 Again?

$600 is a relevant share price level to look at, if one is interested in investing in COST. Costco’s last traded price was $498.90 as of July 11, 2022, so a $600 price target will be equivalent to an upside of +20% and this is the minimum required rate of return which I will demand for any equity investment. Also, COST was trading above the $600 mark just three months ago (more specifically $603.53 as of April 20, 2022), so a potential recovery to $600 seems realistic on paper.

I don’t see COST’s stock price reaching $600 again in the short term, and this is attributable to my mixed views of how Costco will perform in a recessionary environment.

On the positive side of things, Costco has some defensive characteristics, as I have highlighted in an earlier section of this article referring to COST’s stock basics.

COST generates a high proportion of its operating income from recurring membership fees, so its short-term financial performance will be relatively less affected by a sharp decline in merchandise sales.

Costco’s focus on having a smaller number of SKUs and driving a higher proportion of sales from its private label brand is key to the company coping well in a difficult macroeconomic environment. This is because SKU optimization and higher private label sales help the company to keep its company’s costs low, which provides room for COST to keep its product prices reasonably attractive without sacrificing profitability.

On the negative side of things, Costco might find it challenging to raise membership prices in the near term, and the company also sells consumer discretionary products.

At the company’s Q3 FY 2022 earnings briefing on May 26, 2022, COST noted that “increasing our membership fee today ahead of our typical timing is not the right time.” While timing is a potential consideration (there is another one and a half years before a typical five-to-six year cycle of fee increase takes place), it is also possible that Costco had also taken into account weak consumer sentiment in making the decision to avoid raising membership fees earlier. This suggests that there are downside risks relating to the timing and size of the next hike in membership fees for the company.

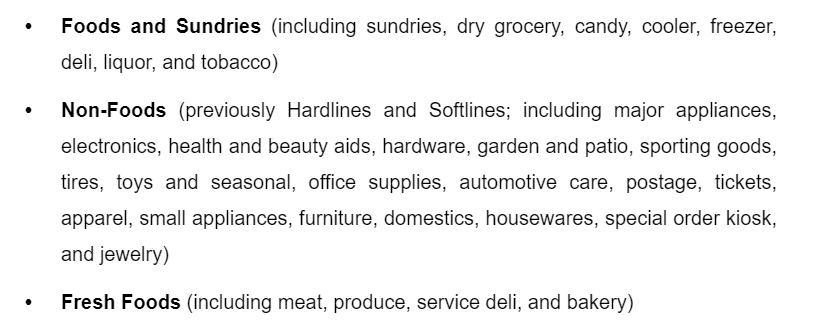

Costco’s Key Product Categories

COST’s FY 2021 10-K

Separately, Costco also has consumer discretionary products like appliances, furniture and electronics in its product mix, apart from food-related products. In the event of a recession, COST’s merchandise sales will still be negatively affected to some extent.

Is Costco Stock A Good Long-Term Pick?

I don’t think Costco is attractive at current valuations as discussed earlier. But I view COST as a good long-term pick as its online sales have the potential to grow in a meaningful way.

COST generates about a mere 7% of its revenue from the online sales channel according to an April 15, 2022 Barron’s article. There is huge growth potential for Costco in this area over the long run. This is because COST’s current business model limits the number of SKUs it can have at its physical warehouses, but there are fewer limitations when it comes to selling online.

Besides relying on its existing e-commerce websites, COST’s Costco Next is the next big driver of future online sales. On Costco Next’s website, COST refers to it as a channel of providing members with “the opportunity to purchase products directly from a Costco Next supplier’s site” to allow Costco to offer “a broader selection of goods to our members.” As per a December 8, 2021 CNN article, COST only “ramped it (Costco Next) up” at the end of last year by including more suppliers and widening the range of products for Costco Next, even though Costco Next was launched as early as 2017. In other words, Costco Next could play a key role in the acceleration of COST’s online sales growth in the intermediate to long term.

Is COST Stock A Buy, Sell, or Hold?

COST stock is a Hold. Taking into account its current valuations, its potential performance in a recessionary environment, and the growth opportunities for its online business, a Hold is the most appropriate investment rating for Costco.

Be the first to comment