smshoot/iStock via Getty Images

Introduction from John P. Calamos, Sr., Founder, Chairman, and Global Chief Investment Officer

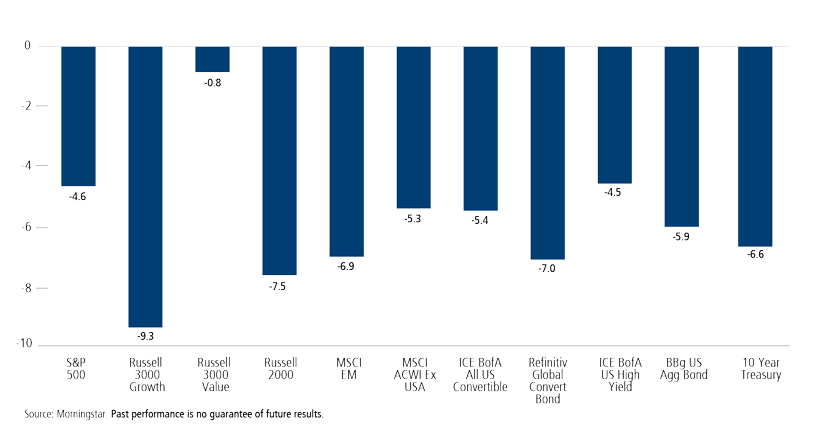

During the first quarter, markets were battered by surging volatility and vicious rotations. Russia’s invasion of Ukraine, sanctions, the start of a tightening cycle by the Federal Reserve, and new Covid lockdowns in China exacerbated investors’ longer-running anxiety about inflation, supply chains, commodity shortages, and interest rates. Oil prices soared and the yield of the 10-year US Treasury spiked upward. Against this backdrop, few areas of the global capital markets were unscathed, and both stocks and bonds retreated. As emotions ran high, even fundamentally strong companies experienced sharp selloffs.

Global Asset Class Performance, 1Q 2022

Total Return %

These next months will continue to test the resolve of investors. The war in Ukraine, Fed policy, Covid-19, inflation, and an uncertain US fiscal policy backdrop each create formidable crosscurrents, and the markets must wrestle with all of them at once. The Fed has a big lift to manage, and we expect markets to reflect an ongoing debate over whether policymakers will be able to engineer the soft landing they seek. We are prepared for choppy, sideways-moving markets where sentiment at times overtakes fundamentals. Selectivity and individual security section will be key, as we are likely to see diverging fortunes, even among companies in the same sector or even the same industry.

Although selloffs can be difficult to stomach, they are a normal part of the market cycle. The best strategy is to not get caught up in market headlines or give in to the temptation to try to time the market. We’ve also seen some stabilization in the equity markets over recent weeks, as well.

Indeed, I’d encourage every investor to remember that the markets and the global economy are resilient. Through 50-plus years, I’ve seen that there are long-term investment opportunities in all environments. As you will read in the commentaries that follow, our teams share this view. In these fast-moving markets, they are relying on discipline and long-term perspective to manage downside risks and pursue opportunities across asset classes.

With so many variables right now, it’s important to not get distracted by a single economic data release, earnings announcement, or news headline. What matters is how all the pieces fit together—and that’s where we believe our decades of experience in the markets will allow us to position our portfolios advantageously. Below, they share their perspectives on the economy and markets, and how they are positioning the Calamos funds. We will be adding commentaries over the coming days, as well.

US Convertible Update: Short-Term Volatility Can Create Long-Term Opportunity

Calamos Convertible Fund (CICVX), By Jon Vacko, CFA and Joe Wysocki, CFA, April 7, 2022

The equity and credit markets faced considerable pressures in the first quarter as geopolitical risks intensified and added to an already uncertain macro backdrop. Convertible securities were not immune to the increase in volatility that took hold. Against this backdrop, the pace of new issuance was also subdued, with $8 billion of new global convertibles coming to market during the quarter. This issuance activity trails the accelerated pace investors had grown accustomed to since 2020 and is also below the long-term seasonal pace we would expect during the first months of the year. Although we have anticipated deceleration in the annual volume of new convertibles after back-to-back years of near-record amounts, we believe heightened global uncertainty materially influenced first-quarter issuance. We expect that an eventual calming in global capital markets should help boost volumes back to a more traditional seasonal pace for the rest of the year.

Our focus in Calamos Convertible Fund continues to be on actively managing the risk/reward trade-off. Convertibles are hybrid securities that can act like equities or bonds, depending on movements in the markets. In periods of larger-than-typical moves, such as we have seen recently, these dynamics can rapidly change.

We continue to favor the balanced portion of the convertible market where structural asymmetrical profiles offer more potential upside than downside. We are underweight and highly selective within the most equity-sensitive portion of the market where convertible structures may lack material downside risk mitigation.

Although macro risks have increased and the markets continue to adjust to a tightening monetary policy, history has shown that periods of short-term volatility can lead to longer-term opportunities. For example, the recent pullback in the underlying stocks of convertible issuers has pushed the equity sensitivity of the overall convertible market toward the lower end of the range seen since the pandemic began. Among these less-equity sensitive names, we believe there are opportunities for us to invest in companies that have the potential to become future market leaders, without taking on full equity downside risk.

On a sector basis, technology is the fund’s largest overall allocation, as we continue to identify many innovative companies and convertible structures with attractive risk/reward characteristics. The consumer discretionary sector is the fund’s largest relative overweight because we expect consumer demand for services to drive returns. The fund’s largest underweight is to financials, due in part to convertible structures that are more exposed to rising interest rate risk.

As we have seen over prior market cycles, actively managing the changing dynamics of convertibles through volatile times such as these provides us with powerful tools for mitigating further equity declines while still retaining upside equity optionality.

Small Cap Stocks: Poised to Lead Once Again

Calamos Timpani Small Cap Growth Fund (CTSIX), Calamos Timpani SMID Growth Fund (CTIGX), By Brandon Nelson, CFA, April 5, 2022

Macro concerns relating to Covid-19, rising inflation, the trajectory of the Federal Reserve interest rate tightening cycle, and geopolitical unrest dominated the first quarter. As a result, stock price valuation multiples fell, even though analyst earnings estimates for 2022 actually went higher during the quarter. The net result of this valuation-versus-earnings-revisions tug-of-war was losses across the board. Large-cap stocks (as measured by the Russell 1000 Index) fell by 5.13%, and small-cap stocks (as measured by the Russell 2000 Index) fell by 7.53%, lagging large caps by 240 basis points.

Interestingly, small-cap underperformance was confined to January, even though macro concerns intensified after January. For the combined period of February and March, small caps had the performance edge by a magnitude of 179 basis points.

Small caps have lagged large caps for several years. Perhaps the recent performance improvement is an early sign that small-cap valuations have neared a relative bottom and small caps may be poised to become a leading asset class once again. We believe this scenario is likely. Although the past cannot predict the future, it can provide investors with useful context. Based on long-term history, research suggests that over the next five years, there is an 84.2% chance that small caps outperform large caps by 8.1% per year.* Asset allocators would be wise to be aware of these remarkable odds.

We believe the aforementioned setup is especially favorable for Calamos Timpani Small Cap Growth Fund (CTSIX) and Calamos Timpani SMID Growth Fund (CTIGX), given their disproportionate exposures to small caps and average market caps that are smaller than their benchmarks and peer groups. We believe our fundamental security selection positions us advantageously to add further value beyond the stand-alone asset class performance.

Both funds continue to have exposure to long-term secular growers and certain cyclical growth stocks that we believe should benefit meaningfully from a continued economic uptick. A noteworthy portfolio change we made early in the first quarter was to increase the funds’ weightings in energy stocks, an area that could continue to see high growth and underestimated growth trends in the coming months. We also increased exposure to certain health care stocks that should benefit from pent-up demand for elective medical procedures.

*Source, Steven Desancitis, Jefferies, using CRSP, the University of Chicago Booth School of Business and Jefferies.

Fixed Income Update: Migrating Toward Higher Quality to Counter Uncertainty

Calamos High Income Opportunities Fund (CIHYX), Calamos Total Return Bond Fund (CTRIX), Calamos Short-Term Bond Fund (CSTIX), By Matt Freund, CFA; Christian Brobst; and Chuck Carmody, CFA, April 5, 2022

To paraphrase Donald Rumsfeld, there are knowns, known unknowns, and unknown unknowns. According to history, it’s the unknown unknowns that can really get you, but we are living in a time with an extraordinary number of known unknowns, and they currently dominate the headlines and the markets. Whether it’s Covid-19, the European war, supply chain disruptions, midterm elections, or energy, the situation teems with uncertainty.

Inflation: Multiple forces are driving prices higher, including continued supply chain challenges, commodity price pressures, and housing. It’s challenging to know how much is structural and how much is temporary. We are hopeful that price spikes in conflict-area sourced items (e.g., neon gas, titanium, wheat, fertilizer) will prove more temporary. At a minimum, there’s been a large one-time upward revision to prices, but the likelihood of a long-term wage-price reaction has increased. If higher inflation expectations become entrenched in consumer behavior decisions (i.e., buying now because items will cost more in the future), the problem will be exacerbated.

Fed policy: What can the Fed do about this situation? The Fed is in a bad spot—there are no two ways about it. The Fed’s goal is to slow aggregate demand without hindering labor conditions. It’s worth pointing out that only once since WWII (in the mid-1990s) has the Fed navigated a soft landing by threading that needle. Six weeks ago, it was clear that the Fed was still focused on balancing to its dual mandate, but recently its focus has shifted abrasively to halting price pressure. We expect the Fed to be very aggressive early in this tightening cycle. This aggressiveness is likely to fade by the second half of the year because the Fed will have to evaluate the impact of reducing its balance sheet in real-time as it navigates these uncharted waters.

Fiscal policy: Political gridlock gripped Washington much quicker than anticipated, starting with last year’s failure to pass “Build Back Better.” Stimulus is on track to decline dramatically over the course of 2022, which will be a de facto economic decelerator. In a midterm election year, we expect there will be plenty of support to pass legislation that puts money in the hands of consumers, but given the inflationary backdrop, the opposition will be staunch. The likelihood of a Republican majority in the Senate or both houses of Congress is growing. This would stall most, if not all, progress on the Biden administration’s domestic agenda. That said, if Biden finds an administrative action to forgive $1.6 trillion in outstanding federal student loan debt, this would equal the economic value of the reduced Build Back Better proposal that failed in December.

Economic and credit conditions: Despite the current challenges and a clearly decelerating set of data, most economic data measures indicate underlying strength. Measures of labor market health, aggregate demand and consumption, and management surveys are robust. One area of weakness is in measures of consumer confidence, which are falling because of reduced expectations for the future, which we primarily attribute to current inflation levels. Put it all together, and the picture remains relatively sanguine in comparison to the past decade—if inflation can be put in check.

In the meantime, borrowing costs for companies and households have increased, but credit is still readily available. Our assessment of corporate fundamentals suggests steady improvement of leverage and interest coverage on the back of record revenue and EBITDA growth, even in non-energy-related sectors.

Positioning implications: Our base case anticipates a more volatile spread environment with moderately higher interest rates over the balance of 2022. Rapid changes in communication from Fed have led to market rates already pricing in an aggressive path of tightening. In our view, the Treasury curve inversions we have seen to this point simply reflect that aggressiveness. (For more on Treasury curve inversions, see our post from 2018, “The Underappreciated Swap Curve.”) But the risk of a Fed policy error has increased, given the high level of volatility, and the possibility of a substantive exogenous shock feels more pronounced than in previous quarters. As a result, we have migrated the positions for our fixed income strategies (Calamos High Income Opportunities Fund, Calamos Total Return Bond Fund, and Calamos Short-Term Bond Fund) toward higher-quality credits. We are also emphasizing our focus on being well compensated for the idiosyncratic risks in our portfolios. Although we continue to doubt that the above-trend inflation environment will lead to drastically higher interest rates in long-dated maturities, we are maintaining cautious duration implementation across strategies.

Capitalizing on Volatility to Build Long-Term Value

Calamos Global Sustainable Equities Fund (CGSIX), By Jim Madden, CFA, Tony Tursich, CFA, and Beth Williamson, April 5, 2022

With the daily horrors in Ukraine providing a somber backdrop, global equities endured a volatile start to 2022, with most markets finishing the first quarter well into the red. The combination of supply chain issues, inflation, and rising interest rates unnerved investors who found safe havens hard to come by. Some of the worst-performing stocks for the quarter included former pandemic superstars, reminding investors that indiscriminately loading up on what’s in favor under certain market conditions can result in painful losses down the road.

Looking forward, central banks have a delicate balance to maintain. Inflation continues at high levels while growth has shown signs of slowing. How much and how fast they should raise rates becomes the key questions, given that monetary policy cannot support growth and fight inflation at the same time. US Fed Chairman Powell hinted at a more hawkish attitude in late March; and this time, markets seemed to take him seriously, spiking yields up and bond prices down as investors started adjusting to a new era.

Higher rates mean higher mortgage costs, which will affect the red-hot housing market. Higher rates mean it is more expensive for companies to repay or refinance their debt. Rapid increases in the price of money have many known economic effects, but perhaps more concerning is what unintended consequences will result as the world moves away from easy money.

Nothing illustrated the volatility of the quarter like Chinese stocks. A yearlong downturn was punctuated by a precipitous fall in mid-March followed by a massive upturn as the Chinese government signaled support for its markets. Rally notwithstanding, there remain questions regarding the investability of numerous Chinese stocks.

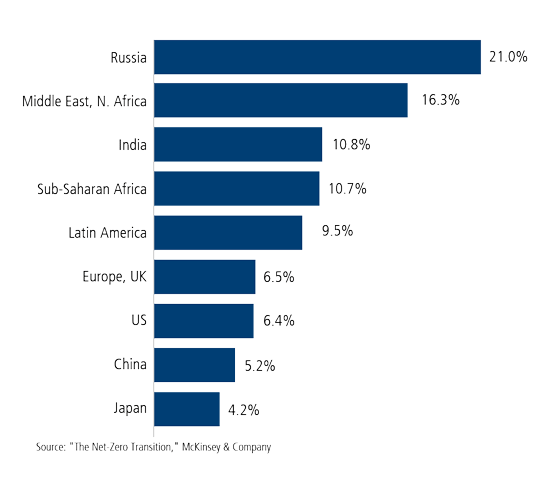

A recent study from McKinsey & Co. estimates that the investment needed to reduce the impact of greenhouse gas pollution to zero by 2050, in alignment with the Paris Agreement, could be $9 trillion annually. Scientists agree that the cost of not meaningfully advancing toward the global climate goal will be much greater. Cooperation by everyone from national leaders to individual citizens is essential. Corporations will need to adjust business models, develop new products, retool supply chains, and make prudent long-term capital decisions to gain efficiencies and remain competitive. Investors who can navigate this transition successfully will be rewarded. The Calamos Sustainable Equities team is focused on doing just that.

Cleaning Up

Developing and fossil-fuel-heavy regions face the greatest burden to reach net-zero emissions.

Net-zero investment as a fraction of 2021‒2050 GDP

Times of volatility can be unnerving for investors but are also times when shares of quality companies can be bought at discounted prices. We view volatility as an opportunity and a time to build long-term value.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Be the first to comment