sankai

Description

I believe the investors have already revised their expectation on Cadence Design Systems (NASDAQ:CDNS) stock given the strong 4Q22 performance, 1Q23/FY23 growth and margin guidance, as evident in the multiples and stock price. While I like the results and outlook, I think the current multiples leave investors with no room for error. If it were to miss guidance or show any signs of derail, it is very possible that CDNS stock gets a double whammy: EPS revised downwards and multiples to revert to mean. I am certainly not going to put myself in that situation, no matter how much I like the company performance.

4Q22 Review

Fourth-quarter revenues for CDNS increased 16% year over year to $900 million, beating consensus estimates of $885 million. This strong growth is driven by performance in all segments. First, adoption of its digital tools contributed to a 12% increase in digital IC revenue. Second, custom IC grew by 7% due to sustained analog growth. Third, hardware emulation and prototyping have been driving forces behind the 39% increase in functional verification. Fourth, strong expansion in the system analysis segment was fueled by expanding presence across a variety of sectors. Fifth, IP income was consistent sequentially due to consistent foundry activity.

In turn, all these contributed to a strong gross margin, which led to a 36% operating margin and $0.96 in EPS.

Industry & growth

Despite the semi-con industry slowing down in FY23, I anticipate that the solid chip design activity will keep demand for chip design software (a major revenue driver for CDNS) high. Demand for CDNS solutions is also expected to increase as chip designs become more complex. This high demand is reflected in 4Q22 results, where CDNS printed strong results and provided a solid 1Q23 outlook, as well as FY23 revenue growth guidance of 12-14%. (much higher than consensus estimates). Emulation and prototyping, as well as strong activity and complexity in chip design, new customers, and market expansion, all contribute to this strong expected growth. Specifically on hardware emulation and prototyping, I see good potential as I believe it is a key spending for underlying customers. In that, it allows them to quickly test their designs and jump into software/firmware development at an early stage, saving them time and money over the long-run. Further, management saw robust demand across all of its Electronic Design Automation [EDA] business segments. The introduction of new products is also meeting with resounding success. More importantly, the book-to-bill ratio is a crucial indicator that the projected increase in revenue for FY23 can be easily realized.

In addition, I see EDA as the most defensive part of the value chain. For instance, both CDNS and Synopsys (SNPS) have continued to grow revenues even during previous down turns. As such, I continue to view CDNS with a positive lens that the industry will continue to grow and CDNS will benefit from it.

Guidance

Powered by a healthy backlog, a robust pipeline of new products, continued business stability, and rising confidence in its hardware emulation and prototyping operations, management guided to a 12–14% y/y revenue growth in FY23. Specifically, management expects robust hardware performance through 1H23, but is factoring some 2H conservatism into their plans. I remain convinced that design complexity verification and the speed of software development are two key tailwinds for CDNS hardware emulation and prototyping. Given that the book-to-bill ratio was healthy at 1.3x in 4Q22, I am optimistic about CDNS ability to hit its overall guidance in FY23. More importantly, for margins, the guided margin for FY23 is a record high, which supports my belief that CDNS profitability still has room to further increase (not limited by historical figures).

For 1Q23, management guided revenue of $1.01 billion at the midpoint, based on sustained growth across all segments. In particular, the operating margin was guided to 41.5%, and management expects the strength in hardware sales to continue into the 1H23.

Valuation

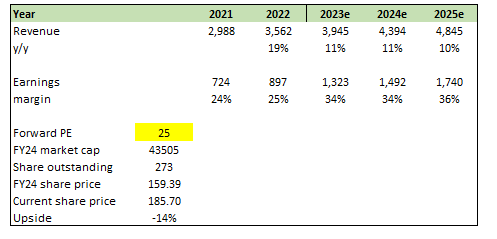

Despite the positive views on the business, I believe investors has priced in a lot of the positive upside in the stock. As can be seen in the forward earnings multiple (38x). Based on my model, using consensus figures, and a multiple of 25x, which I think is far more reasonable for a mid-teens earnings grower, translates to a share price of ~$160, which is 14% below current share price. While I believe there is room for management to beat consensus figures (management guidance is higher than consensus growth expectations in FY23), I think a massive beat with further valuation re-rating upwards is required for investor to generate attractive returns.

Author’s calculation

Summary

CDNS reported strong 4Q22 results, with a 16% y/y increase in revenues driven by growth in all segments, leading to a 36% operating margin and $0.96 in EPS. Despite a slowing semi-conductor industry in FY23, CDNS is expected to benefit from high demand for chip design software and hardware emulation/prototyping, leading to solid growth and margin guidance. However, the current high multiples leave little room for error, and the stock could be negatively impacted if CDNS misses guidance or shows signs of derailment. While there is potential for management to beat consensus figures, a massive beat with further valuation re-rating upwards is required for attractive returns.

Be the first to comment