ArtemisDiana

C3.ai (NYSE:AI) is a tech stock that had been left for dead until most recently, when investors suddenly became very enthusiastic for the future of artificial intelligence. Growth has slowed down precipitously as the company has completed its conversion to a consumption-based pricing model and is also facing macro headwinds. Yet as the company continues to move closer towards profitability, I expect the $858.8 million in net cash on the balance sheet to gain more attention as this remains a $2.5 billion company. AI remains buyable here as the valuation is not pricing in the potential for growth to reaccelerate meaningfully as management executes against multi-year plans.

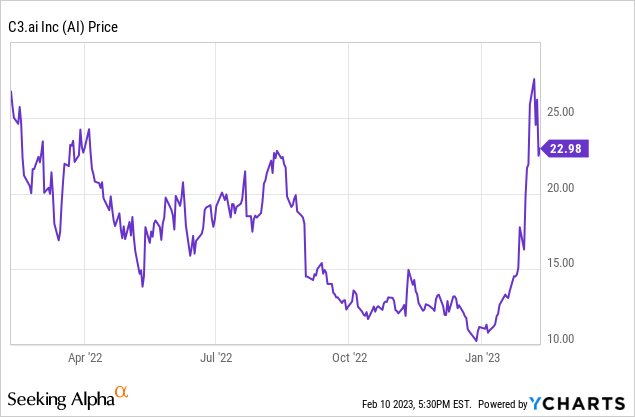

AI Stock Price

As a pure-play artificial intelligence tech provider, AI initially saw its stock bid up to astronomic levels in early 2021. That hype has faded – and more – as the stock has since traded down 90%. But some of that hype seems to have come back in 2023.

I last covered AI in November where I rated the stock a buy on account of net cash making up 70% of the market cap. The stock has since soared 85%, in part due to its progress towards a reacceleration in growth rates but mostly due to the latest craze in artificial intelligence.

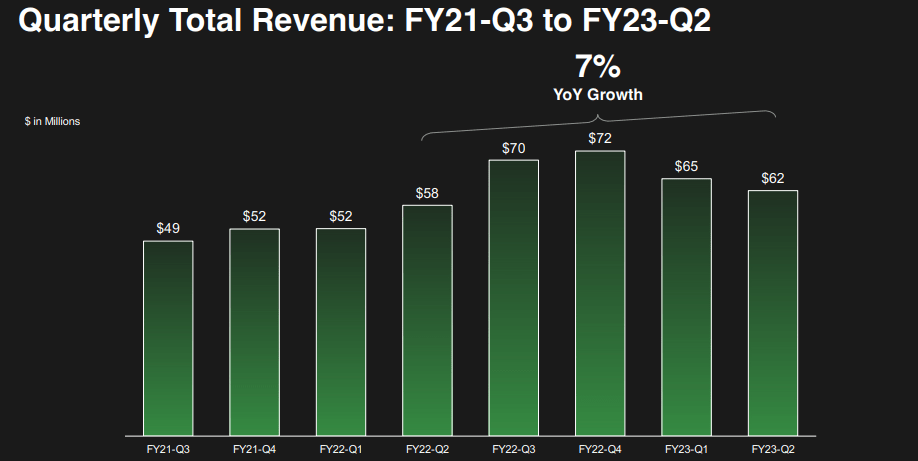

AI Stock Key Metrics

The latest quarter saw further sequential declines in revenue but was the first time that revenue growth decelerated so meaningfully on a YOY basis, with revenues growing just 7% YOY to $62 million.

FY23 Q2 Presentation

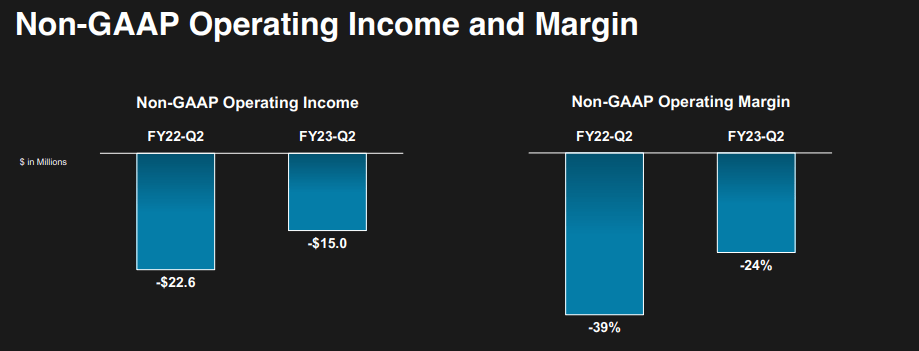

Meanwhile, AI showed some operating leverage with its non-GAAP operating margin loss improving 15 percentage points to 24%.

FY23 Q2 Presentation

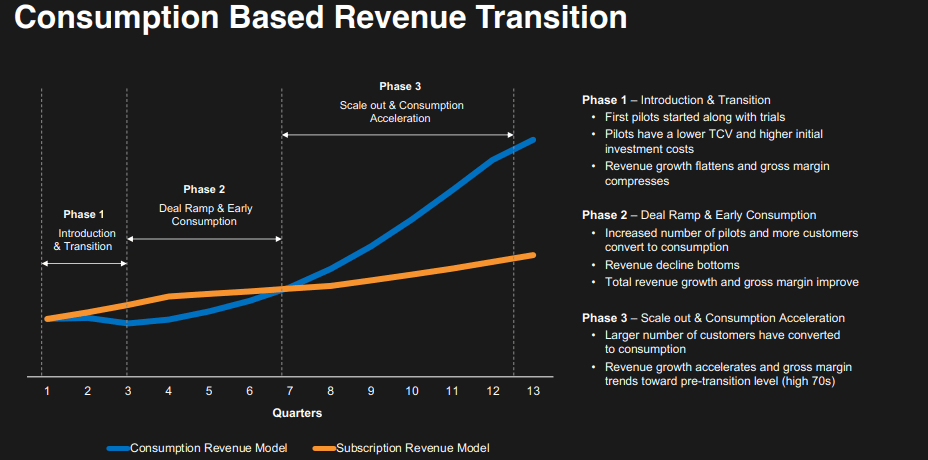

The slowdown in revenue was to be expected as AI completed its transition to the consumption-based model in the quarter. As seen below, management expects the transition to lead to near term headwinds to growth before leading to stronger growth over time.

FY23 Q2 Presentation

On the conference call, management explained the projected acceleration in growth as follows:

We expect this new model to increase the number of customers with which we engage in any given quarter by an order of magnitude. As these customers continually increase their usage over time, we expect the compound effect on revenue growth to be quite significant.

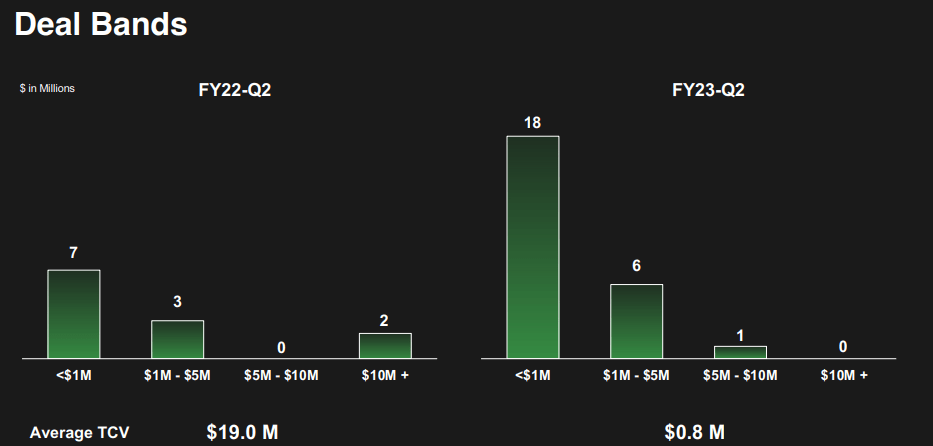

That transition also led to a significant reduction in contract value, with the average contract value standing at $0.8 million versus $19 million from one year prior.

FY23 Q2 Presentation

AI ended the quarter with $858.8 million of cash and no debt which should be more than enough to fund operating losses for 9 years based on the projected FY23 run rate. Even so, management noted that they expect operating profitability on a non-GAAP basis by the end of fiscal 2024 (the most recent quarter was FY23 Q2). I note that the guidance implies profitability not for FY24 but instead beginning in Q4 of FY24.

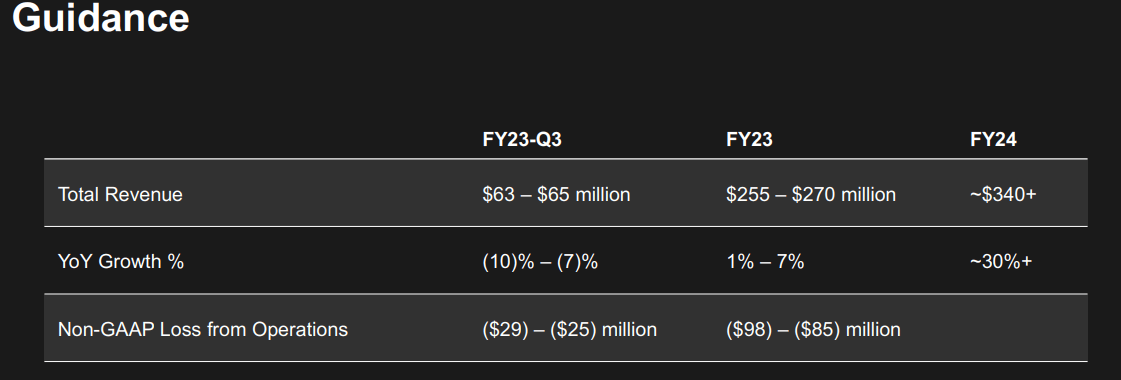

Management is guiding for this year to see only 7% YOY revenue growth at the high end before accelerating to around 30% growth by FY24.

FY23 Q2 Presentation

Why Is AI Stock Soaring?

AI stock is up over 100% year to date. That is probably not due to the fundamentals. Amidst growing enthusiasm for ChatGPT, AI announced its C3 Generative Product Suite, that integrates AI capabilities from OpenAI, among others, into its existing product offerings. It is not entirely clear what that really means – but investors do not seem to care. This announcement seems to have reminded meme investors about the convenient “AI” stock ticker, with AI seemingly soaring in-line with enthusiasm for ChatGPT. While the stock has sold off some from recent highs, it is clear that the stock is beginning to move because of factors beyond the fundamentals.

Is AI Stock A Buy, Sell, Or Hold?

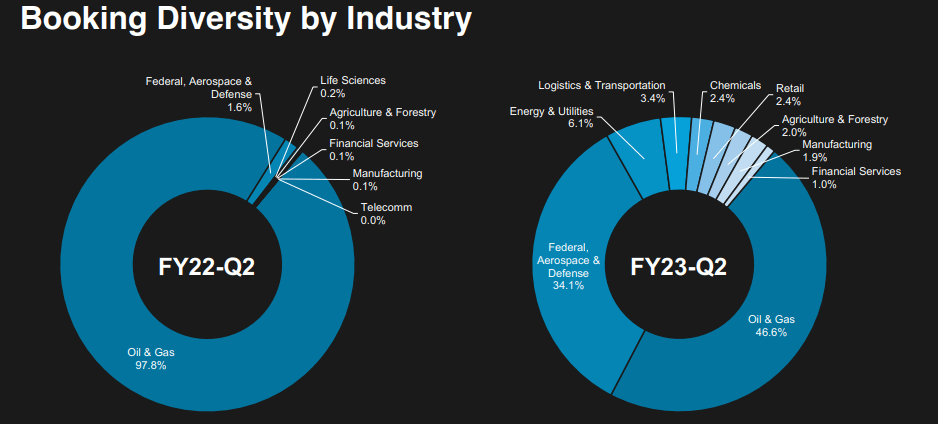

AI remains a promising proposition based on the growth of artificial intelligence. The company has historically seen the most success in the oil and gas sector, where Baker Hughes is its largest customer.

FY23 Q2 Presentation

AI’s sales approach differs greatly from other tech companies which in general sell a one-size-fits-all kind of product. Due to artificial intelligence having varying uses across different industries, AI typically seeks partnerships with top companies in each industry and earns commission revenue when those companies re-sell industry-specific applications of the product within their respective sectors.

In the current environment, investors have grown weary of unprofitable tech companies as the risks amidst a rising interest rate environment have overshadowed the potential reward. Management expects to retain at least $700 million of net cash by the time they achieve positive cash flow generation (as stated earlier, within 18 months). Management reminded analysts on the conference call that they could “turn this to be cash positive and profitable honestly within 90 days… All I got to do is layoff about 40% of the workforce.” Clearly, AI is not going to do this, but it is a worthwhile reminder to Wall Street that many of these tech companies are reporting operating losses intentionally as they aggressively invest in future growth.

As of recent prices, AI was trading at 9.5x sales. As we can see below, consensus estimates are pessimistic, with just 21% projected revenue growth in FY24 (versus management projections of at least 30%).

Seeking Alpha

That 9.5x sales multiple does not include the net cash making up 34% of the market cap. Assuming 25% revenue growth, 25% long term net margins, and a 1.5x price to earnings growth ratio (‘PEG ratio’), I could see AIT reading at 9.4x sales, seemingly supporting the valuation especially in light of the net cash position. That projected upside might increase if AI can execute against projections for 30% growth and positive cash flow. But I must admit that this recent rally seems to be meme-driven as AI is trading richly as compared to tech peers like Okta (OKTA) without clear reason other than the fact that it has a fancy stock ticker.

What are the key risks? A lot of this investment thesis lies on trusting management to be able to execute against accelerating growth rates back to the 30% range. Sure, the valuation is already pricing in material disappointment, but cheap can always get cheaper and the stock might sell off if management continues to disappoint on guidance. AI is competing against formidable competitors like Palantir (PLTR) and Microsoft (MSFT) to name a few – in the current macro environment it is possible that customers might prefer to work with more well known providers. Even if AI meets its guidance of positive cash flow generation by FY24, that would be on a non-GAAP basis and investors may still be subject to dilution until the company officially reaches GAAP profitability. I have discussed with subscribers to Best of Breed Growth Stocks that I have chosen a portfolio of undervalued tech stocks as my preferred approach to take advantage of the tech stock crash. AI is highly representative of a stock fitting in such a portfolio as it offers an attractive combination of secular growth and reasonable valuation. I caution though that the near term may see the stock trade with equal volatility downwards as it has upwards over the past few weeks – this is not a stock for those looking to sleep well at night.

Be the first to comment