Robert Way/iStock Editorial via Getty Images

Introduction

Audi is one of the high end brands for Volkswagen (OTCPK:VWAGY) and Audi’s 2021 annual report shows 1,680,512 vehicles sold worldwide. Toyota’s (TM) luxury brand, Lexus, sold 760,012 vehicles in 2021. YangWang is BYD’s (OTCPK:BYDDY) new premium brand and it does not appear to be made for wide audiences like Audi and Lexus. My thesis is that the first few vehicles from YangWang are meant for a somewhat narrow range of customers.

We see the YangWang U8 SUV and the YangWang U9 supercar in a January 7th tweet from @BYDCompany:

YangWang models (@BYDCompany tweet)

At the time of the writing, 1 RMB is about $0.15.

The Numbers

Jalopnik reports that the YangWang U8 and U9 will start at about ¥1 million each or a little over $146,000. YangWang would attract a larger customer base if they had offerings in the range of $50,000 to $125,000.

CnEVPost reports that YangWang vehicles will be able to adjust to a tire blowout and they’ll be capable of emergency floatation:

This also gives the vehicle greater safety redundancy, such as the ability to adjust the torque of the remaining three wheels at a rate of 1,000 times per second after a single-tire blowout, helping the driver bring the vehicle to a stable and controlled stop. Models equipped with e⁴ technology have IP68-rated protection for their core systems and can gain emergency flotation and extrication capabilities with four-wheel independent vectoring, according to BYD.

This is cool technology but a limited number of customers are making buying decisions based on these factors.

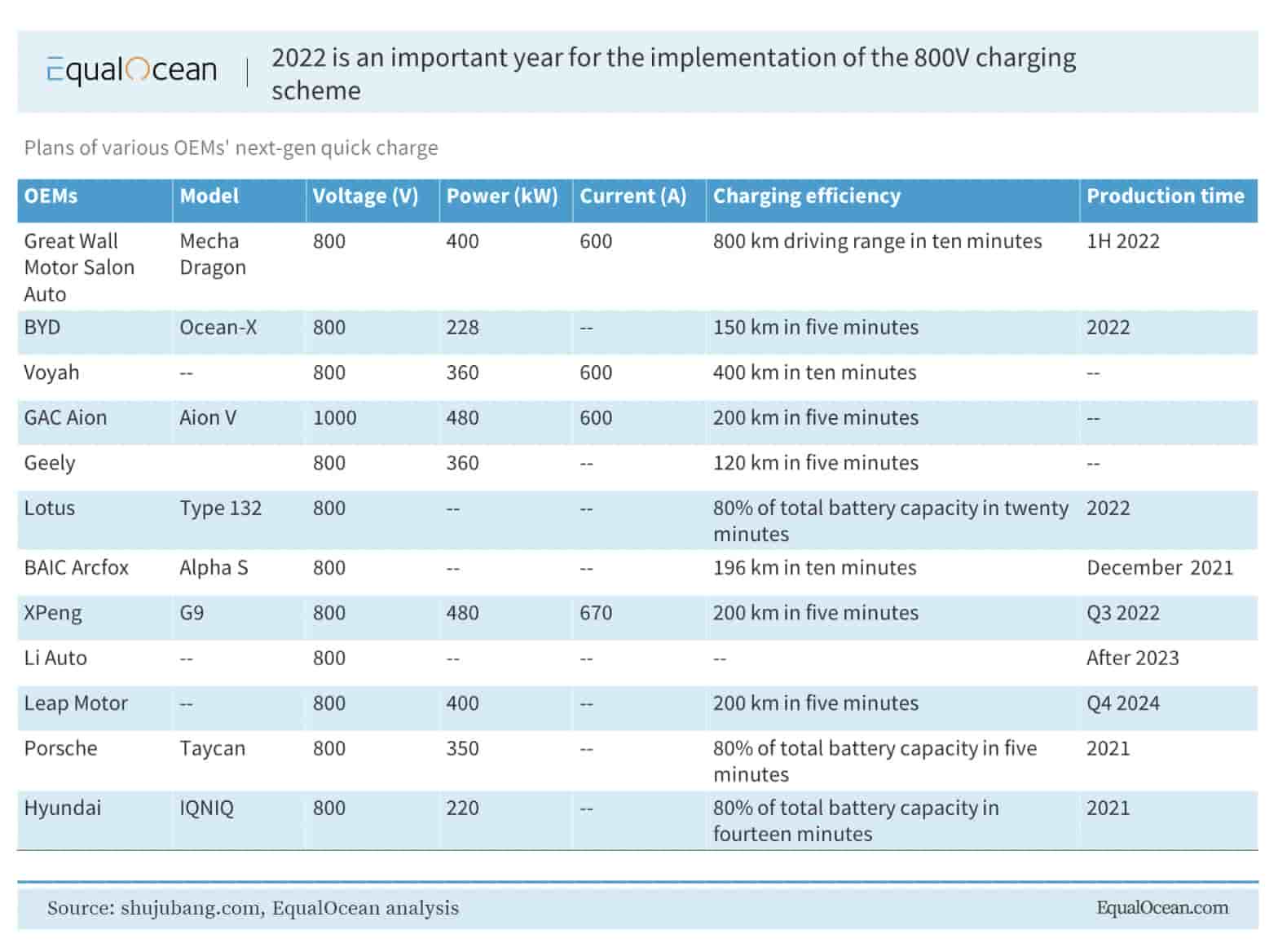

One of the problems with battery electric vehicles (“BEVs”) is that charging can take a long time. I drive a Tesla (TSLA) Model Y and I’ve always assumed that one of the reasons Tesla is perceived as a high end brand in the US is because their vehicles and superchargers have more charging efficiency than what we see with other options out there. We see below that companies like XPeng (XPEV) are improving charging efficiency with 800-volt batteries and new supercharging facilities. Per EqualOcean’s 800-volt list below, the XPeng G9 can add 200 km of range to its 800-volt battery from just a 5 minute charge! Many customers are willing to pay extra for this type of fast charging. Like the XPeng G9, some BYD models also have 800-volt batteries but the charging efficiency is 150 km in 5 minutes which is not as good as the XPeng G9. I thought we might see significant announcements about charging efficiency from YangWang but that hasn’t happened yet:

charging efficiency (EqualOcean)

BYD Stock Valuation

The 1H22 interim report shows gross profit of RMB 20,342 million on revenue of RMB 150,607 million for a margin of about 13.5%. The 3Q22 report shows that 9M22 revenue was a prodigious RMB 267,688 million which was more than 84% higher than the 9M21 revenue of RMB 145,192 million. I don’t see 3Q22 gross profit at a glance in the 3Q22 report but 3Q22 revenue was RMB 117,081 million and DigiTimes reports that the 3Q22 gross margin was 19%. This gels with the RMB 22,199 million 3Q22 quarterly gross profit we see reported at yahoo finance.

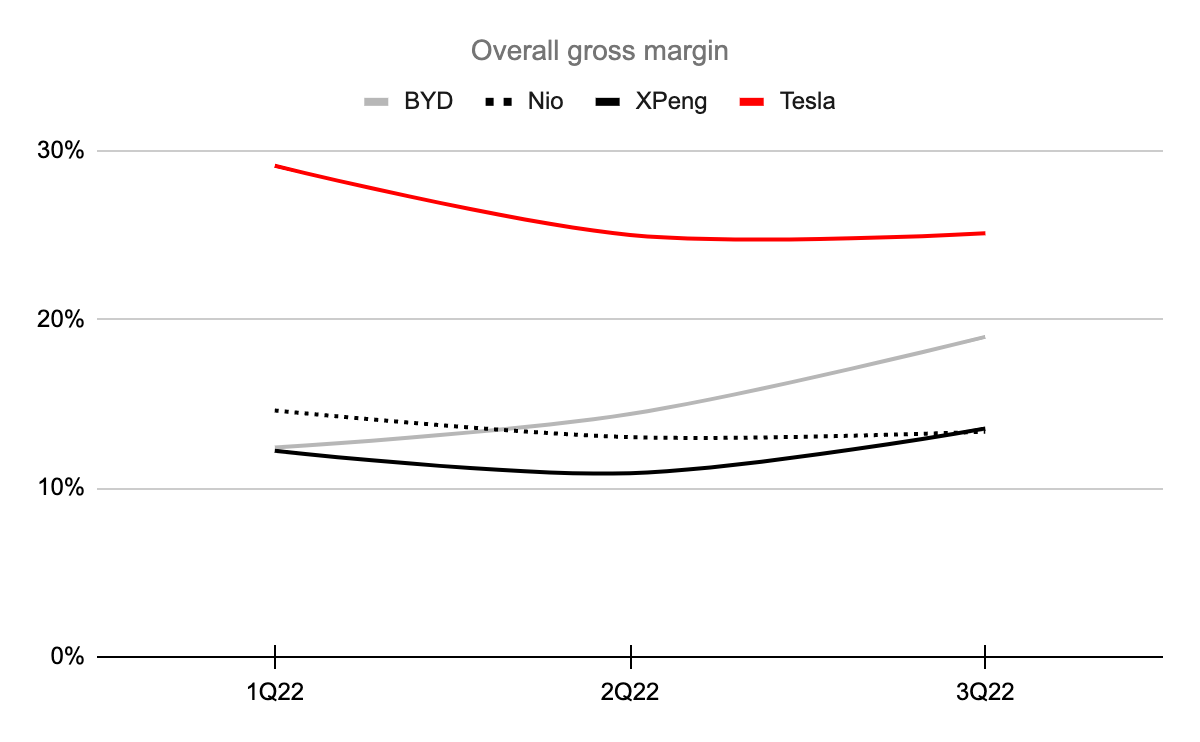

Looking at 2Q22 and 3Q22, BYD has a higher gross margin than competitors like XPeng and NIO (NIO) but a lower gross margin than Tesla:

BYD gross margin (Author’s spreadsheet)

Including PHEVs, BYD sold more overall vehicles than Tesla in 2022 but Tesla delivered 1,313,851 BEVs while BYD sold 911,140. The gross margins above and the higher average price of Teslas are some of the reasons why BYD’s 9M22 gross profit of RMB 42,541 million [RMB 20,342 million from 1H22 plus RMB 22,199 million from 3Q22] or $6 billion was far less than Tesla’s 9M22 gross profit of $15.1 billion. Tesla’s market cap as of January 6th was $357 billion based on the share price of $113.06 and the 3,157,752,449 shares outstanding as of October 18th in the 3Q22 10-Q.

BYD’s valuation is equal to the amount of cash that can be pulled out of the company from now until judgment day. We have to look at much more than gross profit when determining such a range but many of the income statement numbers below the gross profit line have unpredictable elements for the years ahead. I think BYD could be worth up to $100 billion but this is a low conviction estimate.

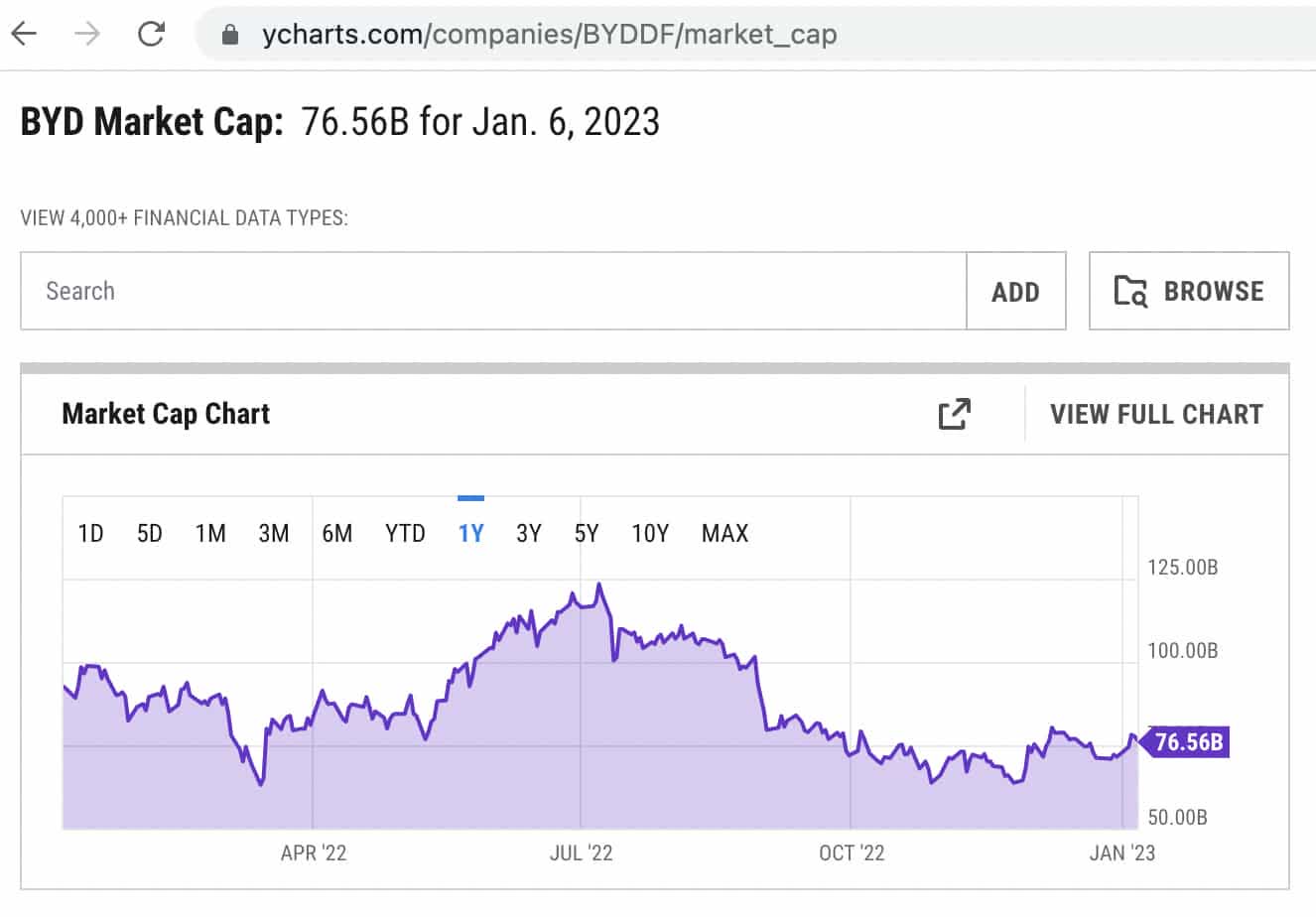

2 BYDDY ADRs represent 1 regular share. Looking at the January 6th BYDDY ADR price of $52.50, we get a market cap of more than $76 billion by multiplying this times the 2,911,142,855 combined shares from the 2022 interim report and dividing by 2. This figure is in line with what we see at YCharts:

BYD market cap (YCharts)

I’m not sure why the above figure differs from the January 6th yahoo finance market cap of $97.4 billion.

Forward-looking investors should keep an eye out for new announcements about BYD’s YangWang business, particularly with respect to charging efficiency improvements. Also, the upcoming 2022 annual report should be studied deeply in order to have a better understanding of what the economics should look like in the coming years.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment