Torsten Asmus

By Antoine Bouvet

Recession risk will make euro bonds investable again

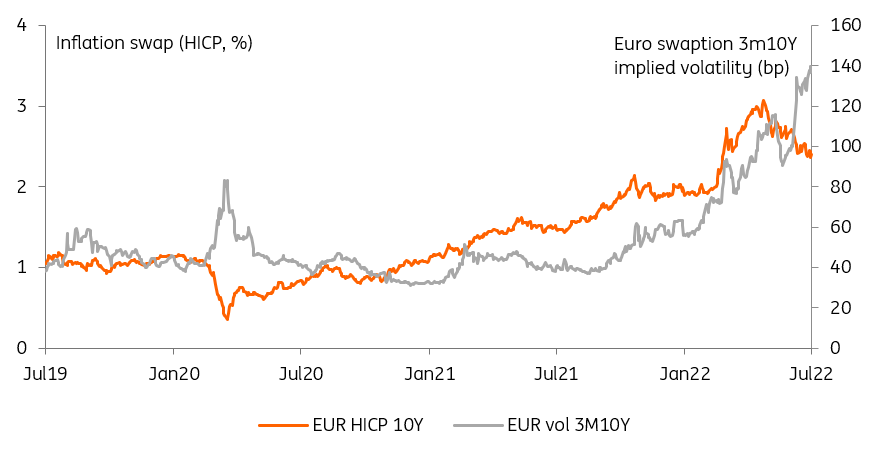

Choppy trading conditions in euro rates should not distract from the bigger picture: a recession is coming and rates should be moving lower. What higher volatility and poor liquidity conditions illustrate is a low level of conviction among participants. A dip in inflation swaps and greater angst priced across risk assets show that a recession in the eurozone is quickly becoming the consensus view. With that, we expect Bund and other core government bonds to regain their safe-haven status.

Volatility is deterring investors from taking advantage of lower inflation worries

With greater confidence about the path of the economy, we expect participation in rates markets to increase progressively. This means that, as rates settle into a lower range, investors and other market participants will increasingly feel it’s safe to dip a toe back in. This will go some way towards restoring the market’s ability to absorb large size trades, and result in lower volatility.

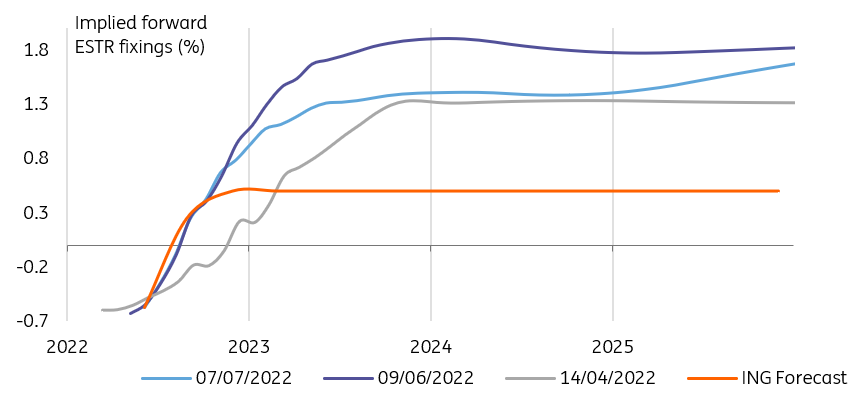

Only halfway through the re-pricing lower in front-end rates

The risk to this view is, of course, inflation. In an era of exceptional uncertainty about price dynamics, it is understandable that markets oscillate between competing views. One where the looming recession would bring inflation down with it, and one where inflation slows but fails to go back to target, thus requiring further monetary tightening down the line.

The curve has converged to our ECB view, but still has some room to drop

We’re decidedly in the former camp. Our economic monthly is part of the increasing chorus warning about recession risk, and our view of a much shallower ECB tightening cycle reaching only 100bp is gaining in popularity. At its peak, the swap curve implied roughly 300bp of hikes by end-2023, this is now down to under 200bp, so we are roughly halfway through the adjustment lower at the front end of the curve. The reality dawning on markets is that the ECB is so far behind the curve, it is starting to look like it’s ahead of the curve. Delays in hiking and a window of opportunity closing fast means our call for 100bp of tightening could even prove too optimistic.

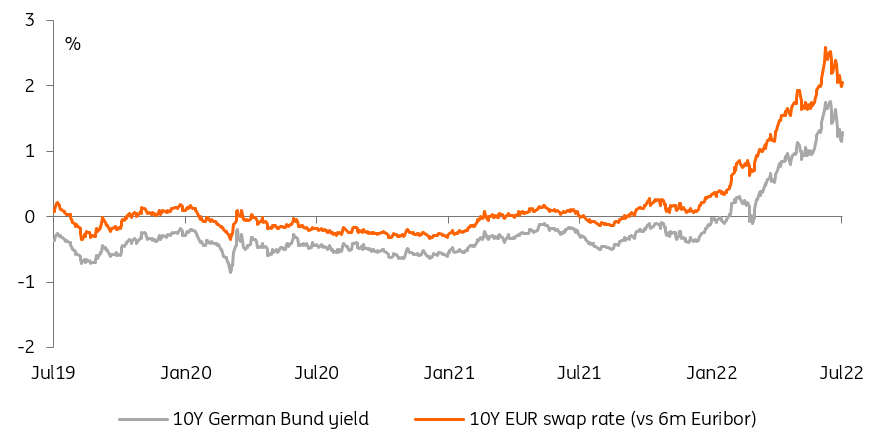

Lower rates by mid-2023, but beware summer volatility

We’re expecting 10Y German Bunds to trade around the psychologically important 1% level by this time next year. This is still 50bp above where we think the ECB deposit terminal rate will be at the time, which is a generous term premium premised on the return of economic optimism. Translating this into 10Y swap rates, a tightening in swap spreads from their currently stretched levels means the drop in rates will be even more noticeable, to 1.5%. The main difference between now and then is that we expect trading conditions to improve materially, also resulting in a positive feedback loop to other markets priced off interest rates.

10Y German yields and euro swaps will move lower into mid-2023

The near-term situation is murkier. The stretch of time between now and the autumn, when the looming recession and energy crisis can no longer be ignored, has the potential to see further jumps in rates and yields. Summer trading conditions could see liquidity deteriorate further still, and a hawkish Federal Reserve could push Treasury yields, and euro rates, higher temporarily. Double-digit daily changes in yields could still be with us for some time, but with lower rates come healthier trading conditions.

Content Disclaimer

This publication has been prepared by ING solely for information purposes irrespective of a particular user’s means, financial situation or investment objectives. The information does not constitute investment recommendation, and nor is it investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument. Read more.

Be the first to comment