_ultraforma_/E+ via Getty Images

U.K. commercial property developer and landlord British Land (OTCPK:BTLCY) has had a rocky couple of years. I expect ongoing troubles in the U.K. economy to mean the road ahead may also be rocky. However, a share price fall means that the company now looks more reasonably valued than before, although I will not be buying as I think the U.K. stock market offers other far more interesting opportunities right now.

My last piece on the company was in June 2021 (British Land: Still Overvalued), in which I was bearish on the basis that it faced ongoing challenges and looked overpriced to me. Since then the shares have fallen 33%. I had noted in that piece that the company had cut its dividend, but the share price fall means that it now yields 6.3%.

The Long-Term Demand Environment Looks Good to Me

The new prime minister in the U.K. and her chancellor have already messed things up royally in the City, in my view, sending many British stocks into an even worse position than they were already in. As has been the case over the past few years, there is no shortage of negative headlines around the economic direction of travel for the U.K.

Take a walk around London, though (and to some extent smaller cities) and the reality does little to live up to the headlines, in my opinion. Things are vibrant, businesses are busy making up for lost time, and there is little sense that we’re going to hell in a handbasket so may as well abandon hope. I think the long-term demand for commercial property in the U.K. remains positive. So, for all the challenges the sector has faced over the past several years, I remain upbeat about the long-term outlook for the sector, within which British Land has a strong position.

Last year, the company already showed considerable recovery from the pandemic. That is pretty much what I would expect of a company like British Land. Although the pandemic delayed some rent payments, sent some tenants to the wall and imposed extra costs on the landlord, the long-term trajectory of the company looks broadly the same in my view: the pandemic did not change the fundamentals of the business.

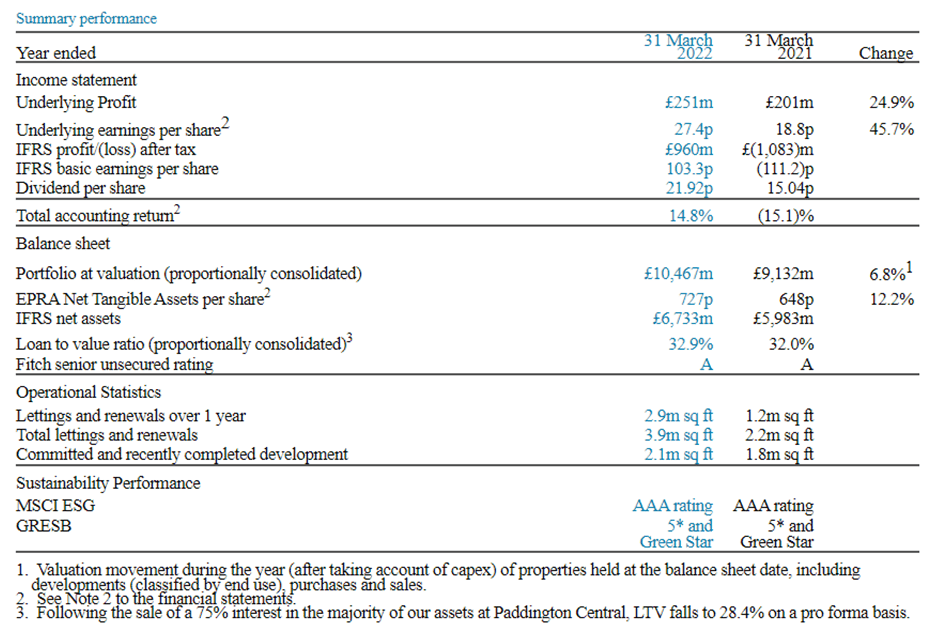

company announcement

The Dividend Yield is over 6%

The British Land dividend last year was only 71% of what it was back in 2019. In my 2020 piece British Land: Don’t Take The Dividend For Granted I explained that the company’s revised dividend policy could make the payout less consistent than before and may also lead to cuts. We have certainly seen that it is less consistent. Last year’s dividend was not a cut per se as it was substantially larger than the prior year payout. But the level remains far below what it was before the Covid-19 pandemic and I continue to expect that the dividend policy could mean cuts in future, depending on business performance.

For now, though, the dividend yield is 6.3% which I regard as attractive for a blue-chip property company of this calibre.

Valuation Looks Reasonable

Having lost a third since my bearish note suggesting they were overvalued, do British Land shares now offer good value? After all, the shares trade at a 52% discount to the EPRA Net Tangible Assets (NTA) value per share of £7.27. That makes them look cheap, but in reality, as the company will not be realising those assets any time soon that figure is not very helpful other than for investors with a very long timeframe.

Using the most recent full-year underlying earnings per share, the company trades on a P/E ratio of almost thirteen. Using the IFRS figure the ratio is dramatically different, at just over 3, but I think that is not useful as an indication of actual earnings that an investor can use to calculate value. Free cash flow last year was £75m before the payment of dividends. Once dividends are included, the firm saw a net cash outflow of £80m for the year. The market cap stands at £3.3bn.

I see limited upside from here. The company faces a number of challenges, such as a possible reduction in office demand and a weakening property market in the U.K. that could weigh negatively on future rental rates.

I think it can manage those challenges, but they do exist. The investment case here is also mixed, in my view. British Land is seen as fairly stable thanks to its portfolio of high-quality sites and the business model of long leases for commercial property. However, recent years have shown that that is no guarantee of consistency of results. While I like the current dividend yield, the lack of likely consistency in the dividend contrasts to other sectors in the U.K. stock market currently offering similar yields that I think are more likely in general to maintain or grow their dividends annually (tobacco and financial services being two examples).

I expect further turbulence in the U.K. property market and economy to dampen sentiment on British Land. I do not see the shares as a bargain.

However, for the strength of the business and a yield of over 6%, I see the current share price as fair value and am accordingly moving my rating back to “hold”.

Be the first to comment