sarkophoto

Introduction

I have written occasional articles here regarding BP Prudhoe Bay Royalty Trust (NYSE:BPT) for almost 10 years. In fact, my very first Seeking Alpha article, in January 2013, was “ BP Prudhoe Bay, A Derivative Security In Disguise” so I am now a few days short of my 10th anniversary as an author on this site.

At the time of my initial article in 2013, BPT was trading at close to $80/unit, and I warned that the structure of the Trust would cause it to terminate, likely prior to 2027, and that it was likely considerably overvalued.

The units are now trading in the $12 range and in fact BPT is still on track to possibly terminate prior to 2027, with total future distributions likely being considerably less than the current price. In fact, there is even a slight possibility that the payment to be made in January could be its final one. As a result of these factors, I reiterate my earlier warning.

BPT’s “Reason for Being”

BP Prudhoe Bay Royalty Trust was established in 1989 as a financial mechanism providing BP with part of the funding it needed to develop its portion of the massive Prudhoe Bay oil field in Alaska. As I explained in my 2013 article, it is best to view BP Prudhoe Bay as an unusually structured loan (or derivative security) rather than a direct ownership interest in the BP field. Like any public debt instrument, BPT has a corporate trustee but no employees as it is not a company.

BPT’s “Real” Vs. “Artificial” Calculation Factors

There are a number of factors which are used to calculate the quarterly distributions due to BPT unit holders. I discuss the three most important factors in this section, and the varying degrees to which they represent the underlying economics of Prudhoe Bay production versus being somewhat artificial factors.

One element of the quarterly payments due to BPT holders is based upon its legally allocated portion of Prudhoe Bay production. This is actually the only element in the calculation that is directly related to activity in Prudhoe Bay.

The second element, the realized price per barrel that BPT holders receive, is not directly dependent upon the price BP (or its subsequent investor, Hilcorp) receives for the oil. Instead, it is based upon a benchmark, the “West Texas Intermediate (WTI)” oil price, which is the actual price received for a somewhat different grade of oil delivered by others to a different location, the storage facilities in Cushing, Oklahoma. The actual price received by BP (and now Hilcorp) is slightly different and usually a bit higher.

The advantage of using WTI, a publicly available benchmark, is its transparency and convenience. In fact, if such a benchmark were not utilized in the calculation of quarterly distributions, I would not be able to provide as precise an estimate of the current quarter’s distribution as I am able to do in this article.

The third element, the Adjusted Chargeable Cost, is a completely artificial construct and has no direct relationship to the actual cost of Prudhoe Bay production. It is now increasing at a rapid rate, simply due to the formula that was established in the Trust agreement in 1989.

The Adjusted Chargeable Cost is calculated by multiplying the Chargeable Cost by a CPI (inflation) factor. For most of the first 30 years of the Trust’s existence, the Chargeable Cost increased by a very modest $.10 per year. However, in 2020, it began increasing by $2.75 per year. When multiplied by the current CPI factor, which is now well over 2, and increasing each year, the cost the Trust owners get charged per barrel is increasing by $6 or more per year, not including changes in production taxes (which will be discussed in a later section).

Over the years that I have been writing articles and reading comments from BPT investors, two very different themes seem to crop up. One theme is that the cost of production at Prudhoe Bay are likely decreasing due to technological advances, increased drilling efficiencies etc. making BPT an undervalued investment. This may, or may not be true, but is TOTALLY IRRELEVANT to the artificial and rapidly increasing cost the BPT holders are actually charged.

The other theme is that BPT holders being charged this high, rapidly increasing fake number is “unfair.” It’s actually perfectly fair. This factor is clearly disclosed in BPT’s financial statements. Investors should read and understand the structure of the Trust before buying units and only be willing to pay a certain price based upon this structure/factor. (“Read the fine print…” or at least my articles…)

To understand why it is fair, it is important to go back to my initial paragraphs and why BP established BPT in 1989; it was simply to raise money to develop the Prudhoe Bay oil field. Keep in mind that the structure of the Trust only allowed for the minor $.10 or so increase in the Chargeable Cost for most of the first 30 years of BPT’s existence. Then in its 31st year (2010) the rapid increases began.

BP didn’t want to have this entity lingering forever along with all of its associated expenses, reporting etc. and therefore structured the Trust so that it would likely go out of existence not too long after the 30th anniversary of its creation. Just as importantly, if BPT had been structured to last much longer than 30 years, investors buying the units from BP when they were first issued in 1989 would likely not have paid appreciably more in the initial offering price; BP had no financial incentive to make the Trust life more open-ended than 30 years+. If it had been structured to go out of business after 15 or 20 years, however, BP would have likely had to sell the units for somewhat less.

My Q4 Model

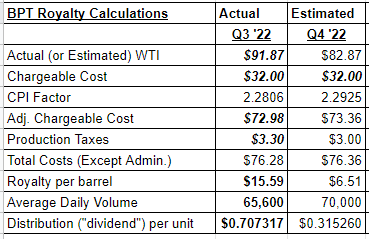

Over the years, I have developed (and refined) a model to project upcoming payments and occasionally also estimate the possible intrinsic value of BPT units. I have presented below BPT’s actual results for Q3 2022 along with my estimate for Q4:

Company Reported Figures and Author’s Estimates

BPT generally reports summary results less than one week after the end of each quarter, so we will likely see the most recent quarter’s summary results this coming Friday. Full results are not reported until the subsequent 10-Q or 10-K is filed, which results in a substantial lag. Because the payment in October is considered a Q4 event, even though it is based upon Q3 results, the details will not be fully available until BPT files its 10-K for 2022 in March.

The timing issue used to be a major one, as BPT’s Trustee, The Bank of New York-Mellon, used to only report the average daily volume and the distribution amount in its summary results. It now reports most of the key factors, which are the figures in bold in the actual column above from its Q3 press release dated October 7, 2022. The two figures not in bold were easily calculated from the figures which were reported.

My estimate of Q4 is mostly based upon my estimate of appropriate, generally minor, adjustments to the Q3 actual figures. For example, the CPI figures BPT utilizes is based upon the difference between the mid-month of a prior quarter (in this case August) and the mid-month of the most recent quarter (in this case November). Although the headline y-o-y government reported CPI increases are still quite high, the actual increase from August to November is considerably more modest.

The one major change (decrease) from Q3 is the decrease in the average WTI during the quarter, which based upon my estimate, went from $91.87 to about $82.87. I utilized the EIA reported figures (monthly averages for October and November, and average of the December daily figures through December 27, the most recent currently available) to estimate WTI for Q4. With my estimate of total costs being very similar in both Q3 and Q4, in both cases close to $76.30, the profit per barrel likely decreased by almost 60%.

I am estimating that the average daily production was 70,000 barrels per day in Q4 (of which BPT holders receive credit for 16.4246%), compared 65,600 in Q3. The State of Alaska reports Prudhoe Bay oil “production”, including that from various satellite fields, on a daily basis. BPT holders are only entitled to its proportion of the oil from the “participating area” of Prudhoe Bay but the state’s daily reporting does not include a breakdown of volumes for this specific area.

As a result, I use as an approximation the percentage change in production from a couple of the prior quarters, specifically the same quarter of the prior year (Q4 2021) and the immediate prior quarter (Q3/”summer” 2022). Total Prudhoe Bay production in Q4 was about 98.5% of the volume for the prior year’s 4th quarter and about 105% of the summer quarter’s volume. (Summer volumes are typically lower due to pipeline maintenance.) When I multiply BPT’s reported numbers by these percentages, I come up with volumes in the 69,500 to 70,500 barrels per day range, and therefore chose 70,000.

Finally, to arrive at my estimate of about 31.5 cents for the 4th quarter, I multiplied the Q3 figure of $.707317 by the changes in royalty per barrel and changes in volumes from Q3 to Q4. ($.707317 x $6.51/$15.59 x 70,000/ 65,600.)

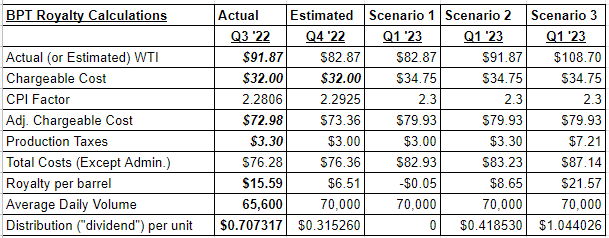

Some Q1 2023 Scenarios

I have expanded the above table by providing three possible scenarios for the Q1 2023 distribution based upon varying WTI prices:

Company reported Figures and Author’s Projections

On January 1, the Chargeable Cost increased by $2.75 to $34.75 per the Trust Indenture, while I am projecting the CPI factor will increase by a minor amount as well, which means the Adjusted Chargeable Cost (prior to production taxes) is likely now almost $80.

I have subjectively chosen three different WTI prices in the scenarios. The first one is utilizing the actual average WTI price I have estimated for Q4; $82.87. It indicates that there would be no distribution in Q1 (WTI would need to be 5 cents or so higher for the Trust to even breakeven.) As I write this, however, WTI is currently a couple of dollars lower, so it would have to increase somewhat this quarter for there to be any distribution in April.

“Scenario 2” utilizes the same WTI as the actual figure for Q3 ($91.87) while “Scenario 3” utilizes the actual WTI for Q2 ($108.70). I chose these prices partly to show the impact of the annual increase in Trust costs on the distributions. At $91.87 the distribution in Q3 was over $.70 while at the same price this quarter, it would be less than $.42. At $108.70, it decreases from $1.40 to $1.04. For anyone who doesn’t want to do complicated math or wants to look at their own preferred scenario, the distribution generally increases by $.04-$.05 per unit for each dollar that WTI increases, assuming all other factors remain the same.

Another major reason I chose these WTI prices is to highlight the impact of Alaska’s oil production tax on distributions. The tax was only $3.30 per barrel at WTI of $91.87 in Q3 but was more than double that amount, at $7.21 the prior quarter when WTI averaged $108.70. The tax formula is somewhat complicated with credits for various costs of production, but when oil prices/profits get above certain levels, the marginal rate becomes as high as 35%. A document explaining some of this is available here.

Further complicating the issue is that, as I have always emphasized in my articles, BPT is an artificial construct/derivative security. As a result, the production tax payer is not BPT, but rather Hilcorp (and previously BP), the legal owner of the interest in Prudhoe Bay’s oil. In turn, there are tax agreement letters between BPT and Hilcorp regarding the tax per barrel deemed fair to charge BPT unit holders. These documents have been provided in past BPT SEC filings. However, I am not providing a link to these documents for two reasons. First, I can’t locate the documents at the moment. Secondly, I am not confident I could correctly interpret the legalese in these letters in any case, and ultimately the most important takeaway is that it appears that at oil prices above about $100, BPT’s marginal production tax rate starts to approach 35%.

This 35% tax rate is important because it means that at higher oil prices, $3.50 of each $10 increase in WTI likely goes to the State of Alaska rather than BPT holders. Combining this with the Adjusted Chargeable Cost now increasing annually by at least $6-7, anyone doing even “back-of-the-envelope” calculations should realize that WTI must increase by about $10 per year just to keep the distributions the same.

A Few Final Thoughts

I suspect there are some oil bulls who will tell me that WTI will likely increase by considerably more than $10 per barrel per year and therefore BPT distributions are on a trajectory to increase rather than the Trust possibly terminating soon. They could well be right. However, if that turns out to be the case, there are likely much better investments in the oil patch than BPT, which gets hit with artificially high and rapidly increasing costs.

It is also clear that BPT’s unit price reacts to both “perceived yield” based upon the most recent distribution announcement and daily changes in WTI, making this an extremely tricky investment. On the one hand, “perceived yield” will plummet by more than 50% when the Q4 distribution is announced, likely on Friday afternoon. On the other hand, predicting short term moves in WTI and various other oil benchmarks is a “fool’s game.”

On the short side (as I am currently am), the risks are even higher due to borrowing costs which are now about 15% annualized (although insignificant in dollar terms for a short term trade) and the possibility of a short squeeze, which could cause the annual borrowing rate to suddenly skyrocket or even a broker to require a position be closed because there are no units available at any borrowing cost. As a result, I would strongly caution against other investors doing what I am doing, but I would suggest that longs who are oil bulls consider reallocating their oil investments into a stock that has brighter prospects.

Be the first to comment