Dilok Klaisataporn

When it comes to companies that rely on government pay, defense contractors like Lockheed Martin (LMT) or Raytheon (RTX) may come to mind. While those are fine companies, it shouldn’t be ignored that they are highly capital-intensive businesses due to their manufacturing component.

This brings me to the asset-light company, Booz Allen Hamilton Holding Corporation (NYSE:BAH) which provides consulting services for the government, and which may be a good diversifier for portfolios that are heavy on manufacturing companies.

BAH is one of an elite club of stocks that’s actually posted a positive return over the past year, while the S&P 500 Index (SP500) is down by 20%. In this article, I highlight what makes BAH a worthy holding for reliable growth, so let’s get started.

Why BAH?

Booz Allen Hamilton is a global consulting firm that’s strategically headquartered in McLean, Virginia. It was founded in 1914, and today consults primarily government agencies (civil and defense) and, to a lesser extent, private sector companies as well. BAH’s government focus means that it’s rather resilient to economic downturns.

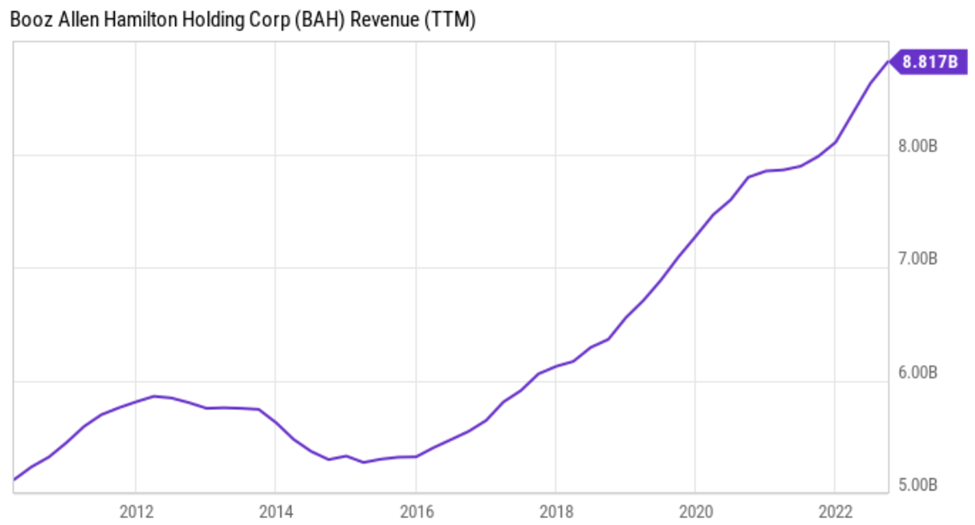

One of the key drivers of Booz Allen’s success has been its focus on innovation. The company has a strong track record of developing new solutions to complex problems. This has helped it to stay at the forefront of its industry and attract top talent. As shown below, BAH has kept a rather solid revenue trajectory over the past decade, without experiencing a downturn during the recession in 2020.

BAH Revenue (YCharts)

Also, BAH is a cash-rich business due to people costs being its primary expense. This has enabled more capital returns to shareholders through dividend increases and share buybacks. This, combined with the growing nature of its business has resulted in market-beating returns. As shown below, BAH’s total return of 910% over the past decade has thumped the 217% return of the S&P 500.

BAH Total Return (Seeking Alpha)

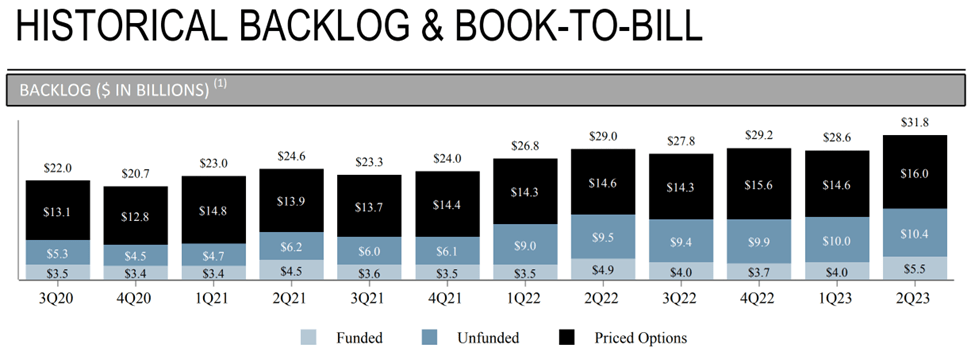

Meanwhile, BAH continues its impressive trajectory, with revenue excluding billable expenses growing by 10% YoY to $1.6 billion in its fiscal second quarter. This was driven by growth across all of BAH’s key markets, including 18% growth in the Civil business and 9% growth on the Intelligence side. Looking forward, BAH looks set to build upon its momentum in the upcoming quarters, as its backlog of $31.8 billion currently sits at its highest level over the past 3+ years, as shown below.

BAH Backlog (Investor Presentation)

Management’s growth strategy revolves around what it calls VoLT, which stands for velocity, leadership, and technology. This is a multi-year initiative with the aim of growing adjusted EBITDA to a range of $1.2 to $1.3 billion by the year 2025. It appears to be currently on track, as it generated $935 million in adjusted EBITDA in fiscal year 2022 (ended in March 2022).

Although BAH has no shortage of programs to work on, one potential headwind could be a tight labor market, which may result in higher salaries to attract talent. Nonetheless, BAH was still able to grow headcount by 4.2% over the past 12 reported months amidst a very competitive labor market, with strong absorption of new hires into billable programs.

Moreover, BAH is set to benefit from geopolitical instability and plans to accelerate its National Cyber business, as noted during the last conference call:

We are pleased to have closed on the acquisition of EverWatch. We’re excited about the opportunities EverWatch creates to accelerate our National Cyber business. Our clients live in an increasingly complex environment, pressured by geopolitical instability, global challenges for pandemics to climate change and the increased need to invest in new technology, while at the same time sustaining legacy programs, all in a fraught political and economic environment.

We believe we are uniquely positioned to use innovation to simultaneously help our clients navigate these complex challenges and drive our own financial performance. Our basic premise is that technology cycles come in waves that are growing in both amplitude and frequency.

Importantly, BAH maintains a strong balance sheet, with a net debt to TTM EBITDA ratio of 2.47x. While its dividend yield of 1.7% is the same as that of the S&P 500, it’s grown at a much faster rate, with a 5-year CAGR of 20%, comparing favorably to the 5.7% 5-year CAGR of the S&P 500.

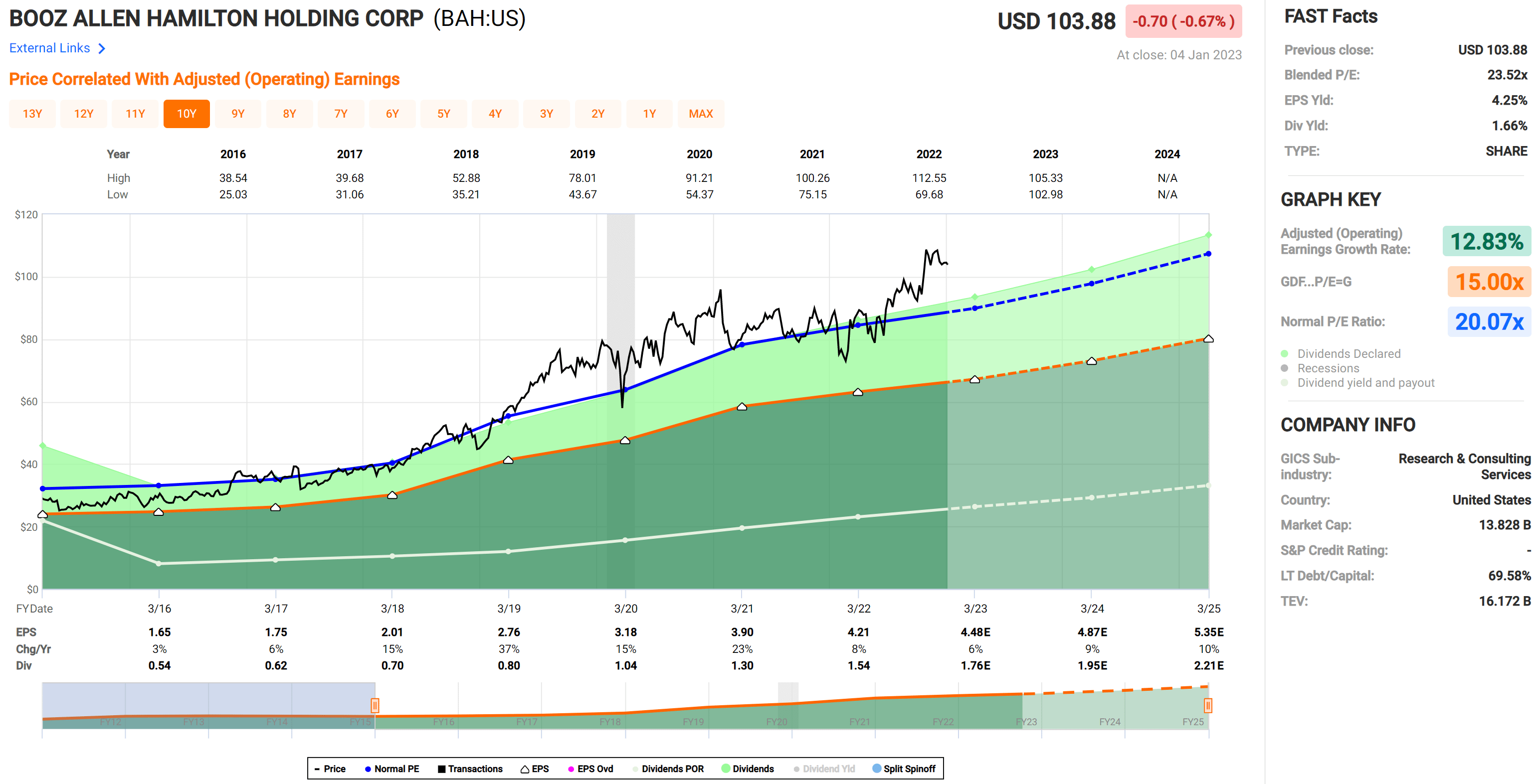

Turning to valuation, BAH doesn’t scream cheap at the current price of $104 with a forward P/E of 23.2, sitting above its normal P/E of 20 in recent years. Given these considerations, I think patience is warranted and a pullback to the ~$95 level would make the stock more appealing.

BAH Valuation (FAST Graphs)

Investor Takeaway

BAH has been a great wealth compounder for long-term investors, with returns far surpassing the S&P 500. The company has strong fundamentals, including a strong balance sheet and an ever-growing backlog. Management is also executing well on its VoLT growth strategy, and it looks set to continue benefiting from geopolitical instability.

However, Booz Allen Hamilton Holding Corporation stock isn’t cheap at current levels, and thus, investors should wait for a pullback before initiating a position. Nonetheless, investors who do decide to hold BAH over the long term could be rewarded with attractive returns from this industry-leading company.

Be the first to comment