andersdahl65/iStock via Getty Images

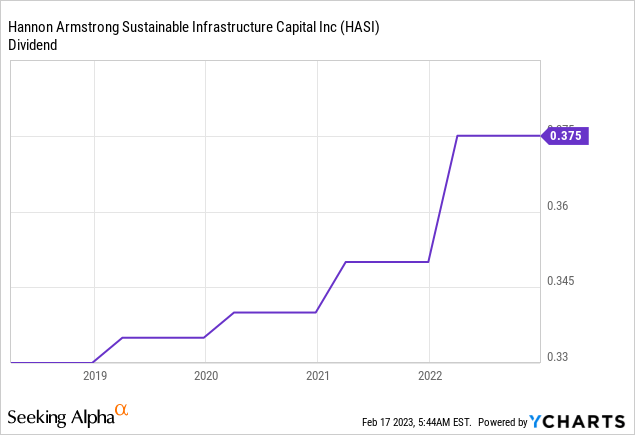

Hannon Armstrong (NYSE:HASI) just raised its quarterly cash dividend by 5.3% to $0.395 per share, for a 4.5% yield against the current price of the commons. The raise came on the back of what had been a torrid few months of trading with Hannon Armstrong under pressure from a short report, rising Fed fund rates, and broader supply chain issues that had affected the green economy. Hannon Armstrong essentially functions as a provider of capital to assets developed by climate economy companies from energy efficiency, renewable energy, and sustainable infrastructure markets.

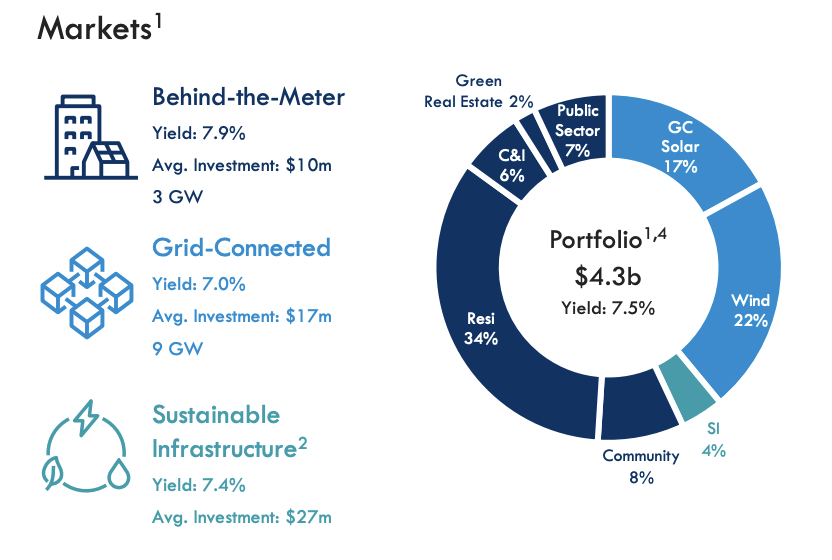

The internally managed mortgage REIT’s portfolio as of the end of its most recently reported fourth quarter stood at $4.3 billion, up by 19% over the prior year with an average yield of 7.5%. Critically, Hannon Armstrong forms a uniquely placed and rare mREIT operating in a space that is set for material growth. The energy crisis, Russia’s war in Ukraine, and US government subsidies have supercharged the transition to green energy to create the backdrop for what should be immense opportunities for Hannon Armstrong to expand its investment pipeline and the overall vivacity of its average yield on investments. The latter faces headwinds from rising Fed funds rates and is stalked by the specter of a recession.

Hannon Armstrong’s stock is up 23% year-to-date to take part in a broad market rally sparked by a possible dovish pivot by the Fed. I believe this dynamic will continue to drive near-term returns even as the relevant financial metrics continue to come in strong in future quarters. The income here is what matters in the interim and its ascent over the last few years has been sustained.

Not including the most recent raise and the quarterly dividend is still up by a 3.83% compound annual growth rate (CAGR) over the last three years, a figure which increases to 7.14% over the last 12 months. The bull case is now built on the REIT building on its fast-expanding investment pipeline to ramp up EPS and dividends at pace over the medium to long term.

A Revenue Beat And Double-Digit Growth In Distributable EPS

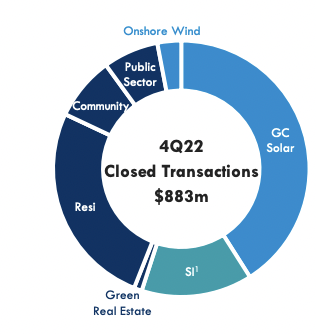

Hannon Armstrong reported revenue of $58.3 million for its fiscal 2022 fourth quarter earnings, this was up by 8.6% from $53.4 million in the year-ago comp and was a beat by $23.22 million on consensus estimates. This growth was driven by $883 million in closed transactions during the quarter. It also formed nearly half of the total investments made in the full fiscal year with Hannon Armstrong’s management flagging a rapid expansion of their investment pipeline during their earnings call.

Hannon Armstrong

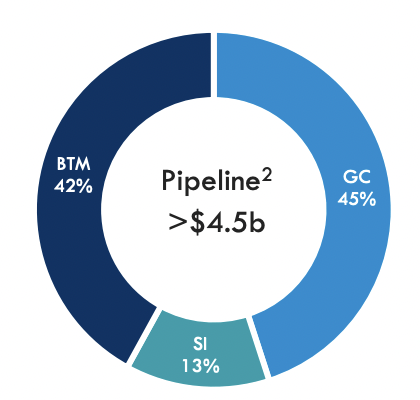

Transactions during the fourth quarter were closed at an average yield of just above 8% with volume building up as more certainty is derived on the investment and production tax credit impacts of the Inflation Reduction Act. The REIT’s investment pipeline, or transactions that have the potential to close over the next 12 months, stood at $4.5 billion as of the end of the fourth quarter.

Hannon Armstrong

This will continue to see an almost even portfolio split between grid-connected and behind-the-meter investments with sustainable infrastructure coming in at 13%. The respective yields of these markets are broadly similar but they of course offer different dynamics.

Hannon Armstrong

This portfolio forms the foundation of future shareholder value and its growth is now backstopped by the most ambitious piece of green energy legislation in US history. This will be further supported by what looks to be a robust response to the energy crisis sparked by Russia’s war in Ukraine.

Providing Capital To The Climate Economy

Hannon Armstrong realized distributable EPS of $0.47 during the fourth quarter. This missed consensus of $0.49 and was unchanged from the year-ago figure, albeit down from the prior third quarter by $0.02 per share. This was on the back of fourth quarter interest income of $36.8 million, a growth from $30.5 million in the year-ago period. The company’s earnings call was a mix of jubilant and sombre with the growth opportunities flagged by management set against the EPS miss during the quarter. The EPS decline was driven by project-level mark-to-market losses on power price swaps. Essentially, the swaps incurred non-cash unrealized losses as energy prices rose. The subsequent increase in project value does not show up in the GAAP numbers.

Hannon Armstrong is guiding for distributable EPS to grow at a CAGR annual rate of 10% to 13% from 2021 to 2024 with distributable EPS of $2.08 for the full year 2022. This was a growth of 11% over fiscal 2021 with distributable net investment income growing by 34% year-over-year to $180 million. However, whilst I retain a position, I’m rating the stock as a hold because whilst fixed rate debt accounts for 86% of their borrowings, floating rate borrowing at 14% leaves the mREIT exposed to further rate increases which might induce more near-term volatility as we get through this macroeconomic environment.

Be the first to comment