Sundry Photography

Bloom Energy (NYSE:BE) is amidst a global decarbonization journey ramping up to deliver outsized opportunities to the San Jose, California solid oxide fuel cells manufacturer. The technology, use case, and future momentum is strong. Bloom’s solid oxide technology converts natural gas or biogas into electricity without combustion. These solid oxide fuel cells merge to form fuel cell stacks which are placed into independent modules. These modules are aggregated to form what Bloom describes as a modular Energy Server platform whose demand is being driven by corporations looking to reduce their carbon footprint and build enhanced resiliency into their operations. Bloom’s fuel cell differs from competitors like Plug Power (PLUG) in that it doesn’t require an expensive catalyst like platinum.

The company counts Equinix, Home Depot, and FedEx as part of a growing list of US and international customers whose fuel cell adoption momentum is being driven by a multitude of factors. Important is downstream consumer demand for companies they buy from to take sustainability into greater regard. Aggressive efforts by global policymakers from decarbonization targets to financial incentives are also driving this growth. For example, the US Inflation Reduction Act, described as a “game changer” by Bloom’s founder CEO KR Sridhar, will provide several relevant production tax credits including a tax credit for biogas equipment and support for US-based manufacturing sites.

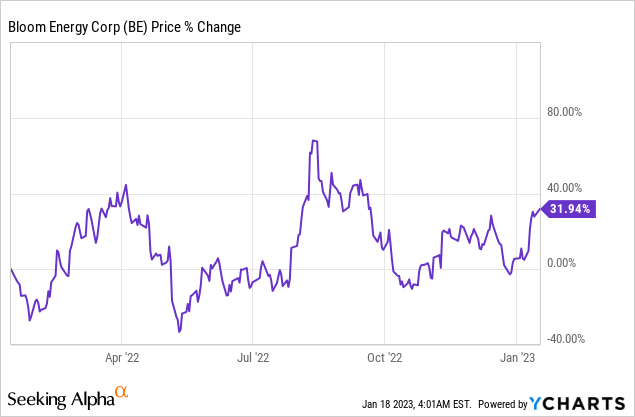

The enthusiasm is clear as in a year when the stock prices for growth stocks and the broader climate economy retrenched materially, Bloom notched a return of 32%. Close comparable peer ITM Power (OTCPK:ITMPF) is down 74% over the same period. 2023 could promise more relative outperformance as the IRA ramps up to boost a business that’s executing ambitious growth plans.

US-Based Manufacturing As Fuel Cell Production Ramps

Bloom’s multi-gigawatt manufacturing plant in Fremont, California was opened just last year in July. The 164,000 square foot facility cost $200 million to build and should help drive the next phase of IRA-derived growth in 2023. The company is chasing harder to decarbonize industries from fertilizer to steel and cement making. Sales are booming, with Bloom last reporting earnings for its fiscal 2022 third quarter that saw revenue coming in at $292.3 million. This was an increase of 41.1% over the year-ago period and a beat of $17.38 million on consensus estimates.

Growth was driven by continued demand from companies in the industries Bloom serves and on the back of the expansion of its manufacturing capacity. Bloom is targeting a broad basket of industries from Data Centers, Chemicals, and Utilities. The Bloom Energy Server platform is really quite applicable to most industries as the creation of electricity closer to where it’s used through a fuel cell versus combustion generates significantly less carbon and other harmful gases like nitrogen oxide and sulfur oxide.

Gross profit at $50.9 million was an increase from $37 million in the year-ago quarter and came on the back of non-GAAP gross margin of 19.1%. This was broadly in line with the year-ago comp of 19.2%. The growth story here is that continued demand will ramp higher with the IRA as the Fremont facility drives healthy year-on-year comp for the coming quarters. Bloom expects revenue for its full fiscal 2022 to be between $1.1 billion to $1.15 billion with non-GAAP gross margins to close the year at 24%.

Some Headwinds As Demand Increases

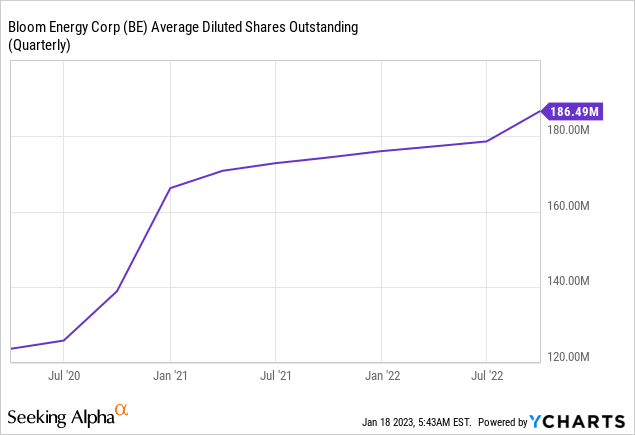

Hence, will Bloom make a great investment? It depends. The company recorded a net loss of $57.1 million during the last reported third quarter with total operating expenses of $103.5 million, up from $80.8 million in the year-ago comp. Bears would also point to the constant dilution. Average shares outstanding is up from around 124 million in the first quarter of 2020 to 186.49 million as of the end of the third quarter.

Bloom raised $388.7 million during the third quarter through the sale of 15 million of its Class A shares at $26 per share. Hence, cash and equivalents ended the third quarter at $492.1 million, up from $121.9 million in the year-ago period and against total debt of $1.08 billion. Bulls would be right to highlight that despite cash from operations coming in negative at $70 million during the quarter, Bloom is still expecting positive free cash flow for its full fiscal 2022.

The company’s fourth quarter typically shows a stronger operating cash position, setting up what would be the strongest quarter for cash generation in Bloom’s history against cumulative operating cash outflow of $168.4 million for the prior three quarters. Momentum has continued post-period end with new customer wins in Western Europe. Overall, Bloom is operating in a secular growth space and its relative robustness against the discombobulated stock market infers the level of investor confidence in its plans to seize on the opportunities posed by decarbonization. I’ve added this to my watchlist and would like to see enhanced free cash flow generation before considering a purchase.

Be the first to comment