Dzmitry Dzemidovich

Introduction

In January 2022, I wrote a bearish article on SA about BK Technologies (NYSE:BKTI) in which I said that I was skeptical that the company would get back into the black when the world’s supply chain issues ease.

In August, I shared with the subscribers of my MP that I was putting BK Technologies on my watchlist as its growth plans seemed compelling and now I’m bullish considering total order bookings for 2022 surpassed $70 million. Let’s review.

Overview of the recent developments

In case you haven’t read my previous article about BK Technologies, here’s a brief description of the business. The company is involved in the production of high specification communications equipment for public safety professionals and government agencies and its products include portable and mobile radios, repeaters, and base stations. The key customers include the United States Armed Forces, the U.S. Department of the Interior, and the California Department of Forestry and Fire Protection among others. In addition, BK Technologies has strategic contracts for ease of procurement with several government agencies.

BK Technologies

Sales to United States government agencies accounted for 36.4% of net sales during the first nine months of 2022.

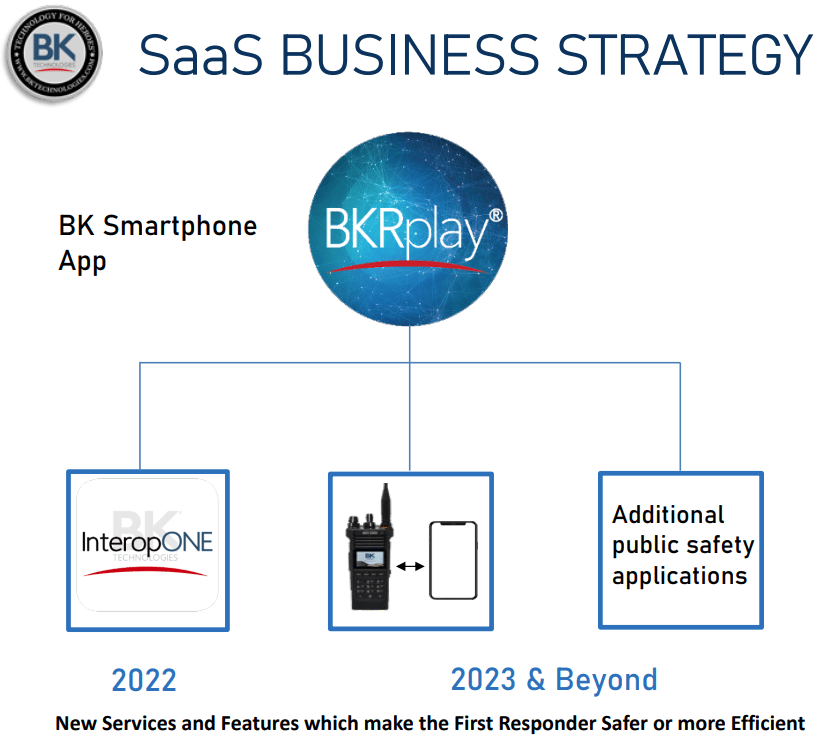

In February, BK Technologies launched a Software as a Service business unit, which has launched a Push-To-Talk over Cellular (PTToC) service named InteropONE that enables universal interoperability to first responders in the public safety sector.

BK Technologies

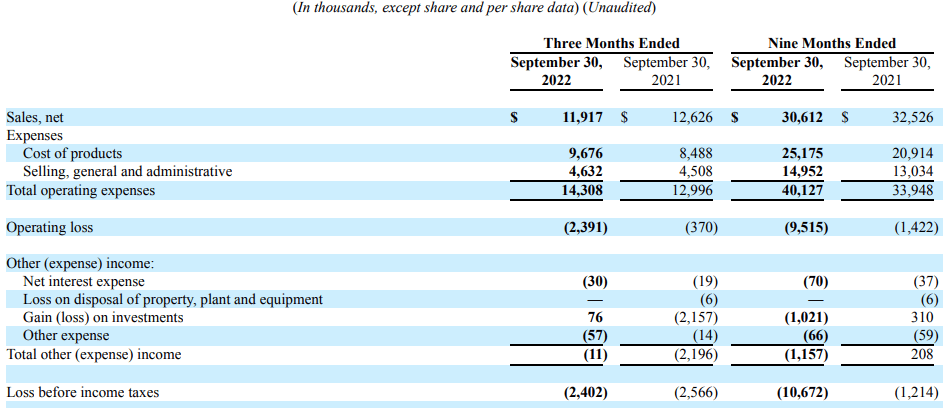

Looking at the financial results for the first nine months of 2022, net sales declined by 5.8% year on year to $30.6 million as the company was negatively impacted by the worldwide shortages of materials, in particular semiconductors and integrated circuits. In addition, Hurricane Ian passed directly over the company’s Melbourne facility in Florida in the last week of September which led to operations being halted for two days. Gross profit margins declined due to the materials and freight prices increases and shortages and the operating loss soared to $2.4 million.

BK Technologies

Considering the financial results of BK Technologies are deteriorating, why am I now bullish on the stock? Well, the two main reasons for this are that the orders for the BKR 5000 single-band radio launched in August 2020 are exceeding expectations and that the launch of BKR 9000 multi-band radio is likely to take place soon as it was recently delivered to a third-party lab for Federal Communications Commission test and certification. In Q4 2022, BK Technologies delivered a total of 11,200 radios thus bringing the total for the year to 25,200 units and total order bookings reached a record $70 million as of December 2022. Considering the total order bookings for 2021 came in at $55.5 million it seems that BKR 5000 is in high demand at the moment and revenues are likely to pick up in Q4 2022. BK Technologies has added a second production line in its Melbourne facility in order to meet the strong demand as the backlog orders stood at $42 million as of September. BK Technologies mentioned in its latest presentation that key component shortages related to this product were cleared in September as it secured a two-year supply of key chips (see slide 4 here). In addition, BKR 5000 margins were expected to return to near historical levels by December 2022.

The launch of BKR 9000 is key as this product should help the company to expand in several new market verticals, thus boosting the addressable market significantly.

BK Technologies

BK Technologies is currently targeting annual revenues of $100 million by 2025 and I think that economies of scale could allow it to reach an annual net income level in the region of $5 million. With law enforcement expected to upgrade portable communications platforms in the near future, demand for this new product is likely to be strong over the coming years. However, I rate the stock as a speculative buy considering the launch of BKR 9000 has been delayed several times already. According to discussion on RadioReference, the initial release date was planned for April or May of 2021. During its Q3 2022 earnings call, BK Technologies said that it encountered some issues during the second manufacturing run completed in September which were being addressed.

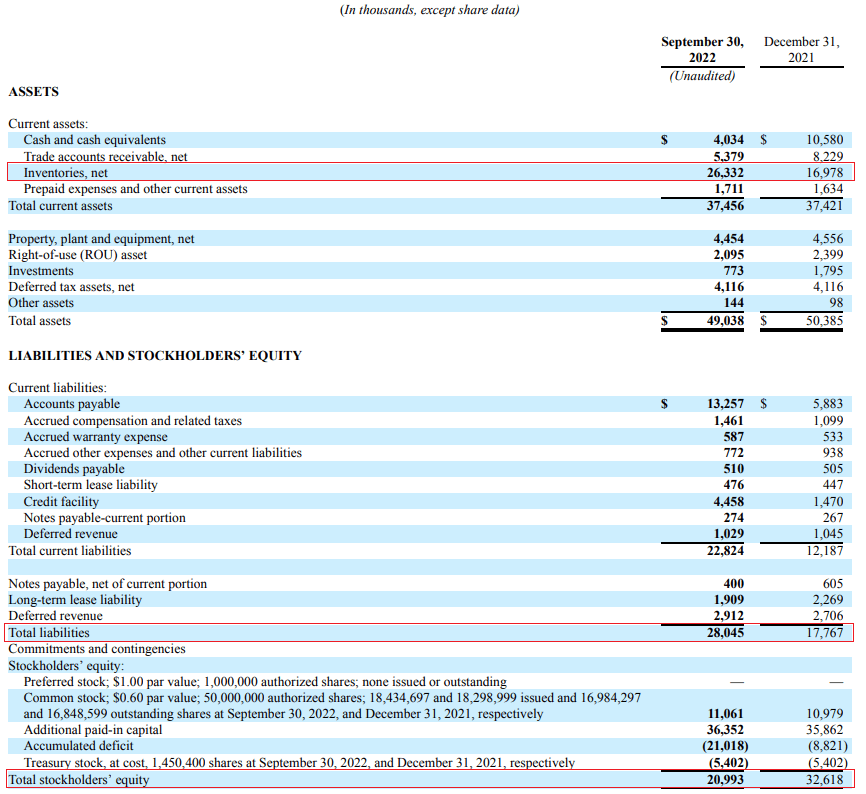

In my view, another major risk here is the state of the balance sheet as liabilities soared to $28 million at the end of September due to shipment delays. The stockholders’ equity was down below $21 million at the end of the quarter and I think there could be significant stock dilution here if orders for BKR 5000 dry up and the launch of BKR 9000 is delayed once again.

BK Technologies

Looking at the near future, the company’s Q3 2022 presentation includes a forecast for radio units shipped rising to 32,000 (slide 7 here) in 2023 and with margins improving, I think it’s possible that the company gets back into the black soon. This could be a significant catalyst for the share price.

Investor takeaway

The past year was challenging for investors of BK Technologies as the company’s sales and margins were pressured by supply chain disruptions and delays due to Hurricane Ian. Yet, there was a silver lining as BK Technologies saw a significant booking activity driven by BKR 5000 and delivered over 11,000 radios in Q4. With costs for materials and freight slowly returning to historical levels, I think that the company is likely to return to profitability in the near future. The launch of the next-generation BKR 9000 multi-band radio seems to be just around the corner and I think that the company has decent chances of boosting annual revenues to $100 million by 2025.

However, the balance sheet of BK Technologies is not in pristine state and another delay of the launch of BKR 9000 could create serious issues. In my view, it could be best for risk-averse investors to avoid this stock.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment