ra2studio

More than four years have passed since I started writing a very extensive series on Bitcoin (BTC-USD), comprised by the following articles:

The FTX (FTT-USD) failure has again shown crypto remains exceptionally vulnerable to strange failures, generally affecting crypto exchanges.

These failures – usually attributed to hacking – typically produce very large losses for customers, as well as lead to renewed distrust in crypto in general, and Bitcoin (BTC-USD), the best-known crypto, in particular. Calls for more regulation are typical, at this point.

Today’s article is about a lesson which the FTX collapse allowed us to learn, or perhaps re-learn, which fully applies to Bitcoin.

I still recommend anyone not very familiar with Bitcoin or cryptocurrencies in general to read the entire series, starting with the first article. Whether you share my opinions or not, you will greatly increase your knowledge on this cryptocurrency – the biggest of them all.

Crypto-Holding Institutions Are Intrinsically Unsafe

This is something many “investors” in Bitcoin fail to understand.

The belief in Bitcoin’s (and other cryptos’) resilience to direct attacks on the blockchain, clouds the obvious fact that the blockchain itself serves as nothing but a master/omnibus account when it comes to a crypto exchange or broker.

In this sense, crypto exchanges aren’t different from regular banks, brokers or exchanges. These, too, don’t really keep 1 account per customer when it comes to depositor or investor assets. Instead, for instance at the central bank, the bank will have just one account. And the broker will equally have just one account at a securities depository, or at the exchange. Then, internally, a broker divides its assets present in these aggregate (master/omnibus) accounts by using an internal book-keeping system to establish how much of the asset each customer owns.

It’s the exact same with a crypto exchange. On the blockchain (per each cryptocurrency), the crypto exchange will keep just 1 or a few addresses where all the crypto will be stored. Then, an internal book-keeping system will divide this aggregate between customers.

Since assets are kept concentrated in one (or few) places, regular banks and brokers have to be extraordinarily cautious regarding the security of the access to this place (as well as the internal book-keeping).

Indeed, no one executive will be able to tamper or move assets recklessly both within the bookkeeping system, or from the master account. Systems will be in place to, at all times, verify the consistency of the aggregate assets implied by the internal book-keeping system, and the value held on master accounts. No executive will have the power to move assets quickly and in large chunks, and no unjustified (not consistent between the ledgers) movement of assets will be possible silently.

Cryptos are different:

- No internal system belonging to a crypto-holding institution can prevent or censor the movement of crypto by any person having the keys to the (few) exchange wallets.

- Unlike in at a regular financial institution, such movement can be initiated from anywhere (geographically) and completely outside the company’s software infrastructure.

- The person knowing and using the keys needn’t be known to the institution or part of it (though he can be).

- The person using the keys needn’t sign anything (at the institution) to move crypto.

- The person using the keys needn’t request anyone the permission or ability to realize a transfer.

- The person using the keys needn’t even penetrate or use the institution’s systems in order to steal the crypto.

Instead, a person just has to sign a transaction with the required keys, and immediately the exchange wallets will be breached, and the transaction will go through with nothing and no one being able to censor it.

Of course, like with regular financial institutions, it will be possible for the crypto-holding institution to immediately realize an accounting inconsistency emerged between the value held in its master accounts, and the one implied by its internal bookkeeping. Unfortunately, even in the case such alarm uncovers trouble, the trouble will already be irreversible (a characteristic of Bitcoin and most other cryptos – transactions cannot be reversed or censored).

This, for all purposes, means that any institution holding crypto will always be unsafe. There are no possible safeguards for this structural vulnerability.

Misdealing Is Much Easier With Crypto

This is a corollary which results from the previous observation.

Without looking – it’s doubtful FTX transferred cash or cryptos to Alameda.

It’s much more likely FTX bought stablecoins (with the cash) and shared keys with Alameda. As well as shared keys regarding various master crypto accounts. The money wouldn’t move (in a suspicious way), so no third parties would thus be warned. Ownership would just be a book entry. Internally, there could be warnings – but those were suppressed, as per Reuters (bold is mine):

In a subsequent examination, FTX legal and finance teams also learned that Bankman-Fried implemented what the two people described as a “backdoor” in FTX’s book-keeping system, which was built using bespoke software.

They said the “backdoor” allowed Bankman-Fried to execute commands that could alter the company’s financial records without alerting other people, including external auditors. This set-up meant that the movement of the $10 billion in funds to Alameda did not trigger internal compliance or accounting red flags at FTX, they said.

In his text message to Reuters, Bankman-Fried denied implementing a “backdoor”.

This kind of action is possible because generally, in crypto, there is no ownership nexus. He who has the keys, controls the crypto but doesn’t really own it. He’s just able to move it. And if 2 (or more) institutions have the keys to a given crypto address, then they both can move this crypto and act as its owners. How they report ownership of the underlying crypto at any given time is entirely arbitrary. How they chose to move it to “somewhere else” at any given time is also entirely arbitrary (but will raise red flags internally in the unaware institution, as explained).

In the presence of a misdealing actor, this is a tremendous hole in crypto security. The misdealing actor will single-handedly, and without possibility of censorship, be able to move assets away from any of his controlled (or even not controlled, as long as they were controlled in the past) institutions at ease. This risk probably expressed itself both during the time FTX and Alameda were seen as viable, legitimate entities, and after that time (during the supposed hacking).

Notice how this differs from common banking. In common banking, each account has an ownership nexus. 2 different institutions will not be able to claim ownership of the same master account. And to transfer assets from the account of one institution to the account of another will require the agreement of those with the power to commit the institution, leave a paper trail, and be subjected to scrutiny. The financial institution holding one or both accounts (for customers) might even suspect the activity taking place and interrupt it to conduct further scrutiny. The risk for someone trying to compromise a crypto-holding institution is thus many orders of magnitude higher, due to this structural difference.

Finally, even if an illicit transaction takes place at a regular institution, there’s still a good chance to reverse it. Such isn’t possible with Bitcoin.

Regulation Won’t Solve The Problem

The flaw I described, and which must have been taken advantage widely in the context of the FTX collapse, cannot be solved by regulation. The most regulation can do is to be extremely strict regarding internal controls up to and including the internal warning system.

But crucially, there is no possible system or regulation which can prevent or reverse a master account from being abused from anywhere in the world, just as long as the keys to the master account are known to someone wanting to compromise them. This is structural to Bitcoin and most of crypto in general. It is so by design.

Hence, regulators, when it comes to crypto, will always be handicapped. This is unlike the present financial system, where checks and balances can keep control of most catastrophic attempted transactions, or reverse them after the fact. Indeed, the one common fraud within the financial system is typically slow – it mostly consists of making uneconomic loans to “friendly” customers. This can over time collapse an institution, but it will tend to:

- Last a long time, since no single loan can be catastrophic and avoid scrutiny, plus loans aren’t instant.

- Not compromise a very large percentage of customer deposits.

- In the end, to not imply widespread customer losses in the sense that deposit insurance schemes exist the world over. It can, however, lead to creditor and investor losses.

Anyway, the central point is:

- Crypto in inherently unsafe.

- Crypto is easier to steal as the possession of just 1 key can compromise a master account irreversibly and without the chance for censorship.

- Given the above, the losses will tend to be larger and affect customers (depositors) to a much larger extent than in regular deposit-taking financial institutions.

Outside Of An Institution, Crypto Is Unpractical

Crypto fans will immediately say that none of this applies if you just keep your crypto with yourself. Which is true, the vulnerabilities I talk about are present in the crypto ecosystem as a whole, not on the underlying blockchains. It’s very hard to take your crypto if you don’t have it deposited somewhere.

However, at the same time, it’s wildly unpractical to hold crypto yourself. Besides the opportunity to lose it forever just because you lose the key, there’s also the fact that crypto is crazily unpractical.

For investors, which is what this argument concerns itself about, there’s simply no practical way to trade in and out of your crypto without putting it into an exchange, which is where liquidity for trading exists. Hence, there’s no solution here either.

There Will Likely Be More Details Of Wrongdoing At FTX

Already, we know that FTX used customer funds which ought to have been segregated, to be loaned out to Alameda, which proceeded in some form to lose them. We also know that FTX did this in a covert way. These seem the main wrongdoings within the collapse.

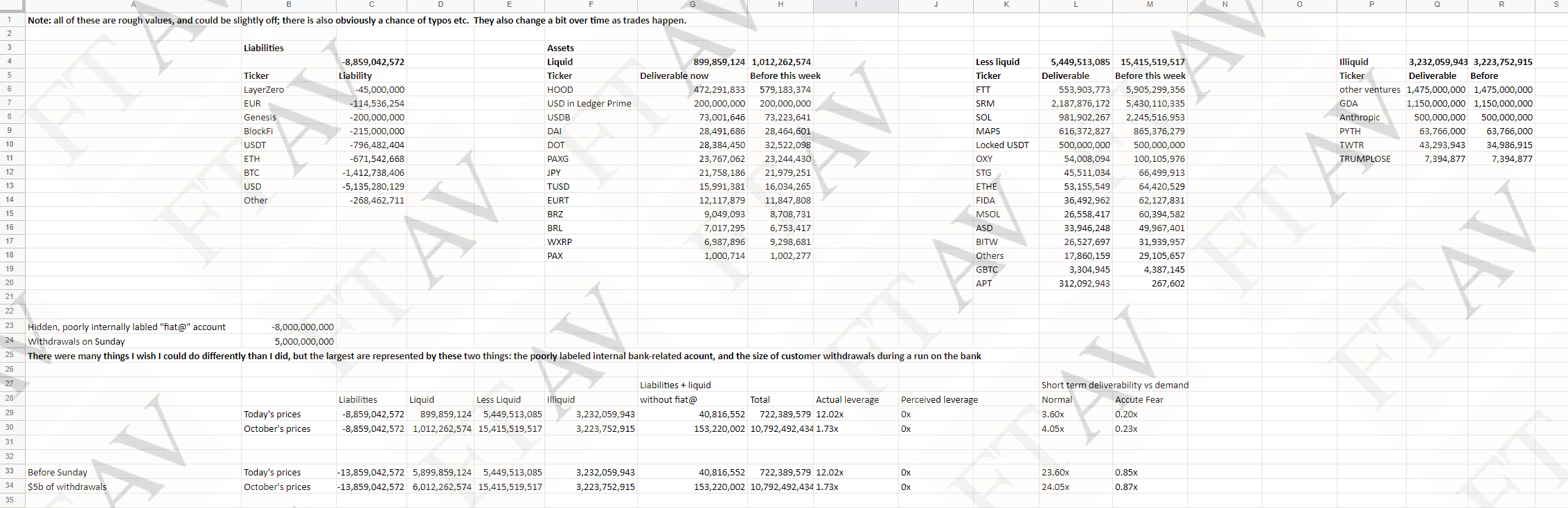

However, I’ll immediately put forth that further wrongdoing is going to be disclosed. From observing the “haphazard” FTX Balance Sheet volunteered by SBF to which the Financial Times had access, I conclude the following:

{kind=link}

- We notice the existence of large liabilities in several cryptos, including BTC and ETH. These are to be expected. If a customer decides to buy BTC, acquiring that BTC for him will become a liability to FTX. This is so because, if a customer buys BTC then FTX has to buy BTC and hold it in one of its master wallets. Hence, FTX’s balance sheet will show both a BTC asset (held in its master wallet) and a BTC liability (the BTC is owed to the customer and registered as so in FTX’s internal book-keeping system). Hence, one would expect BTC to not only show up on the liability side of FTX’s balance sheet, but also appear on the asset side, and for the amount of BTC on the asset side to be the same or more than what customers bought for themselves.

Yet, there is no meaningful BTC or ETH on the asset side. It thus follows that it wasn’t just customers’ cash funds which might have been abused. Even the customers’ crypto assets were abused. This is yet to be disclosed in the news (though it is implied by the leaked balance sheets). Indeed, given what’s on the asset side (mostly obscure FTX-linked tokens), I’ll go as far as to say that nearly all customer assets (not just cash) are gone.

It also follows that in abusing customer crypto assets, the exchange had to keep a diverging accounting of those assets on the client-facing interface. Or else, the customers would think their assets still existed, which they didn’t. This is part of the “backdoor” we earlier talked about.

The FTX Customer Losses Are Going To Be Very Large

It’s immediately evident that if customers face losses, then other creditors and investors will be entirely wiped out.

However, from the leaked FTX balance sheet, it’s also immediately obvious that very large losses are coming to the customers / depositors as well. Initially the reports put this shortfall at $1-$2 billion, but there’s reason to believe the shortfall is much larger. Let me explain why:

- Taken at face view, the leaked balance sheet indicates $8.9 billion in liabilities (of which around $8.1 billion look to belong to customers), and $9.6 billion in assets ($0.9 billion liquid, $5.45 billion less liquid, $3.23 billion illiquid). This translates into an actual positive book value of around $0.7 billion. One would argue that perhaps the problem was just one of liquidity mismatch, between the assets and liabilities. And that some emergency help could plug the liquidity hole until assets could be liquidated.

- However, immediately there is a supposed hidden $8 billion liability. That totally changes the balance, as now the hole could be as large as $7.3 billion.

- The hole, though, is even larger. After all, many of the illiquid assets will be all but worthless in a liquidation scenario. This includes $4-4.5 billion of the less liquid assets, and likely nearly $3.15 billion of the illiquid assets. Thus, $7.15-$7.60 billion of the $9.6 billion in assets looks very dubious.

- If we take these dubious assets off, we can thus be looking at just $2 billion in actual assets trying to satisfy $8.1 billion in customer claims. In this case, recoveries for customers would be around 25%.

- However, there might be reason to believe that the hidden $8 billion liability also belongs to customers (since it matches with the kind of reporting that says around half of the customer deposits were lent out to Alameda). In that case, recoveries might be as low as around 12.5%. This could be mitigated by assets at Alameda, but the scenario there is equally disastrous, with a lot of made-up assets (FTT-USD) as well as the same kind of less liquid assets held by FTX which will be near worthless in a liquidation scenario.

Conclusion

This article leads to the following conclusions and predictions:

- Bitcoin (and crypto in general) is structurally unsafe when used through an institution. And not even regulation can make it safe, in the sense that there will always be an extreme vulnerability because of the potential to sign irreversible and un-censorable transactions from anywhere in the world just by knowing the keys to the master accounts at a crypto-holding institution.

- Bitcoin (and crypto in general) is also easier and more appealing to misdeal, given that structural problem. I struggle to call it a “flaw”, since this structural problem is actually part of the design for Bitcoin.

- I believe recoveries for customers will be low at FTX. For FTX investors and creditors, recoveries will be zero – they come after customers, so if customers are going to suffer large losses, everyone else is a zero.

- The blockchain technology is valid, but the “get rich quick” mentality means the things speculators can bet on (the value of crypto coins) is divorced from the value the technology can add. Indeed, blockchain technology doesn’t require any “flying tokens” to be used or to be valid.

- One, or more, stablecoins built with a more robust permission system as well as a more robust reversion system (while keeping anonymity) will eventually steal away most of the functional, legitimate, use for crypto. This will lead to a loss of value for Bitcoin, Ethereum (ETH-USD), etc.

Be the first to comment