BT Series/iStock via Getty Images

Overview

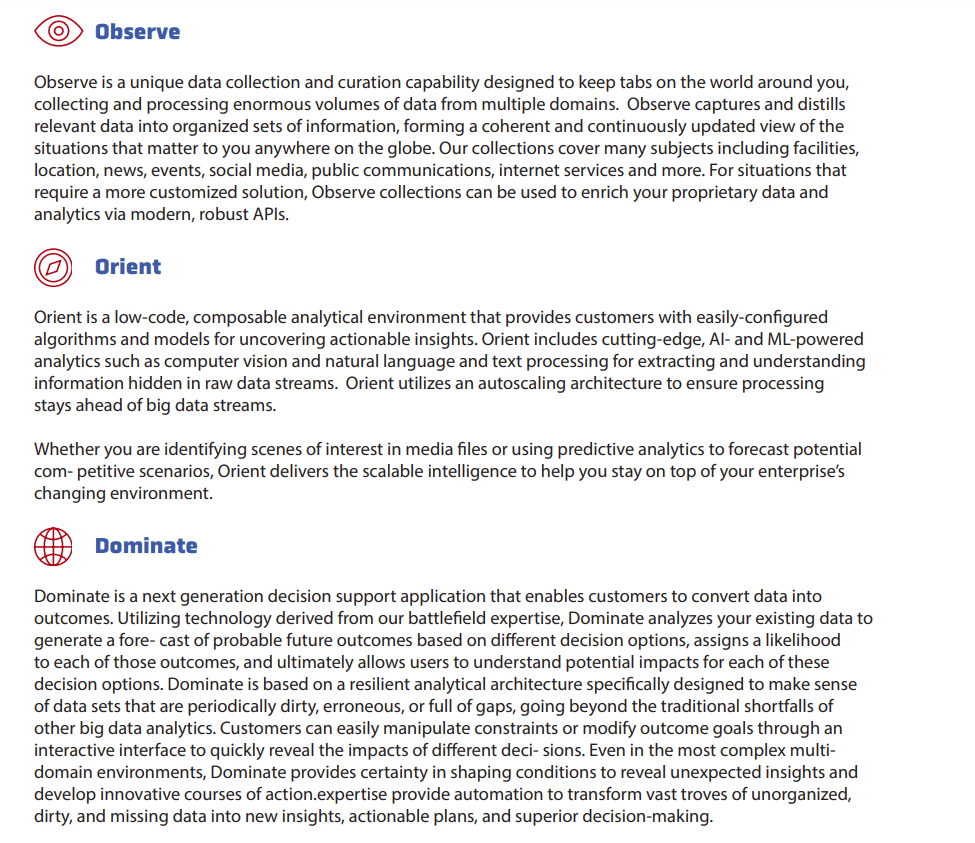

BigBear.ai Holdings (NYSE:BBAI) is a software company focused on operations and decision science (optimization). Leveraging artificial intelligence, BigBear provides a suite of modelling capabilities to optimize operations across a suite of industries – including manufacturing/logistics, hospitals, shipyards, and others. This portion of its offering is referred to as ‘dominate’ by the company.

The next piece of BigBear’s offering is its capacity to ‘orient’ itself in the context of data. To practitioners, this refers to identifying statistical patterns that are quite likely not visible to the naked eye – a go-to capability of any quality ‘deep learning’ system. By absorbing all of the relevant data and marking statistical trends, the system is able to identify dimensions that people cannot.

Additionally, the company provides a capability to ‘observe’ data flows using artificial intelligence. Leveraging real-time data feeds, BigBear allows for rapid identification of changing/emerging patterns within these data flows. This can take the form of any kind of data, including but not limited to social media, news, and custom defined events via the firm’s API.

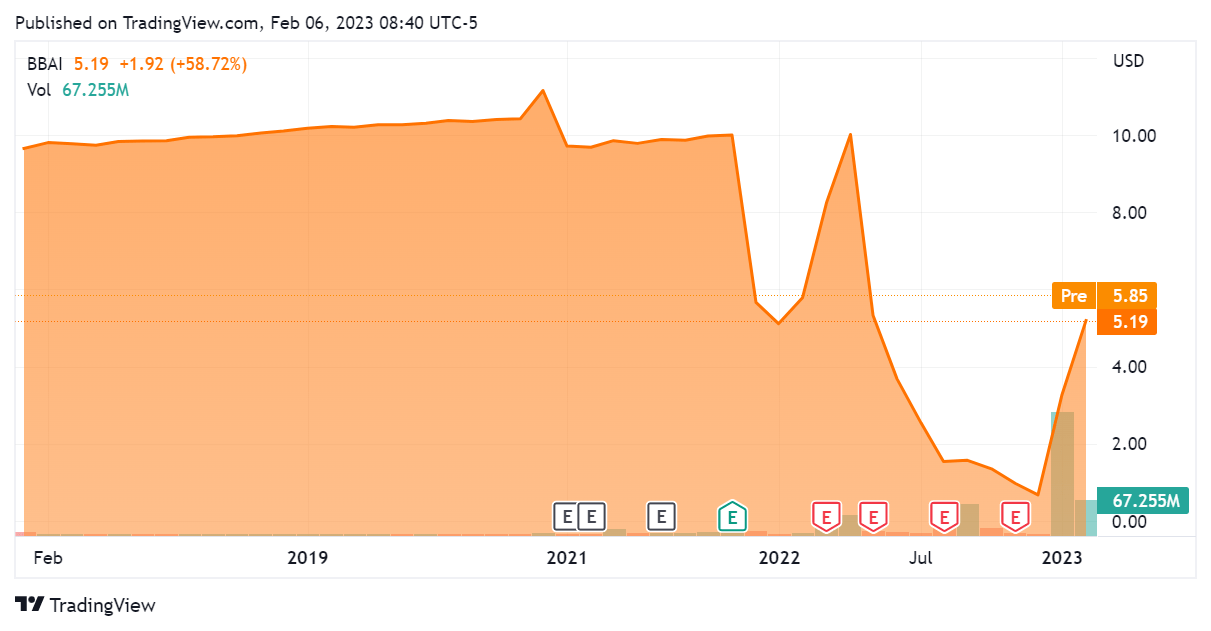

Bigbear.ai 2.6.23

The company went public via SPAC merger in Q4 2021 and has traded under its current name since. While initially trading in the $9 – $10 range, BigBear saw a significant drop-off in the wake of several earnings misses.

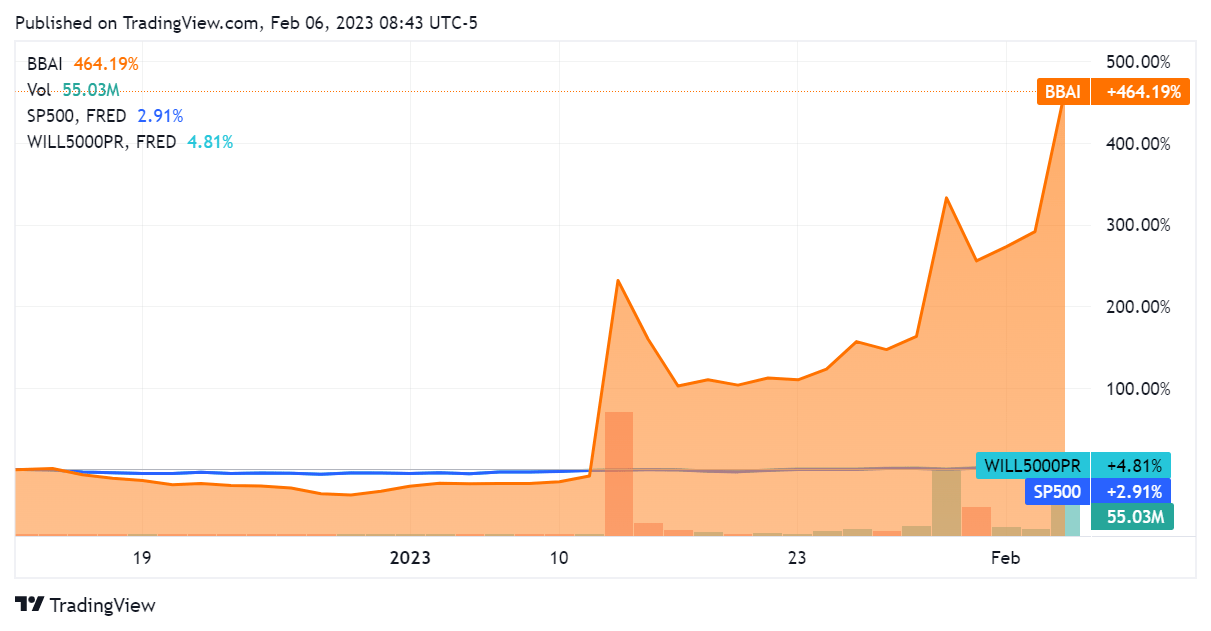

seekingalpha.com BBAI 2.6.23

2023 has been a completely different story, with the stock appreciating significantly; a slew of double-digit increases throughout January has compounded to a 464% YTD gain. Indeed, this represents a very significant multiple of both the S&P as well as the Wilshire 5000 index as to price performance.

seekingalpha.com BBAI 2.6.23

Recent appreciation is likely due to investors becoming more attuned to the ‘AI factor’ within the current market context as well as the significant contract that BigBear has secured with the USAF. By factor here I am referring to a statistically identifiable driver of price movements across a range of securities, akin to ‘growth’ or ‘value’. This is a sensible explanation as artificial intelligence has been discussed significantly more in the context of big tech firm earnings as well as the news cycle (ChatGPT). Additionally, other artificial intelligence stocks (or at least stocks with AI in the name) have appreciated over the last several weeks; a deeper dive into this factor per se will be left to another article.

This article will review the company’s financials in order to determine if the stock presents a quality investment at present.

Financials

As with any relatively early technology entity and/or growth stock, we must review revenue first.

seekingalpha.com BBAI 2.6.23 seekingalpha.com BBAI 2.6.23

Revenues are at $145.6M for fiscal year 2021, representing a significant ($96.2M) since the company’s first published fiscal year of 2018. Gross profit has also moved in tandem, with the numbers correlating tightly. While we shouldn’t extrapolate this data too far out, this company appears to be growing at the rate that one should expect of a technology company of its size.

These results unfortunately are not yet translating into the bottom line. Net income actually took a precipitous hit in 2021. As per the earnings call transcript for that quarter, this was owing to stock-based compensation expense of $61 million, a $33 million write-off to the fair value of the company’s share purchase agreements, and $12 million for one-off transaction expenses.

seekingalpha.com BBAI 2.6.23

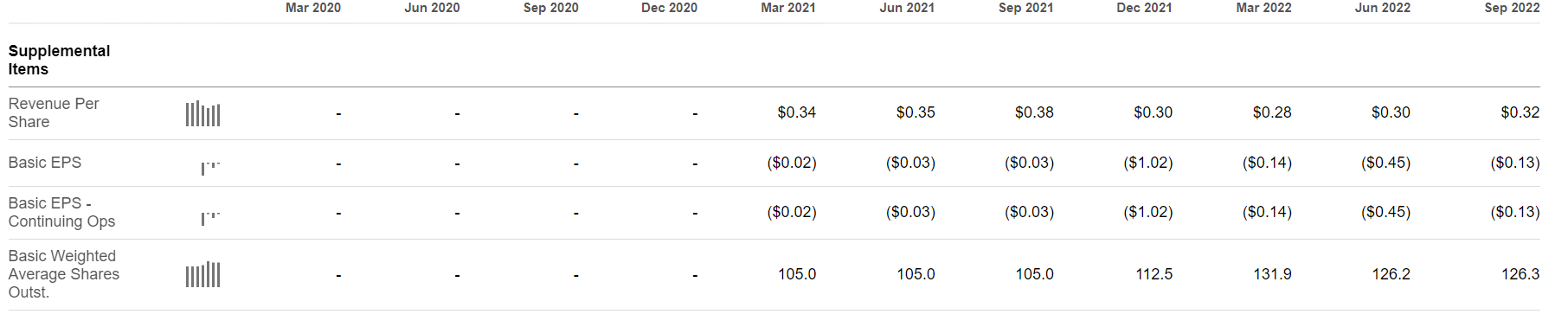

As such, we must continue to pay attention to the quantity of shares outstanding for this entity. It appears that the company had hit a peak of 131.9 million shares outstanding during its IPO quarter and has begun to take that number down via share repurchases. Given this, it’s fair to expect that stock-based compensation expense shouldn’t drag down net income going forward; nonetheless, the significantly negative net income has amounted to negative retained earnings of $223.2M as of Q3 2022. This is now money that the company will have to earn back, creating a hurdle to clear before it generates fundamental per-share appreciation or distributes dividends.

seekingalpha.com BBAI 2.6.23 seekingalpha.com BBAI 2.6.23

The company has managed down its net operating loss since going public, and the recent numbers give some degree of confidence in its capacity to break even relatively soon.

seekingalpha.com BBAI 2.6.23

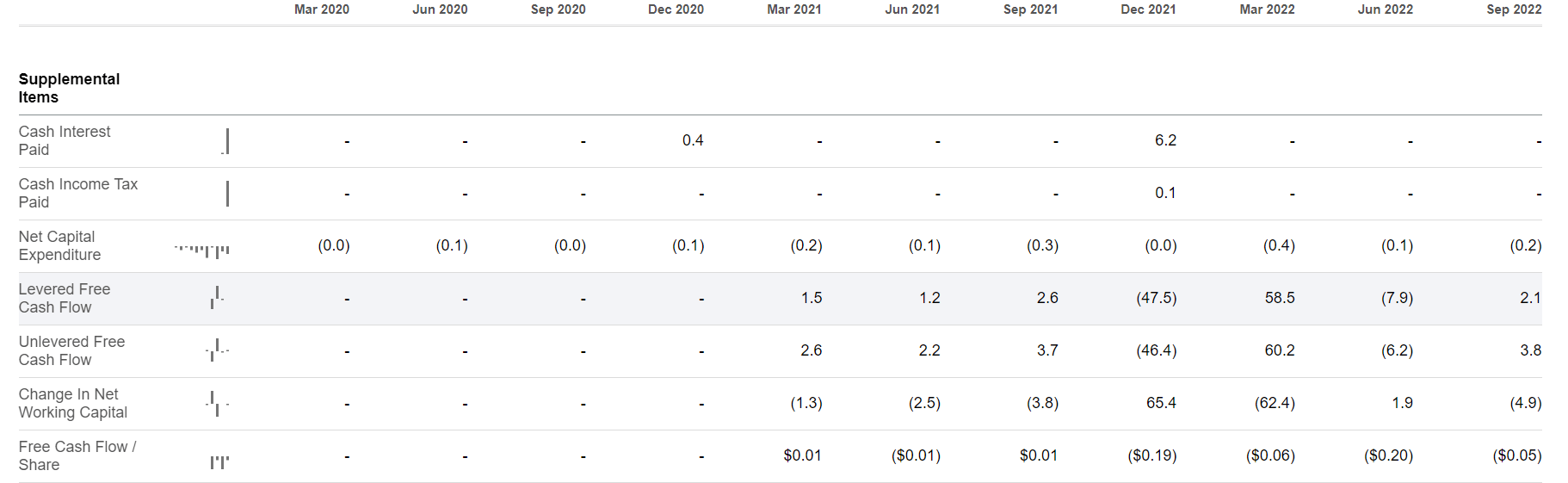

As to cash flow, its notable that BigBear has been able to generate positive cash flow for most quarters since going public. While posting a severely negative quarter during its IPO quarter, the subsequent quarter saw a boom in cash flows and two quarters fluctuating around zero since. Additionally, the per-share cash loss is decidedly close to break-even. It is quite possible that the firm turns the corner on this with its next earnings release; numerically speaking, I believe this is very much feasible.

seekingalpha.com BBAI 2.6.23

Worth noting is that the company is not paying any interest and has not done so for 3 quarters running. We can conclude that the cash it is generating from operations is sufficient to keep it a going concern. This makes the firm’s balance sheet less relevant for our first-look analysis.

In sum, these financials look healthy to me. While the accumulated loss as to retained earnings is significant, it is only about 1.5x the company’s yearly revenues. The ongoing growth in revenues as well as the cash flow picture allow me to conclude that this early stage technology company is headed in the right direction.

Conclusion

BigBear is a unique AI company that is seeing traction with its offering. I am bullish on its capacity to scale revenues as it has successfully sold into the US military, including both the Air Force (Q1 2023) and the Army (Q4 2022). The firm is well-positioned as it now has active customers across both the public and private sectors, making it similar to Palantir in terms of its commercial footprint.

Taking this into consideration as well as the fact that the firm is able to operate itself through its own cash flows, I consider this a quality early tech stock and a good play for the AI factor today. I am calling it a buy.

Be the first to comment