Ivanko_Brnjakovic/iStock via Getty Images

Bear thesis

When I see DoorDash (NYSE:DASH) and its history as a public company, it serves as a big reminder on why buying into IPOs could be a terrible idea. Valuation made very little sense, but the story was growth and there was very little to gain by buying into this IPO. But this was lost on investors. The delivery company’s shares closed at $190, more than 80% above its initial public offering price of $102. This episode reminded me of a quote from the great Benjamin Graham:

In every case, investors have burned themselves on IPOs, have stayed away for at least two years, but have always returned for another scalding. For as long as stock markets have existed, investors have gone through this manic-depressive cycle

Fast forward to now, it looks like the growth story has started to take a turn. Growth has peaked and there is no new story that is attractive enough to continue to carry the stock. This has been well reflected in the stock price. The stock is down more than two-thirds from its first day of trading. Does it mean it is a buy now? Far from it. As we will explore in the upcoming sections, it seems like we would be worse off buying now. In addition to slowing growth, investors have to still contend with an unprofitable business model, insider selling, stock dilution and sky high valuation.

Slowing growth and unprofitable Business model

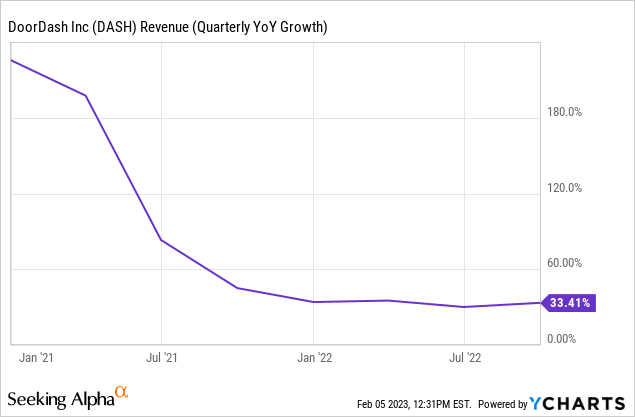

Comparable QoQ has slowed considerably. From a peak growth rate of 225% in 2020 to 33% in its most recent quarter, it is quite obvious that growth has fallen off a cliff.

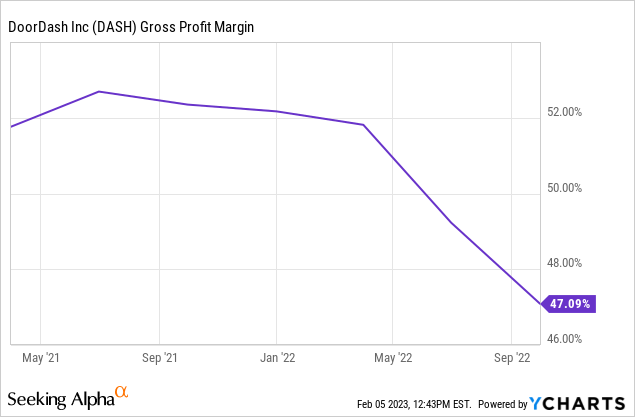

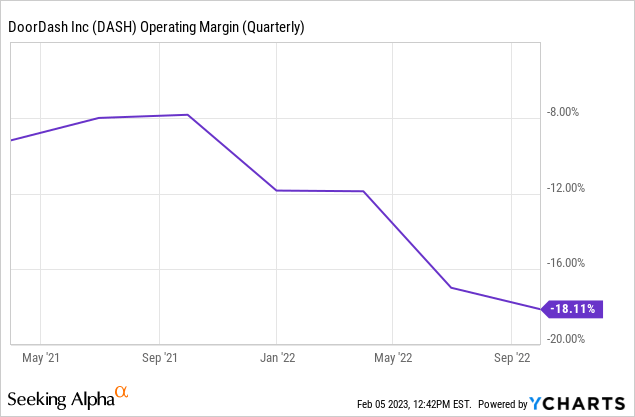

Now could this be justified? It can be argued that the pandemic pulled forward a lot of growth and this slowdown was only natural all things considered. But things are not looking so good under the hood either. Gross profit has tanked, and operating margin is still negative.

With expanding losses and EPS standing at -$0.77, it’s hard to expect profitability anytime soon with this company. This phenomenon is spread across delivery apps. The one quarter where it eked out a small profit was during the height of the pandemic. So the elephant in the room is if the best case scenario did not generate a profitable year for the company, when will it ever be profitable? The short answer is there is no realistic path to profitability. Customers are always hunting for deals between different delivery apps. Promotions, marketing and other deals on food delivery always make a big factor for choosing an app for food delivery.

During Q3 of 2022, DoorDash incurred $418 million in sales and marketing expenses, equivalent to 25% of its revenue. This figure, while significant, is still much lower compared to its marketing expenditure in 2019, which was 67% of revenue. This high marketing spend is probably what allowed it to surpass the market share of its then nearest competitor, Grubhub. With no real product differentiation between food delivery apps, it is usually a race to the bottom in terms of bottom line.

My take is that the food delivery model is inherently not sustainable. One way to think of it is when these companies are private, customer prices are subsidized at the expense of venture capitalists. Once they go public, it is the shareholder subsidizing these costs. This is all the more evident when one looks at operating cash flow levels since they have gone public. On the face of it, it looks like it has held steady. But a more sinister picture emerges when one looks at Stock based compensation. When you remove stock based compensation, OCF is negative for almost every quarter.

SBC V OCF (Seeking Alpha Webpage)

Zilch for shareholders

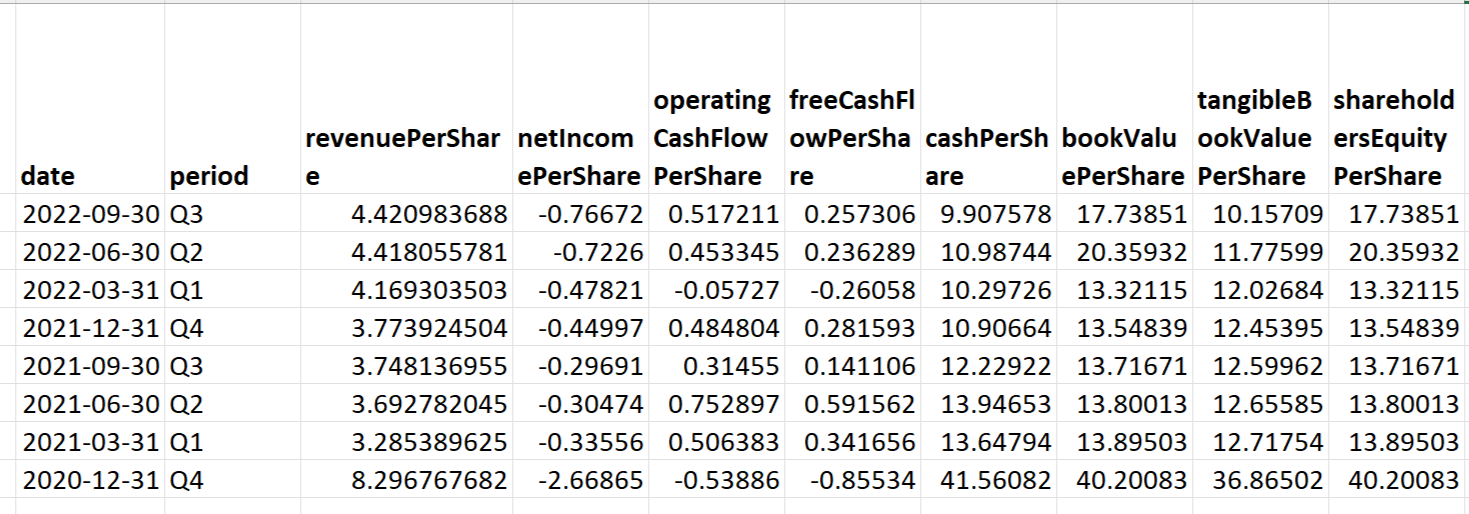

For an investor, there is a simple and quick way to see if the management is bringing any benefit or returning any value to shareholders. Looking at your share of the pie. If they are spinning a story of growth, look at the revenue per share; if it’s a story of value, look at profitability, cash, book value per share etc. From what I see, there is not a single metric that has meaningfully grown since its IPO. In fact, most metrics have heavily declined.

Financial metrics on a per share basis (Financial Modelling Prep computed from company data)

Upcoming quarter

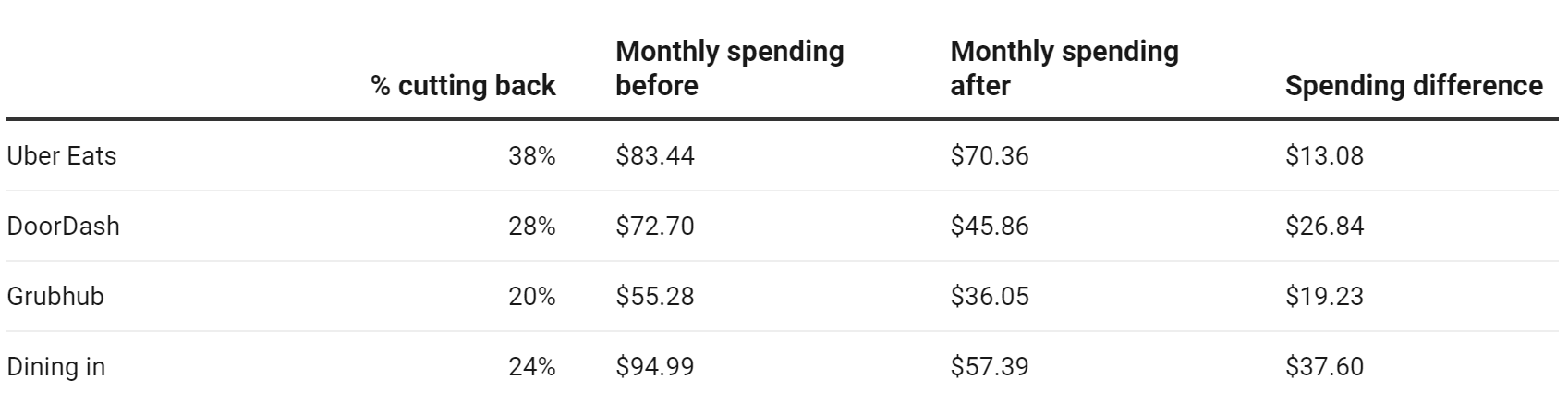

If this article is anything to go by, it is further proof that DoorDash’s growth future looks bleak and the cracks in its story are getting wider. A survey conducted by Personal Capital of over 1,000 consumers found that 94% have reduced their delivery orders or dining out frequency in the past year. 28% of those surveyed reported using DoorDash less, with their average monthly spend dropping from over $70 to just over $45.

Food Delivery Apps Spending (Restaurant Business Online)

Nearly half (47%) of those consumers cited the high cost of delivery for the change. The service can be much more expensive than ordering in-restaurant because it includes delivery and service fees as well as tips, and the menu prices themselves are often inflated. One study found that McDonald’s delivery costs nearly 100% more on average than ordering on-site.

Insider Selling

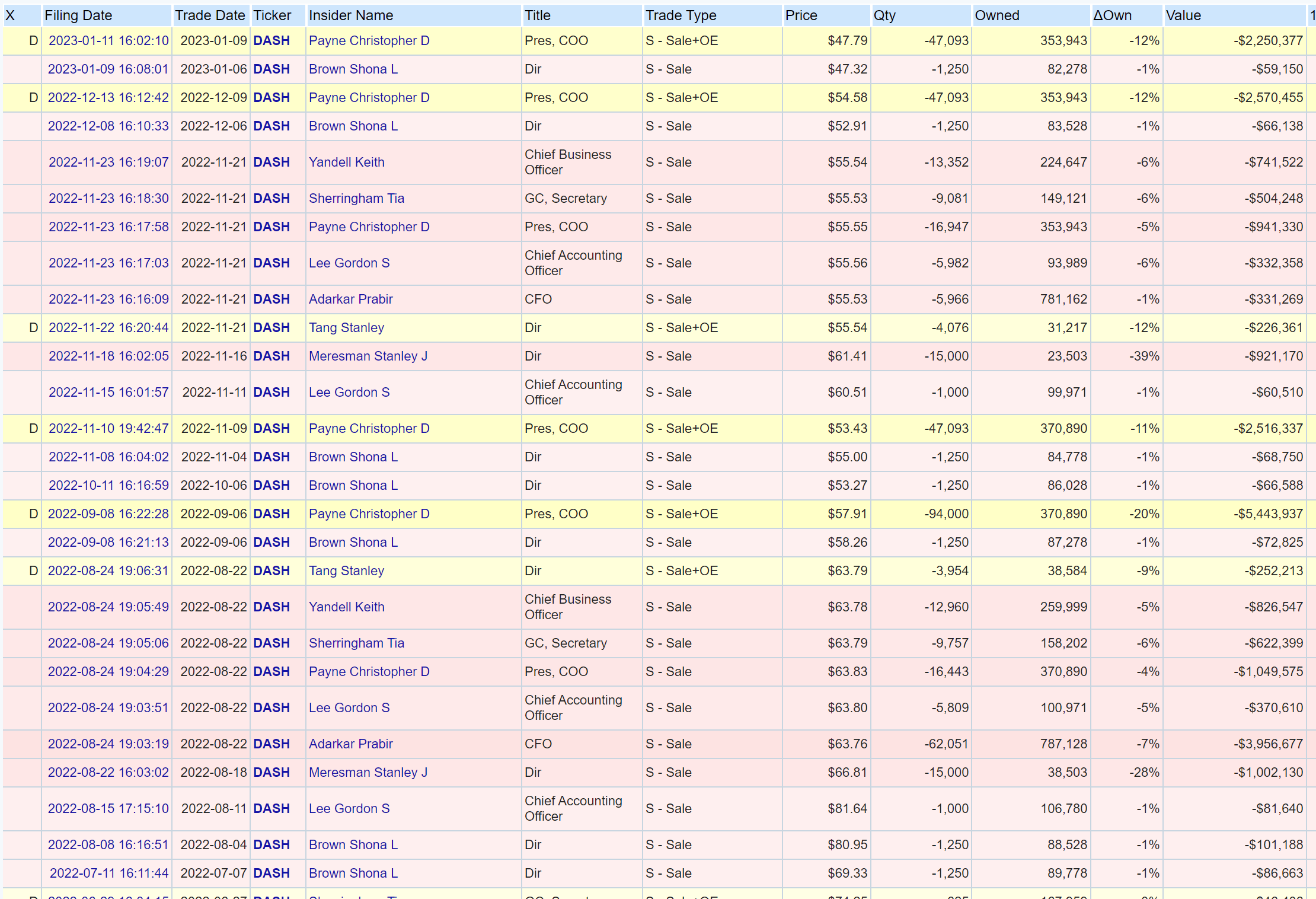

This metric may not be entirely reliable, as a sell can happen due to a variety of reasons. However, it’s hard to completely ignore the sheer amount of insiders that have been selling stock in the company. Over the last one year alone, there have been at least 60 insider sales, and it could be a sign of decreased confidence in the company’s ability to have a good performance in the upcoming years.

Insider Transactions (Open Insider)

Is the price fair?

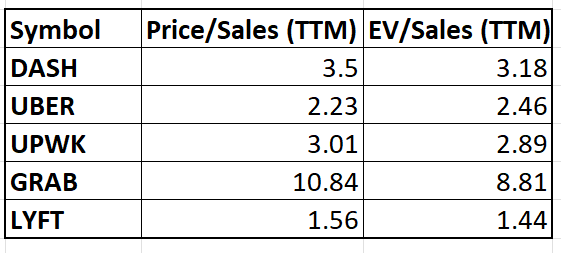

This stock is not attractive even from a valuation perspective. Even after a 75% drop from its high in 2021, the price is hard to justify at its current level. Since it’s not profitable and cash flows are severely affected by SBC, some metrics cannot be used (PE, PEG) or in other instances it will not be reliable (Price/CF, EV/CF). As this is commonly pegged as a growth stock and in consideration of other mentioned factors, we will have to rely only on top line metrics to value this company.

Collected from Seeking Alpha

Finding comparables can get subjective, so here I am basing my comparison on the fact that the shown companies are all in the gig economy space and in the comparable market cap range. Uber, its closest competitor both in terms of geography and product offerings, is valued quite below DoorDash both in terms of Price/Sales and EV/Sales (Maybe worth mentioning that Uber suffers from many of the same problems as DoorDash).

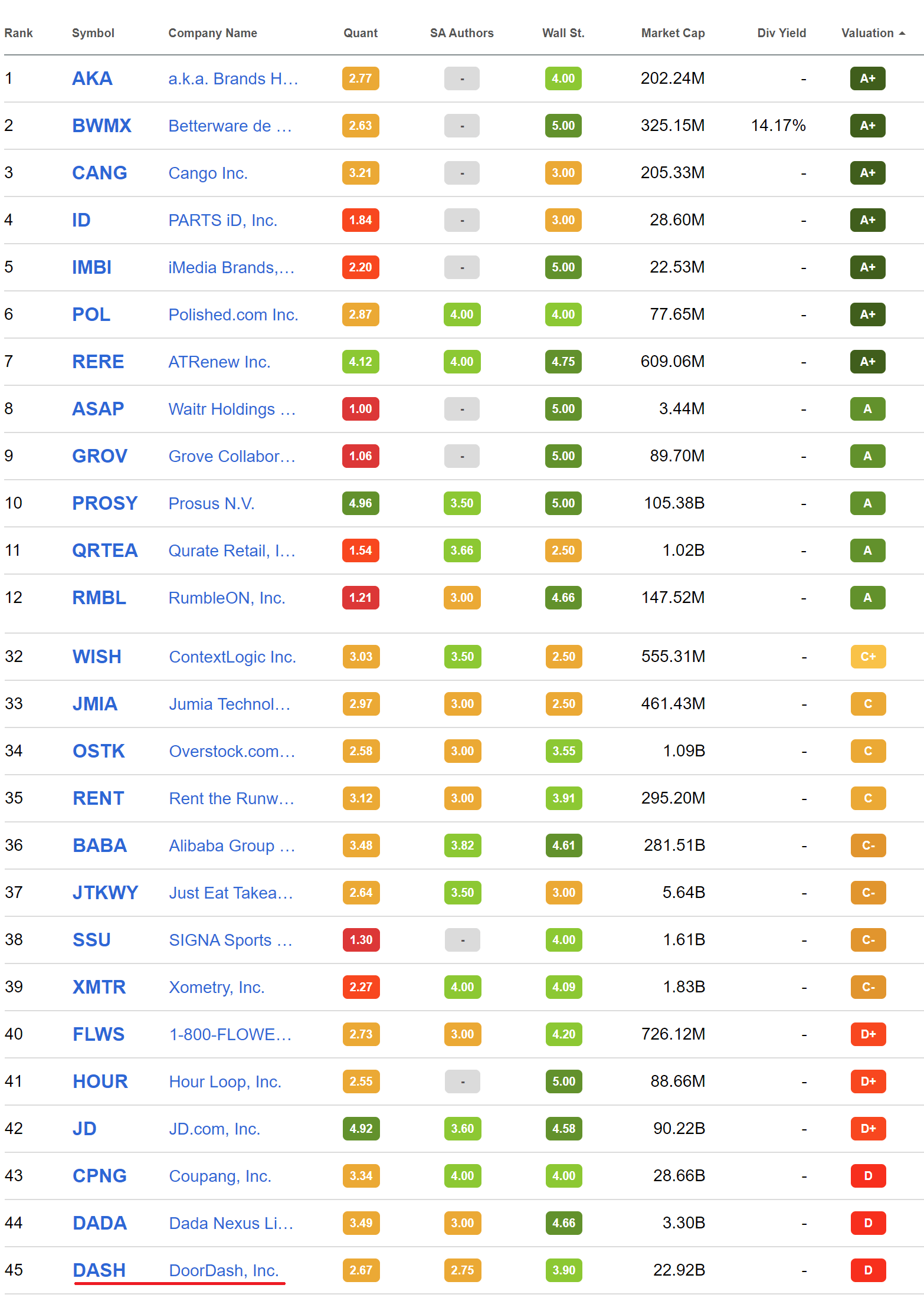

If I zoom out a little, the scenario seems no different. Ranking DoorDash against other stocks in the entire Industry, it places 45th from a result of 58 stocks.

Valuation Grade (Seeking Alpha)

Concluding thoughts

I rate this stock as a Strong Sell. It looks highly likely that the stock will severely underperform the market in the years to come. That does not mean to say that the business won’t grow. It may continue to grow, increase market share in existing segments and also foray into new segments. But a combination of high valuation, shareholder dilution and unprofitability could keep the stock price performance suppressed and there are better opportunities for an investor’s capital.

Be the first to comment