DamianKuzdak/E+ via Getty Images

Article Thesis

Medical Properties Trust (NYSE:MPW) has crafted a deal that will reduce its Steward exposure and that will allow Steward to pay back some of the money it owes MPW. This is an excellent deal for MPW that eases some of the concerns bears have had in the past. At the same time, MPW also offers a high dividend yield and trades at an undemanding valuation. Shares have significant upside potential, I believe.

What Happened?

A couple of days ago, Steward, Medical Properties Trust, and CommonSpirit Health announced a series of deals that will be great for Medical Properties Trust as reported here on Seeking Alpha. Steward will sell its hospital operations in Utah to CommonSpirit Health, which, in turn, will lease the hospitals that were previously used by Steward from Medical Properties Trust. MPW’s news announcement can be found here.

Why It Matters

Medical Properties Trust stock will continue to own the same assets it owned in the past, and yet, this deal is highly impactful for MPW, as it helps the company in making progress when it comes to reducing the proclaimed Steward risk. Steward has been MPW’s most important tenant for quite some time, and Steward has experienced financial troubles. That made some bears fear that MPW could lose a lot of money if Steward were to go bankrupt. While some MPW bulls, including us at Cash Flow Club, argued that a potential bankruptcy by Steward was not a company-threatening event for MPW as the hospitals would still be used by a restructured Steward or another tenant even if Steward were to go insolvent, the Steward situation still was a major problem for MPW’s share price:

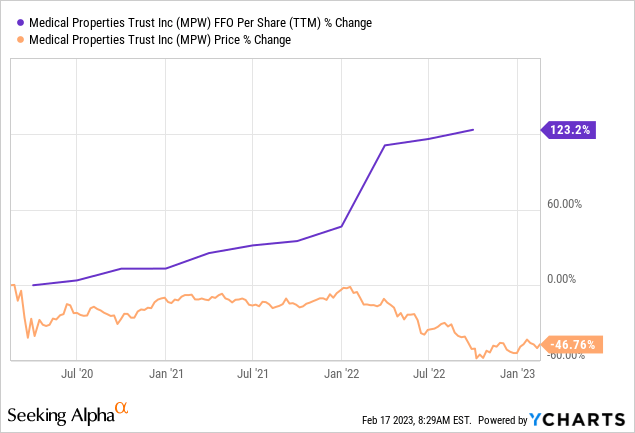

Over the last three years, MPW grew its funds from operations per share by 123%. And yet, over the same time frame, its share price has been cut in half. Clearly, the issue wasn’t MPW’s underlying results – those were strong, as evidenced by the high FFO and EBITDA the company generates. Instead, MPW’s shares suffered due to multiple compression – the market suddenly decided that it wants to pay significantly less per dollar in profit that MPW generates. This, in turn, is largely attributable to the fears around the Steward situation and what a potential Steward bankruptcy might do to MPW.

While we have thought for a while that these concerns about Steward are overblown, as the underlying assets (the hospitals that MPW owns and that Steward uses) would not vanish even if Steward were to go bankrupt, it is pretty clear that many market participants were fearful due to the Steward exposure. With the deal that has now been crafted between Steward, MPW, and CommonSpirit Health, the Steward situation should improve meaningfully, due to several reasons.

First, with the sale of the Utah operations from Steward to CommonSpirit Health and with MPW now leasing these properties to CommonSpirit Health, MPW’s exposure to Steward has naturally declined. The Utah hospitals make up 6% of MPW’s asset base, thus MPW’s exposure to Steward has declined by 600 base points, which is quite meaningful. Even if Steward were to go bankrupt in the future, the impact on MPW would be smaller. CommonSpirit Health has an investment-grade credit rating, thus there is very little risk to worry about bankruptcy with this new tenant. The lease terms are attractive as well, as MPW will receive 7.8% of its gross investment in the first year, with a 3% annual escalator. In the not-too-distant future, the cash yield will thus be 10% – around eight years from now. While a 3% annual rent escalator is below the current inflation rate, it will be north of the inflation run rate once the Fed has managed to bring down inflation to the target 2% range.

Second, the sale of the Utah operations to CommonSpirit Health will lead to cash proceeds for Steward. While the deal value has not been disclosed, Steward expects to use these cash proceeds for debt reduction purposes. This will, according to MPW, include the early prepayment of loans that were made by Medical Properties Trust. The deal will thus strengthen Steward’s balance sheet and reduce its bankruptcy risk, and since Steward will pay back money that it owes to MPW, the deal will also strengthen MPW’s balance sheet. MPW can use the cash inflows for reducing its own debt, thereby strengthening its balance sheet, which will reduce its own risk and exposure to the current rising interest rate environment.

In 2022, Medical Properties Trust has stated that Steward’s operations would be improving and that the company would soon be able to generate positive free cash flows. That will reduce risks, and with the additional cash inflows from the Utah operations sale, Steward’s company-specific risks will decline further. With MPW becoming less dependent on Steward, MPW will become even safer from any Steward-related trouble. Since the Steward situation was the biggest bearish argument against Medical Properties Trust in the recent past, the deal between Steward, MPW, and CommonSpirit Health should thus be highly beneficial for MPW and its shares.

Valuation And Dividend

The initial reaction to the deal announcement was positive, and MPW’s shares jumped upwards. But considering where shares trade today, relative to where they traded in the past, the rally may just be beginning. Steward tried to sell the same Utah assets in the past, to HCA Healthcare (HCA). That deal did not work out due to antitrust issues, however. When that original deal from late 2021 was announced, MPW traded at marginally above $20 per share. The market liked that original deal due to the same positives – declining Steward exposure, and a stronger balance sheet for Steward – which is why Medical Properties Trust saw its shares climb to the $24 range over the following two months. It is, of course, not guaranteed that we will see MPW rise to the mid-$20s again. But considering that the underlying business has performed well and that dividends did not decline, it seems possible for MPW to rise to the old share price eventually.

Even if MPW were to climb to just $20 per share, that would make for very compelling total returns for someone buying at current prices of around $12.80 per share – that would be a 56% return before dividends. And from a valuation perspective, a climb toward the $20 range seems quite possible, although it could take a while.

Medical Properties Trust’s guides for normalized funds from operations per share of $1.81 in 2022 (Q4 results aren’t out yet). Even if that amount does not grow in 2023, despite rent escalators, a $20 share price would only require an 11.0x FFO multiple. For a recession-resistant (hospitals are needed in any economic environment) real estate player, that’s not a very demanding valuation. Of course, that means that the current valuation is even lower, as MPW trades for just 7.1x 2022’s expected normalized funds from operations, which pencils out to a 14% FFO yield. I believe that this is far from justified, especially not following the recent good news that will reduce the Steward risk considerably. I would thus not be surprised to see MPW benefit from multiple expansion going forward.

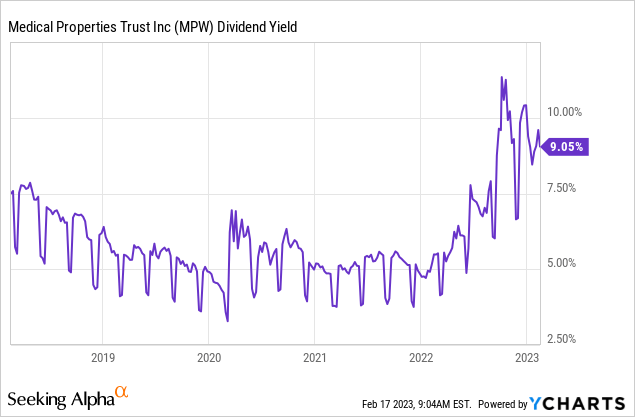

With the Steward risk waning, the dividend cut risk for MPW will decline as well. While we always thought that the MPW dividend is pretty safe, more market participants will now likely agree with this belief. This, in turn, could lead to increased buying from income investors, as MPW’s dividend yield of 9.1% is quite attractive still. At a $20 share price, the yield would still be very solid, at 5.8%:

That would be relatively in line with how MPW was valued in the past, as its yield oftentimes was in the 5%-6% range. The current yield levels are an absolute outlier, however, which is why we expect that the yield will not remain this high – due to a rising share price, not due to a dividend cut.

The following chart also shows that MPW is inexpensive versus how its peers are valued:

Stock Rover

Final Thoughts

Medical Properties Trust has already climbed from the lows seen in 2022 and has returned more than 12% since our last bullish article in October. But that might only be the beginning – due to a high yield, waning Steward issues, and a very undemanding valuation, we would not be surprised to see MPW climb meaningfully in the coming years. It does not take especially bullish assumptions to craft a scenario where MPW eventually trades at $20 again – a meager 11x FFO multiple without any business growth would be sufficient. MPW traded at well above $20 for some time in the past, thus a share price of $20 would not be unprecedented. With MPW offering a 9% dividend yield while we wait for MPW to rise back to a more normal valuation range, the REIT looks attractive for total return investors and income investors alike.

Be the first to comment