knowlesgallery/iStock via Getty Images

Commodity Sentiment Remains Bullish

Commodities continue to run hot because they are in a global short supply. As the world watches oil, nickel, copper, and wheat prices skyrocket, exasperated by the War with Russia-Ukraine, commodities are becoming an excellent hedge against the Fed’s hiking cycle. According to Seeking Alpha News, CBOE Global Markets’ Q1 options volume hit a record for its second consecutive quarter. Earlier this year, oil jumped above 130/barrel, gold rallied to a high of $2,070 an ounce, and post-pandemic global supply chain disruptions are getting worse on the heels of the Russia-Ukraine conflict, and inflation is prompting investors to consider commodities from energy to agricultural to diversify portfolios and capitalize on rising costs.

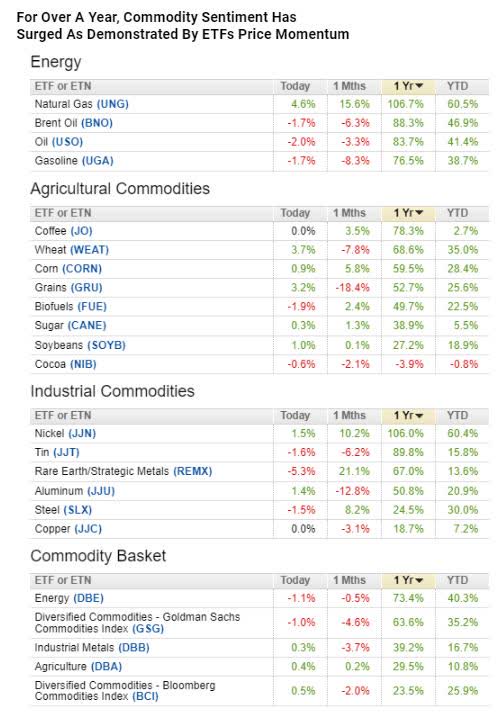

Commodity Sentiment (Seeking Alpha ETF Performance)

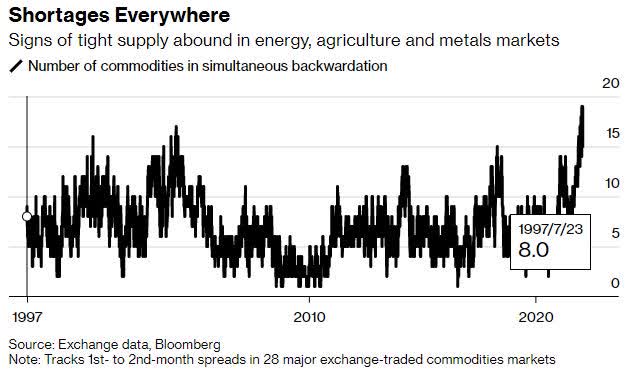

As evidenced by the Bloomberg visual below, 19 out of 28 raw materials are trading in backwardation, something not seen since 1997. We’re experiencing many commodity futures in backwardation (the current price of a commodity is higher than its price in the futures market), which highlights the short supply, resulting in higher prices.

Commodity Shortages Everywhere (Bloomberg)

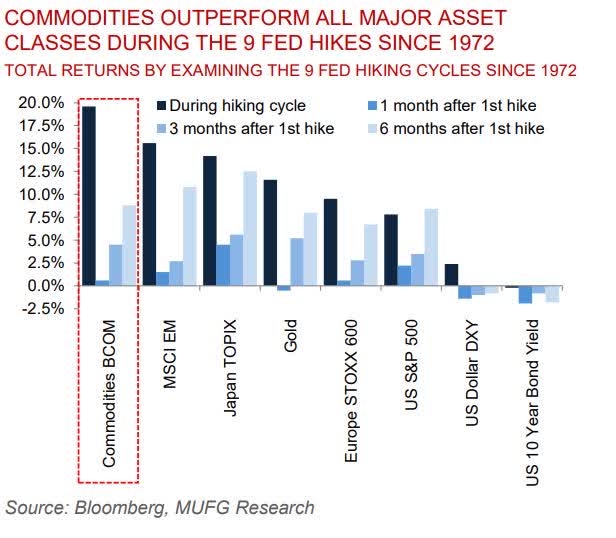

Record-high commodity prices began the first quarter of 2022 with a bang, offering three-digit price increases, the most significant price increases in over a decade. As I wrote in You Name It, We’re Out of It, shortages in energy, agricultural products, and metals are key drivers of the rising prices. If you’ve not yet capitalized, do not fear the price action over the last year, as history has shown commodities outperform when the Federal Reserve is on the warpath. In fact, according to MUFG Research chart below, commodities have outperformed all major asset classes since 1972, following the last nine fed hikes.

Commodities Outperform All Major Asset Classes Since 1972 (Bloomberg, MUFG Research)

The Fed is tightening monetary policy and raising interest rates because inflation has gotten away from them. Going forward, what’s crucial to monitor is the pace at which the Fed raises rates. If they get too aggressive, they could ultimately crater or stifle demand, triggering a recession. For now, as long as demand exceeds supplies, commodities are an excellent hedge against inflation, and we have five stocks for you to consider for your portfolio.

5 Top Commodity Stocks for 2022

1. Intrepid Potash, Inc. (NYSE:IPI)

For those unfamiliar with potash, it is a potassium-rich salt mined from seabeds, used primarily in fertilizers to support crop yields and enhance water preservation. Potash resulted when ancient inland seas evaporated millions of years ago. Its uses include fracturing fluids for oil and gas and various chemical products like pool salts, detergents, and ice melt. Together with its subsidiaries, Intrepid Potash, Inc. (IPI) engages in the extraction and production of potash globally. The stock has been trending upward with a +84% YTD increase, and over the last year, it’s seen a near 150% share price jump. IPI’s overall Valuation grade is A- and indicates this stock is trading at a discount, with current P/E ratios of 4.42x, nearly 75% below its sector peers.

IPI Factor Grades (Seeking Alpha Premium)

As we take a closer look at IPI’s collective factor grades, momentum is stellar, and we believe the stock overall is bullish.

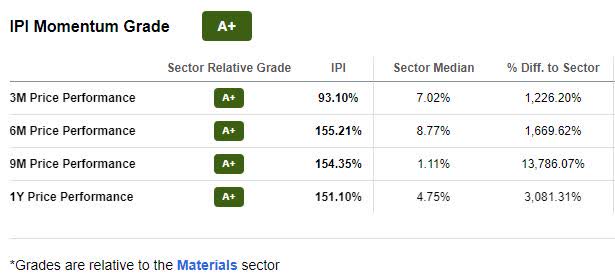

IPI Momentum Grade

Intrepid has done well over the last five years, as its share price grows. The company has improved its financial situation by increasing its top and bottom lines, and as evidenced by the momentum grades, the company is steadily increasing its quarterly price performance.

IPI Momentum Grade (Seeking Alpha Premium)

When reviewing the above figures and IPI relative to its peers, we have a lot to be excited about. IPI is currently ranked #1 in its industry and sector. Intrepid is growing with a favorable outlook, zero debt on its balance sheet, and a $35M share buyback announcement, so let’s explore the growth and profitability numbers. Author of Deep Value Returns, Michael Wiggins De Oliverira, highlights in his article Intrepid Potash: Why I’m Buying This Stock, “The business is in a greatly improved shape, with no debt on its balance sheet and Intrepid’s free cash flow in 2021 jumped to $60 million compared to $14 million in 2020.”

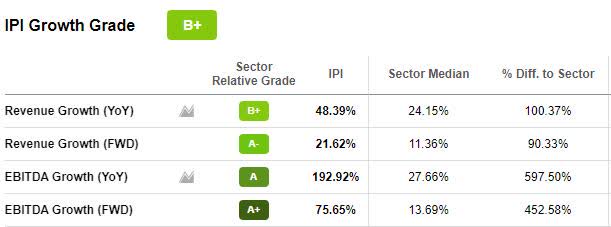

IPI Growth & Profitability

Despite IPI going through a rough patch from 2016 to 2017, where its share price dropped from $6.91 to $1.09, and the firm contemplated bankruptcy, the stock rebounded and is currently on a tear, in line with oil, gas, and other commodities. After coming to terms on a $35M revolving credit agreement and removing bankruptcy concerns, IPI could focus on the future, which is paying off handsomely, as it is currently trading at over $80/share.

IPI Growth Grade (Seeking Alpha Premium)

“In 2020, the sales price per ton of IPI potash was $250. As of only two weeks ago, Canpotex agreed to sell potash to India and China at $590 per ton,” writes Seeking Alpha Contributor Jason Wong. Additionally, Intrepid announced paying off all outstanding debt in Q3 of 2021 and had $26M cash on hand. Currently, IPI has $79M Cash From Operations and an overall Profitability Grade of A and a solid B+ Growth Grade. With year-over-year revenue growth at 48.39%, forward operating cash flow growth at 153.87%, and a growing balance sheet, it’s no wonder company executives anticipate an increase in sales and growth throughout 2022. “With a strong balance sheet in a growing cash position, we announced in our earnings release a $35 million share repurchase program…We expect our first quarter 2022 net realized price for Trio will increase between $440 and $450 per ton, and we are currently booking sales for second-quarter shipments at the increased price level, which is approximately $215, moreover last year,” said Bob Jornayvaz, Intrepid Co-Founder & CEO during the Q4 2021 Earnings Call. Agricultural commodities and fertilizers are big benefactors of the current market environment, but metals and mining companies are also reaping the benefits.

2. Alpha Metallurgical Resources, Inc. (NYSE:AMR)

U.S. mining company Alpha Metallurgical Resources Inc. (AMR) produces, processes, and sells coal. Despite its share price tumbling 11% Monday among other material losers, there’s no news to consider this a concern. The stock’s short-term momentum may be pausing on the back of its record move. We consider it a strong buy at even more of a discount!

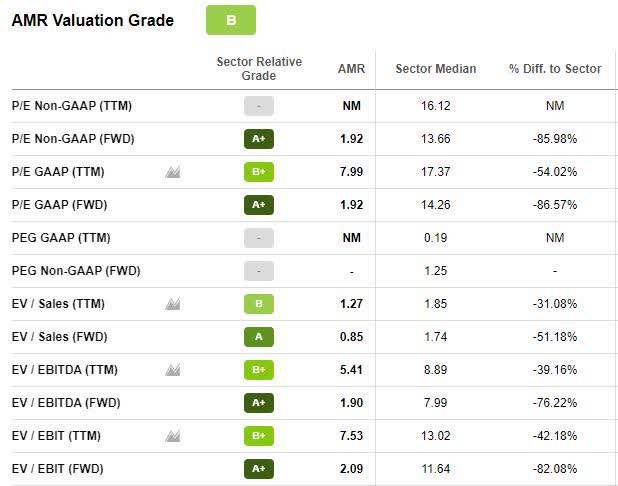

AMR Valuation (Seeking Alpha Premium)

AMR is currently trading more than 85% below the sector with a forward P/E ratio of 1.92x. We believe now is a great time to buy this stock, ranking #1 in its industry out of 26 at a price under $125/share and a strong growth and profitability outlook. EV/Sales and EV/EBIT numbers are strong, and Alpha’s overall B Valuation grade is solid.

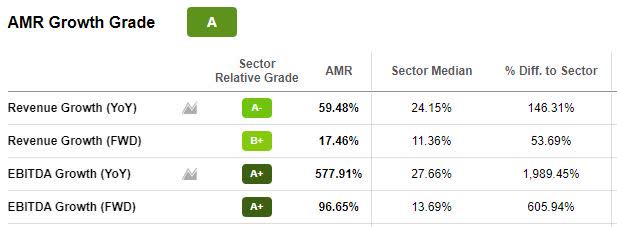

AMR Growth & Profitability

Alpha Metallurgical Resources’ earnings have been strong over the last couple of quarters, and Q4 turned up significant figures, including an EPS of $13.45, beating by $2.01. YoY Revenue of $828.22M, beat by more than 155%. Intending to eliminate long-term debt, the company paid down $200M, bringing its current debt level to $300M.

AMR Growth Grade (Seeking Alpha Premium)

Profitability also remains solid with its overall B+ grade. As the war in Ukraine persists, coal prices are on the rise according to SA News, jumping above $100/ton for the first time in more than a decade. AMR is capitalizing and continues its growth trajectory and profitability.

AMR Profitability (Seeking Alpha Premium)

Current EBITDA Margins are solid at 23.53%. As the company continues to pay down debt, we should see the Cash from Operations of $174.94M steadily increase. As evidenced by the figures above, the company’s growth remains strong and strengthened by the current need for more coal. “Given the continued strength of the current coal markets and faster than expected pace, which we’ve been able to dramatically reduce our debt, and legacy liabilities, we are also pleased to announce a shareholder return program. Our Board of Directors has approved a $150 million share repurchase program that will allow us to buy back our stock in the open market,” said David Stetson, AMR Chairman & CEO.

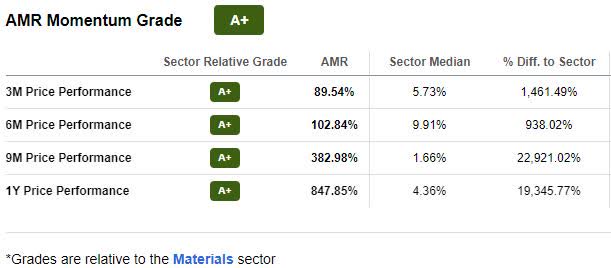

AMR Momentum

AMR Momentum Grade (Seeking Alpha Premium)

AMR’s long-term outlook appears strong given the company’s momentum and performance over the past year. It’s clear from the last three months to one year that shares of AMR have increased quarter-over-quarter significantly, gaining 847.82% over the previous year. Short-term price is an excellent indicator of investor interest in the stock, and when compared to the industry, AMR is a top company.

3. Teck Resources Limited (NYSE:TECK)

Diversified metals and mining company Teck Resources Ltd. (TECK) explores and produces natural resources worldwide and operates through steelmaking coal, copper, zinc, energy, and corporate segments. The company has had tremendous growth year-over-year and the stock has a very solid valuation framework. Teck Resources also holds a tremendous amount of cash at $3.75 billion and has decided to round up its cash position by selling a small mill to Bunker Hill Mining (OTCQB:BHLL). “Bunker Hill Mining reached an agreement with Teck Resources’ for satisfying the remaining purchase price for the Pend Oreille Mill… Under the agreement, a total purchase price of $2.75M is to be paid to Teck in cash or $3M in cash and shares; non-refundable deposit of $500K was paid earlier towards the purchase price.”

TECK should have a strong outlook, given its exclusive option to acquire 100% of the mine’s production of zinc and lead concentrate over five years. “With the Trail Smelter as the natural home for Bunker Hill’s future concentrate production, we are excited to lay the groundwork for a potential long-term offtake relationship and broader strategic partnership with Teck,” commented Bunker Hill CEO Sam Ash.

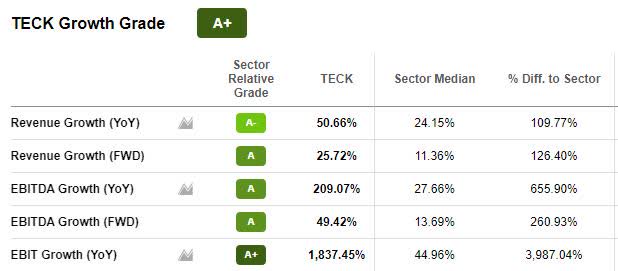

TECK Growth and Profitability

Growth prospects for this stock have already proven strong, as evidenced by the below growth grades and quarterly results that produced EPS of $1.98 beating by $0.11, Forward Revenue Growth is at 25.72%, and YoY EBIT Growth is substantially above the sector at 1,837.45%.

TECK Growth Grade (Seeking Alpha Premium)

With its strength in numbers, analysts within the last 90 days have given the stock 21 FY1 Up Revisions and zero down, leading to an A+ Revisions Grade. Commodity prices remain high, so TECK is reaping the benefits by selling 76,000 tons of copper, 5.9M tons of metallurgical coal, and approximately 2.2M barrels of bitumen in Q3 of 2021. As commodity prices continue to skyrocket with high demand persisting, TECK is an ideal stock pick whose gross profit margins and whopping $3.75B Cash on Hand should quickly grow.

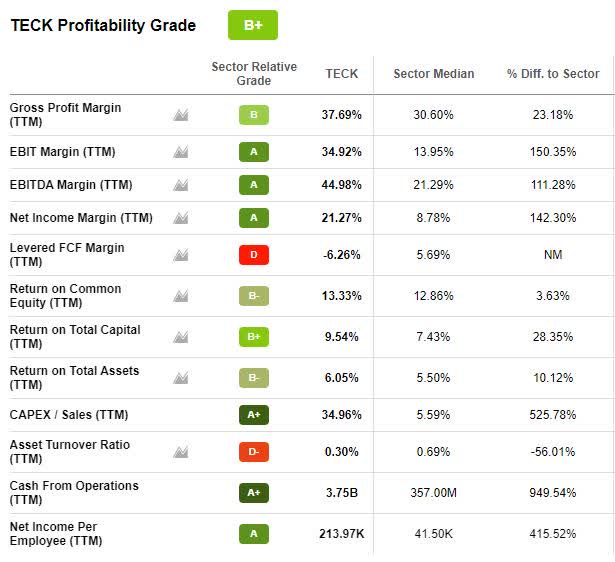

TECK Profitability Grade (Seeking Alpha Premium)

“With $6+ in earnings per share being projected for fiscal 2022, we see TECK’s return on equity growing at a swift pace over the next few years. Currently, TECK’s ROE comes in at just over 4.3% over a trailing twelve-month average…TECK’s bullish technicals are certainly being backed up by the fundamentals,” writes Seeking Alpha Contributor Individual Trader, and I agree, and is why at its B valuation, this stock comes as a steal.

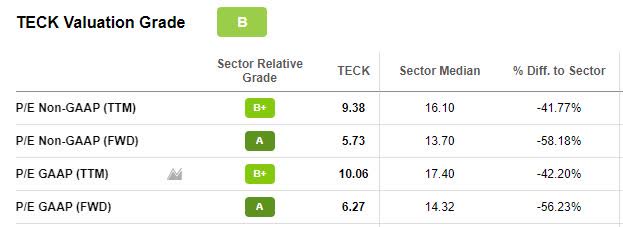

TECK Valuation

Trading substantially below its sector with a forward P/E ratio of 5.56x, -59% difference from the sector, and a price point below $40/share, you can’t go wrong given the current path of commodities.

TECK Valuation Grade (Seeking Alpha Premium)

Copper and steel are resources for the future, and TECK Resources is one stock that is doubling down on production, by way of smart partnerships like Bunker Hill which will help drive growth well into the future. Another such company is Mosaic. In addition to its current price, YTD, the stock is +34%, its one-year +94%, and over five years, it has seen more than a 68% share price increase.

4. The Mosaic Company (NYSE:MOS)

Similar to our stock pick Intrepid (IPI) above, The Mosaic Company (MOS), through its subsidiaries, markets and produces potash crop nutrients globally, a mix of crop nutrients and animal feed ingredients for industrial use. Like some of the other stock picks we’ve discussed today, MOS is on a tear shattering records in the fertilizer industry. Because fertilizers are in short supply due to Russia’s invasion of Ukraine and reduction in supply volumes due to labor strikes in Canada, North American fertilizers producers like Mosaic are capitalizing. A Seeking Alpha report highlights that “‘Russia is a major, major exporter across all of the major fertilizers… losing Russian exports is a very big deal,’ says Josh Linville of StoneX Group, noting that the country accounts for 14% of urea, as much as 31% of UAN, 10% of phosphate, and nearly 20% of the global operating potash capacity.”

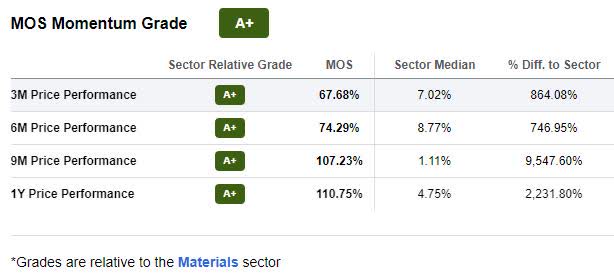

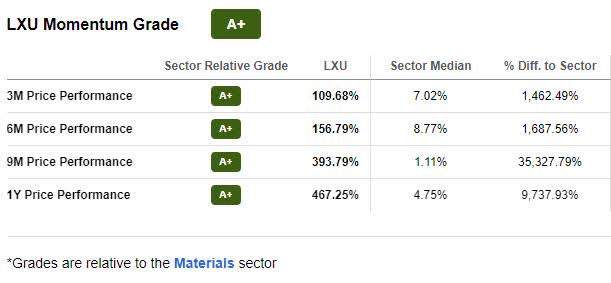

Despite Mosaic’s D+ Valuation grade, the stock has excellent momentum and is trading under $70/share with stellar short-term price performance. Looking at the A+ Momentum grade below, this stock is a top stock in its respective sector, gradually outperforming its peers on a quarterly price-performance basis.

MOS Momentum (Seeking Alpha Premium)

Given the stock is strongly bullish, investors should continue to pay higher prices for MOS shares as it continues to trend higher. As we look to MOS’ future, let’s dive into the growth and profitability prospects.

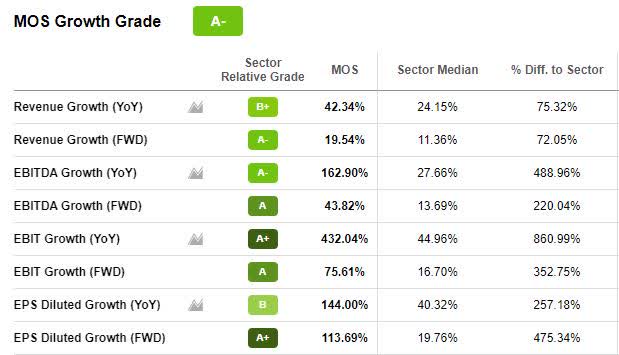

MOS Growth and Profitability

Agricultural prices are at multi-year highs. Given the strong demand for crops and shortages stemming from geopolitical issues in Europe, stocks like MOS will advance. It is a leading producer of potash and phosphate fertilizers desired by the growing demand for fertilizers that can boost yields.

MOS Growth Grade (Seeking Alpha Premium)

Mosaic displays strong growth and profitability grades. Year-over-year revenue growth is strong at 42.34% compared to 24.15% for the sector. EBIT Growth for the same period is stellar and significantly trumps its median peers.

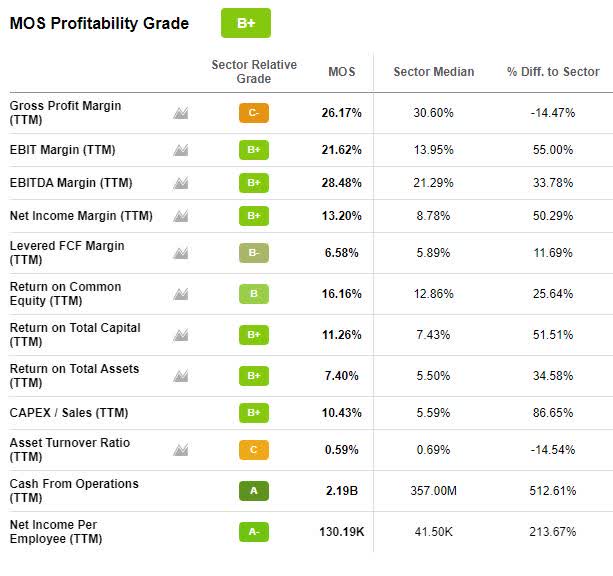

MOS Profitability Grade (Seeking Alpha Premium)

As we look at MOS’ cash from operations and underlying profitability margins relative to the sector, higher demand for potash should increase profitability figures. Namely, as some of the top five countries account for more than 75% of potash production, China and India’s potash lags significantly. To secure food supplies, potash prices specifically for those nations have risen drastically and should persist at those levels for some time, prompting U.S. producers like Mosaic to profit handsomely.

Emphasizing its excellent financial performance, during the Q4 Earnings Call, Mosaic President and CEO Joc O’Rourke said, “For Mosaic Fertilizantes, we expect the business to continue reflecting the favorable market backdrop and our transformation efforts in 2022. Sustained grower demand and improved market positioning should continue to drive results.” We agree, and as we transition from fertilizers and agricultural chemicals, there is one last chemical company worth adding to a portfolio.

5. LSB Industries, Inc. (NYSE:LXU)

LSB Industries, Inc. (LXU) is a nitrogen-based fertilizer company that manufactures, markets, and sells chemical products like ammonia and fertilizer blends for corn and other crops. Although the stock has a D+ valuation, the overarching fundamentals we look for in addition to valuation like growth, EPS revisions, profitability, and momentum are strong.

LXU Momentum

With the increasing demand for chemicals and fertilizers that offer higher crop yields, and lower carbon, while meeting the needs of this volatile market, stocks like LXU continue to expand, with no sign of slowing. “North American growth in organic fertilizer is one of the biggest opportunities for agricultural purposes and is expected to grow at a CAGR of over 13% from 2022 thru 2027,” writes Seeking Alpha Contributor, EnigmaDude.

LXU Momentum (Seeking Alpha Premium)

Sanctions against Russia are putting pressure on companies with the supplies to produce, thus LXU’s momentum in the short-term should continue to experience an uptick. LXU’s YTD share price is up 105% and, at its current trajectory, is showcasing that this stock pick could help grow your portfolio in addition to crops! Let’s check out some of its growth and profitability metrics.

LXU Growth and Profitability

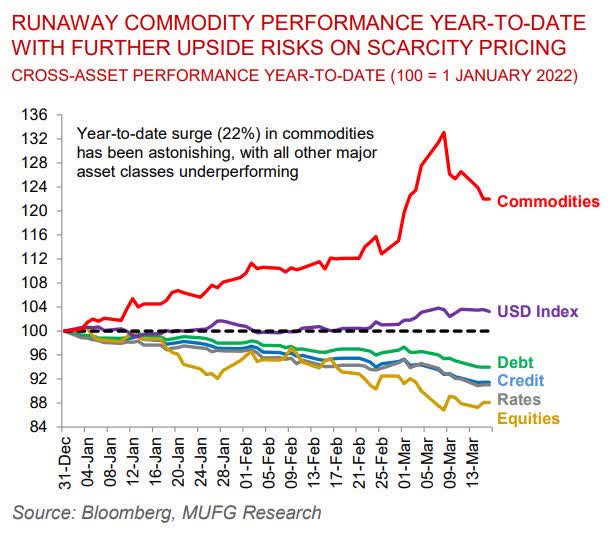

Year-to-date commodity performance is astounding, as showcased by the below chart. MUFG Commodities Weekly writes, “A core rationale as to why commodities perform well during hiking cycles is that the root cause of the inflation that the Fed is endeavoring to tackle is created by strong and rising physical goods demand rather than cost push supply economics.”

Runaway Commodities YTD Performance (Bloomberg, MUFG Research)

The continued surge in commodities is why I believe these assets are excellent short-term hedges against rising inflation and are fundamentally sound.

LXU Growth Grade (Seeking Alpha Premium)

LXU revisions are strong (A+) following Q4 results and an EPS of $0.47, beating by $0.19. Year-over-year revenue growth has been solid at 58.33% and EBITDA growth for the same period is 209.17%. Profitability metrics, while average (overall C- grade), should improve given the charts and outlook for this sector. Record high fertilizer prices pose opportunistic as companies are pushing off these prices to consumers, which should increase profit margins. With agricultural products representing more than 50% of LXU’s net sales and gross profits, this commodity stock pick and some of the others are growth-oriented and excellent choices in this challenging investing environment, trending upward and capitalizing on global trends.

Conclusion

War, fear, supply chain issues, inflation, and the threat of a tightening monetary policy are creating market volatility. Inflation at a 40-year high shadows the economic environment, and commodity resources are in short supply. Over the last few weeks, some commodity stocks have experienced enhanced volatility. Zooming out of the trading patterns of the previous few weeks, since 1972, history has shown commodity stocks fair well when the Federal Reserve is on a campaign of interest rate hikes. There is increased speculation that the Fed may take rates up too much and potentially set up an environment for a recession in 2023 or 2024.

According to Seeking Alpha Contributor BlackRock, on average, since 1997, commodities have historically outperformed the S&P 500 in the first 12 months after the beginning of a rate hiking cycle. BlackRock’s key takeaways are that “commodity indexes have rallied amid heightened geopolitical uncertainty and structural supply shortages… commodities have historically shown resiliency in rising rate environments and can help investors hedge against rising inflation and diversify portfolios.” The stocks I am recommending, IPI, AMR, TECK, MOS, and LXU, are Strong Buys based on our quant ratings, growing earnings, and solid profitability. They are defensive in the current inflationary environment, and the inherent nature of their businesses allows them to pass on rising costs to their customers.

Our investment research tools help to ensure you’re furnished with the best resources to make informed investment decisions. Consider Top 5 Energy Stocks To Buy in this uncertain and inflationary environment. You can also use Seeking Alpha’s ‘Ratings Screener’ tool to help you achieve diversification into desired sectors you like, including commodities. Click the links above to get started.

Be the first to comment